The Quality Growth System📈

Systematic approach to investing (Evolution AB example)

Thank you for subscribing to Invest In Quality.

We deeply value your feedback, and would love for you to take this 3-minute survey to help us improve our service to you:

In this article, I will provide an example of a Quality Growth based investing system that you can use to analyze potential investments.

If you like this kind of post, please leave a ❤, and a comment, or reply to this email and let us know. We love your feedback!

The system will also work as a checklist, making sure you have done your due diligence before investing.

The Quality Growth System consists of 6 components:

The Six Components of the System:

I) Competent management with skin in the game

II) A superior business model

III) A strong competitive advantage

IV) Growing demand for the product or service sold

V) Risk factors

VI) Valuation

For this example, we will use Evolution AB ($EVVTY):

I) Competent management with skin in the game 8.3/10

High insider ownership 9/10

Key executives own significant stakes in the business.

CEO owns 684.710 shares + rights through warrants

CPO owns 96.300 shares + rights through warrants

CSO owns 700.000 shares + rights

CFO owns 60.000 shares + rights

Insiders are purchasing shares 8/10

Carlesund bought SEK100 million worth of stock in the open market (CEO) in recent months.

Track record 10/10

The current management team is responsible for taking Evolution from a small niche software player to a Live gaming powerhouse.

Total stock return in the tenure of management is a CAGR of 62.3% annually.

Tenure 9/10

CEO since 2015

CPO since 2015

CSO since 2008

CFO since 2016

Long-term focus 8/10

Management is creating long-term shareholder value

Management incentives are aligned with shareholders

No proof of short-term thinking from executives

Capital allocation 6/10

Spent shareholders capital on a few poor acquisitions that have not materialized in the RNG segment.

Would like to see Evolution making tactical buybacks when the share price is depressed, not buybacks at any price.

Would like to see more buybacks and less dividends (Personal preference)

Combined score for management: 8.3/10

II) A superior business model 8.7

Why is the business model superior to competitors? 8/10

Evolution is uniquely positioned to benefit from the global trend of online live gaming, being the clear market leader and choice for customers. Evo is the best live games operator in the world, and its incentives are aligned with its customers, creating a virtuous cycle of product improvements to satisfy customers and increase their returns per game/table.

Does Evo make money in a unique way? 8/10

It makes a percentage of what their customers are making. This means that the more successful Evolution’s games are, the happier the customer (Casinoes) gets, and the more money Evolution makes. Few companies have pulled off a similar model to the extent Evo has.

Is their distribution unique compared to competitors? 7/10

Yes. Competitors are not able to replicate their business model and create value at scale like Evolution does.

Does their model affect their relationship with suppliers/customers? 9/10

Incentive alignment with customers creates a virtuous cycle

Customers are satisfied and willing to pay higher take rates for Evolution’s services as they have the best-in-class games & live operation.

Capital light business model 10/10

Capital expenditure 2023: 42.2 million Euro

Operating revenues 2023: 1.798,6 million Euro

Operating cash flow 2023: 1.168,4 million Euro

Capex / Revenue = 42.2 / 1.798,6 x 100 = 2.3% of revenue (Very low)

Capex / OFC = 42.2 / 1.168,4 x 100 = 3,6% of OCF (Very low)

Stock-based compensation 9/10

Evolution does not issue stock-based compensation, but offers warrants to Evolution executives that can cause a dilution to shareholders of 1.6% + 0.9% if all warrants are exercised:

Evolution has diluted shareholders by 2.12% annually since 2015:

A dilution of ~2% is well within reason for a business that grows at Evolution’s rate. The warrants incentivize management to think long-term and create shareholder value.

