Top 5 Quality Buys March 🚀

5 Fairly priced Quality Businesses 💎

Hi partner! 👋🏻

Welcome to the March edition of Top 5 Buys ✅

You can access our Top 15 Buys for 2025 list as a premium member here.

In this article, we will discuss our top stock picks for March 2025.

Let’s get into it 👇

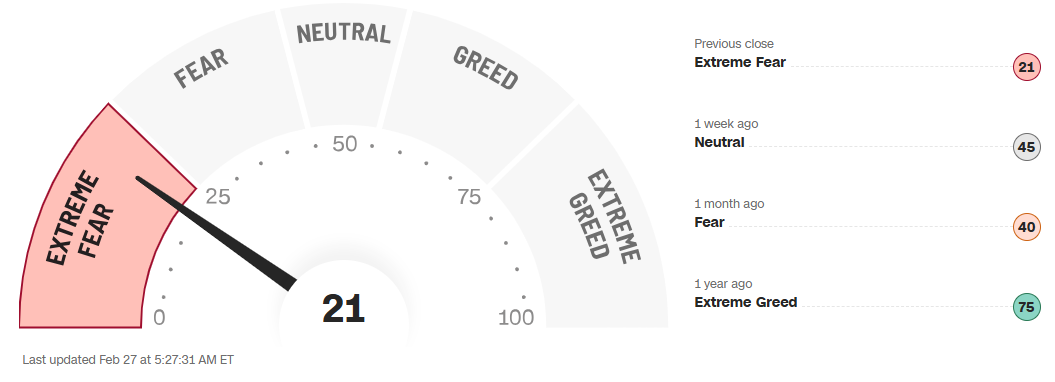

The Market Sentiment: Extreme Fear

The Fear to Greed index is (finally) pointing towards extreme fear, indicating that investors are more fearful of taking excess stock market risk.

For long-term investors, fear in the market is synonymous with opportunities.

Lower prices in quality assets are often long-term opportunities for savvy investors.

The last time the market was at similar levels (<25), we saw a dip in the market (August 2024). This does not mean that the market can’t keep declining, but for long-term investors, we get better risk-reward opportunities from lower prices than higher prices in the stock market.

Cheap stocks from our investable universe (Sorted by PE)

A sample from our investible universe sorted by lowest TTM PE. There are many attractively priced quality companies in markets outside the US.

What is a Good Buy? 🧠

We emphasize understanding the fundamentals before investing. If you prefer an in-depth analysis, check out our guide, trusted by over 300 investors. We also offer a free valuation cheat sheet for a straightforward approach to determining a company’s intrinsic value.

We assess a company's quality based on its business model, revenue generation, margins, return on capital, management, and competitive advantages. We then analyze its historical valuation to identify attractive buying opportunities.

Invest in Quality is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Disclaimer: This is not investment advice. Always conduct your due diligence and make your own investment decisions.

Now, let's get into it 👇🏻

Top 5 Quality Buys March 2025 🚀

The Hershey Company NYSE: HSY 0.00%↑ 🍫

The Hershey Company (HSY) is a global leader in confectionery. It is known for its iconic brands, such as Reese’s, Hershey’s, and Kit Kat. With strong brand loyalty and pricing power, the company maintains a dominant position in the chocolate and snacking markets.

Despite rising input costs, Hershey’s ability to manage expenses and pass costs to consumers helps sustain solid margins. Its expansion into better-for-you snacks and strategic acquisitions further strengthen its growth prospects.

Looking ahead, Hershey is investing in innovation, digital marketing, and international expansion. These initiatives position the company to capture new market opportunities and drive long-term shareholder value.

Key fundamentals:

Gross Margin: 47.4%

Operating Margin: 26.7%

Return on Equity (ROE): 56.8%

Revenue growth (3Y): 7.0%

Earnings per share growth (3Y): 15.4%

Forward PE: 29.2x

Why we like The Hershey Company:

Strong brand loyalty and pricing power—Hershey owns some of the most recognizable confectionery brands, including Reese’s, Hershey’s, and Kit Kat. Its strong brand equity allows the company to maintain pricing power, helping it offset rising input costs and sustain high profit margins.

Resilient demand and diversified product portfolio– The snacking and confectionery industry remains stable even during economic downturns, as consumers purchase affordable indulgences. Hershey’s expansion into better-for-you snacks, premium chocolates, and international markets provides additional growth avenues beyond traditional candy sales.

Consistent Financial Performance & Shareholder Returns – Hershey has a track record of steady revenue and earnings growth, driven by strong operational efficiency and cost management. The company remains an attractive long-term investment with consistent dividend payments (Yield of 3.1%), share buybacks (Yield of 1.47%), and strong cash flow generation (FCF yield of 5.52%).