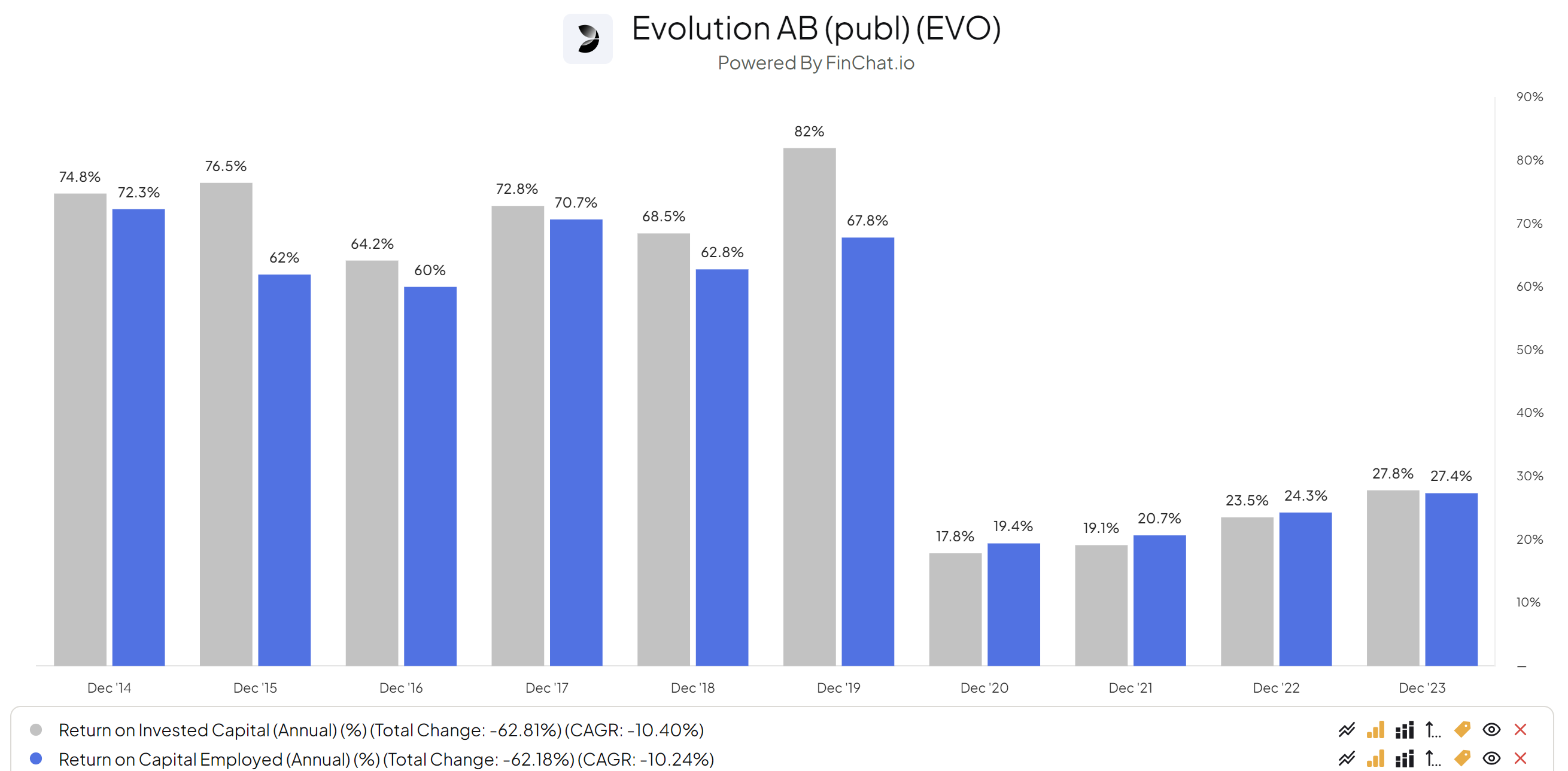

Does Evolution make an above-average return on its invested capital? 10/10

Yes, although taking a hit in 2020 after a poor acquisition, Evolution has demonstrated that its ROIC is above average for a sustainable period of time:

Combined score for the business model: 8.7

III) A strong competitive advantage 8.8

Moat source 8/10

Sufficient scale & economies of scale: Competitors are unable to drive the same profits from their live tables as Evolution. This is because Evolution has the best games, and can provide sufficient scale to each of the tables, resulting in close to maximum utilization of each live table. Setting up a live casino operation without sufficient scale provides bad unit economics, and hence it is hard to compete with Evolution. This is also why we don’t see many in-house operations for live casino tables.

Network effects: Evolution is the market leader and the preferred supplier for casinos worldwide. This also means that they can derive data from the largest pool of customers. At the end of the day, it is the gambler of the casino that decides what games he or she wants to play, and operators like Evolution must do everything in their power to keep the gambler’s attention to have profitable tables. This has been the case, and Evo has been diligent in using customer data to improve games & make new and exciting games.

Switching costs: Like most software solutions in a B2B setting, the switching costs are relatively high. Not only is there a direct cost of switching from Evo to another supplier (time, resource allocation, licenses), but there is also an alternative cost. If a customer of Evo were to change to a competitor, they would have to accept a lower engagement from its customers - so even if the take rate of the competitor is lower than Evo’s, the casino would end up losing revenue and earnings by switching to another supplier.

Moat strength 8/10

Evolution’s moat is underestimated, and we believe it is stronger than what is generally accepted in the market.

Widening or deteriorating? 8/10

Their innovative leadership keeps on widening, making it harder for new entrants. If it was easy to compete with Evolution (like most believe it is), there would be multiple competitors gunning for Evolution customers, and that is just not the case at the moment.

High and expanding margins 10/10

The results speak for themselves. The question for Evolution is rather: Will they be able to keep on expanding margins over time, or are they optimized?

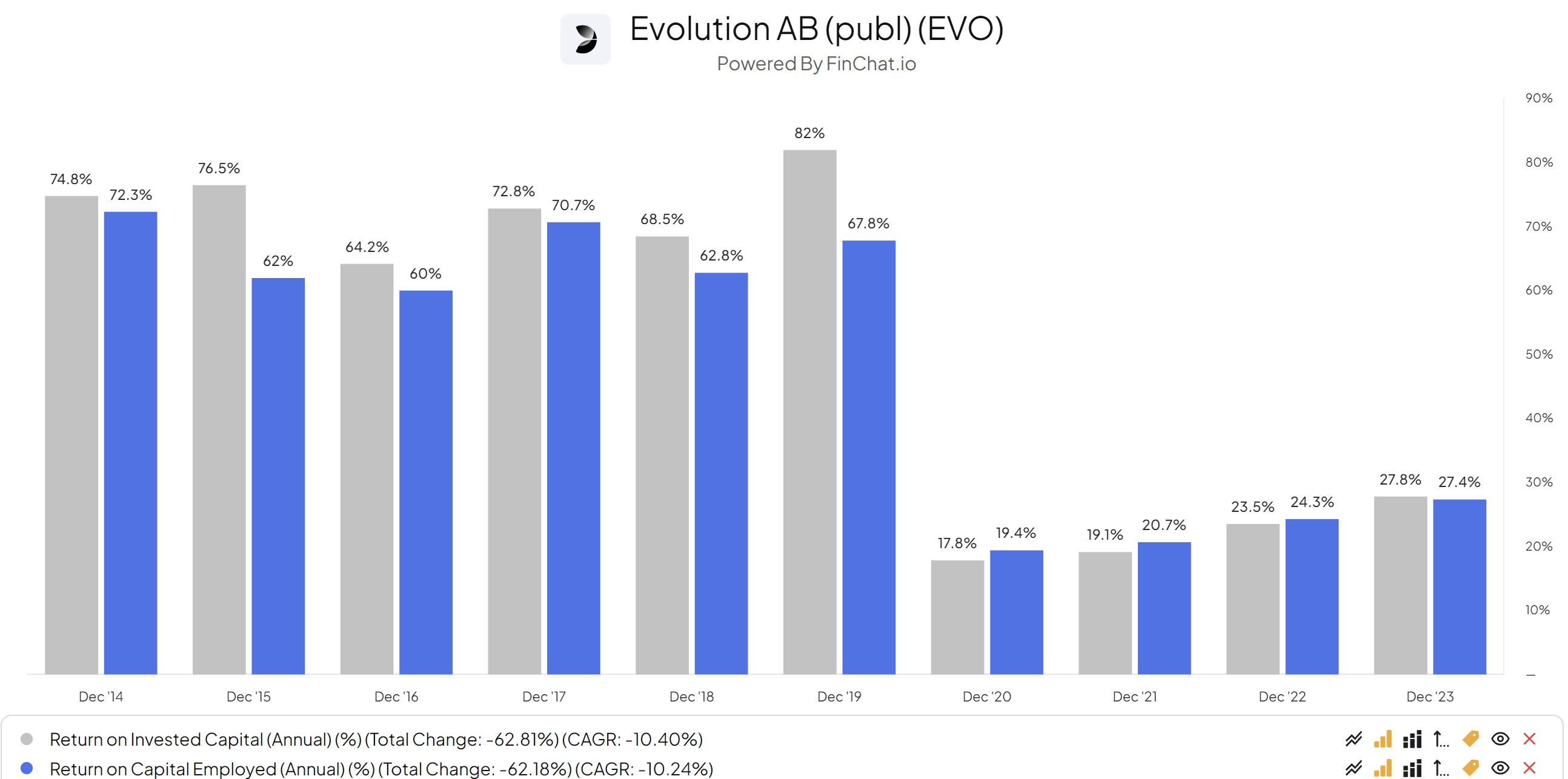

High ROIC over the industry to support moat? 10/10

Although Evo’s return on capital took a hit after their 2020 RNG acquisition, they are improving capital efficiencies over time, now closer to 30%.

IV) Growing demand for the product or service sold 8.6/10

Secular trend with +10% CAGR 8/10

Total gaming market has an estimated value of £450 billion, growing at 11% annually.

Total online gaming market has historically grown by 19% annually and is expected to grow by 12% annually.

Market gainer 9/10

Evolution is the market leader in Live while lagging in its RNG segment.

Evolution is gaining market share despite being the clear leader.

Growing revenue, earnings & cash flows at +10% annually 10/10

Historically, Evolution has compounded its per-share value significantly (+45% annually) since its IPO in 2015.

Analysts estimate Evolution to grow its long-term EPS by 18% annually.

Growth drivers 9/10

Number of engaging live games delivered

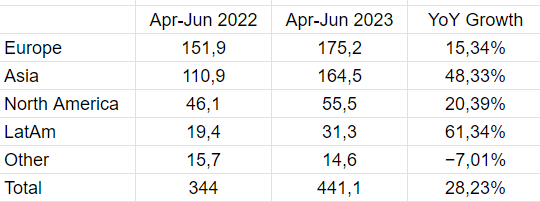

Untapped markets in the US, Canada, and Asia provide a significant upside opportunity if regulations allow it.

Scalable business model with one key constraint to look for: Evolutions ability to build new studies and hire and retain dealers.

Potential for global expansion 7/10

Already global exposure

Still plenty of room to grow into new markets such as NA & LatAm.

V) Risk factors 7.25/10

Company-specific risk factors 5/10

Regulatory changes - making online gambling illegal or restricted (Sin stock)

Unregulated markets - Evolution earns a significant percentage of its operating revenue from unregulated markets. Although these are unlikely to go away, they must be mentioned as a risk factor.

Crypto reliance allegations

CPO as a single point of failure - The CPO is considered the mastermind behind Evolution’s success, as the number of and engagement in their new games is a key growth driver. If the CPO were to quit, it could materially affect Evolution.

Slow down in sales 7/10

Evolution is transitioning from a high-growth stock growing at +40% annually to a more modest (still very high) growth of 15-25%. The slowdown is also tied to Evolution’s ability to build new studios as demand is still very high for their services.

Lower levels of disposable income mean less consumer gambling and less activity for Evolutions customers.

Balance sheet 10/10

Net cash position (-£906.3)

Debt to equity of 0.02

Cash on balance sheet of £985.76

Valuation risk 7/10

Forward PE 21

Forward POCF 18.2

Forward PFCF 20.7

Forward PS 11.2

Evolution is trading at a fair price compared to its historical average, and relative to other similar fast growers. The main risk is in its price-to-sales ratio, which is 11.2. Generally, a PS above 10 is a stretch, but it depends on the business. Evolution is very profitable, but if margins are challenged, this will pose a valuation risk for investors.

Deciding factor: Valuation 9/10

Our model suggests a 30-40% upside in the stock from current levels using conservative inputs.

Growth will be the deciding factor for the valuation moving forward.

Margin compression could cause the current estimate to be wrong. However, we don’t see any obvious red flags for Evolution’s margins.

Total Quality Growth score for Evolution: 8.44/10

Evolution gaming is a fantastic business at a fair price, but it is not without risks. Investors must be aware of risks that might cause our value estimate to be wrong, such as a slowdown in growth, compression of margins, or other company-specific risks materializing.

If you like this kind of post, please leave a ❤, and a comment, or reply to this email and let us know. We love your feedback!

Whenever you are ready, this is how I can help you:

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Essentials of Quality Growth — Join more than 250 investors who have bought the guide. Essentials of Quality Growth Investing is a multi-step guide for building a stock market portfolio of 10-20 high-performing quality compounders.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

(Free) How to analyze the financial statements — Learn how you read & analyze the balance sheet, income statement, and cash flow statement.

Promote yourself to +6.500 stock market investors (48% open rate) — Contact us via: investinassets20@gmail.com

Very well done,It Is important to be very detailes on risk and valuetion potwntial contraction