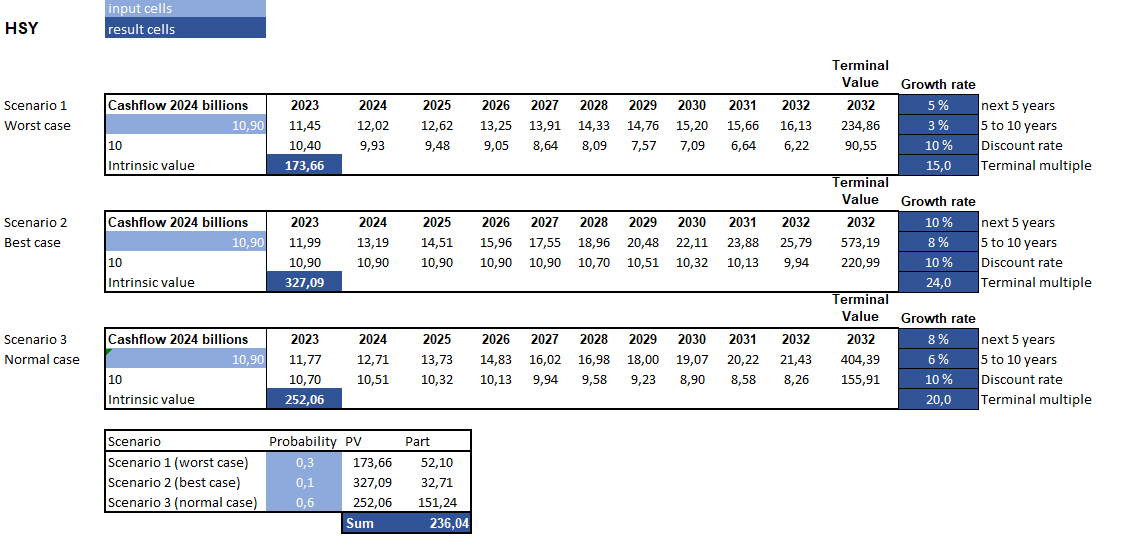

Simple Discounted Cash Flow Analysis

The short-term outlook for Hershey is not good, but we believe the strong brands, coupled with efficient operations and cost control, will provide solid growth in EPS long-term.

Fair value estimate: $236.04

Current price: $171.29

Upside: +37.8%

Expected CAGR: +15%

UnitedHealth Group NYSE: UNH 0.00%↑ 🧑🏻⚕️

UnitedHealth Group (UNH) is a dominant player in healthcare. It operates through its insurance arm, UnitedHealthcare, and its healthcare services division, Optum.

Its diversified revenue streams and operational efficiency help mitigate risks from regulatory pressures. UnitedHealth’s ability to manage costs while delivering essential healthcare services keeps it well-positioned for stable growth.

Looking ahead, UnitedHealth is investing heavily in digital health, AI-driven solutions, and value-based care. These innovations could enhance efficiency, improve patient outcomes, and drive long-term growth in an evolving healthcare landscape.

Key fundamentals:

Gross Margin: 22.3%

Operating Margin: 8.1%

Return on Equity (ROE): 21.6%

Revenue growth (3Y): 11.7%

Earnings per share growth (3Y): -5.0%

Forward PE: 15.8x

Why we like UnitedHealth Group:

Market leader with multiple revenue streams—UnitedHealth Group is the largest U.S. health insurer and a leader in healthcare services through its Optum segment. With a wide customer base and multiple revenue sources—including insurance, pharmacy benefits, data analytics, and medical services—it has strong competitive advantages and reduced reliance on any single business line.

Consistent organic growth and financial strength—UNH has delivered strong revenue and earnings growth over the years, supported by operational efficiency and pricing power. Its ability to generate substantial cash flow allows for consistent dividend increases, share buybacks, and reinvestment in high-growth areas like digital health and AI-driven healthcare solutions.

Long-Term growth drivers—As healthcare costs rise and the industry shifts toward value-based care, UnitedHealth is positioned to benefit from increased demand for managed care and cost-saving healthcare solutions. Its investments in AI, telemedicine, and data-driven healthcare services through Optum provide long-term growth opportunities in an evolving market.

Simple Discounted Cash Flow Analysis

UnitedHealth is expected to grow its long-term EPS by 15% CAGR.

Fair value estimate: $579.85

Current price: $463.59

Upside: +25.07%

Expected CAGR: 14%

The rest of the article is for premium subscribers, read more here: