Novo Nordisk: Time to Buy the dip?💊

Why the stock is down -43% after its recent report 📉

Hi investor👋🏻

We wrote an article about Novo Nordisk a few months ago detailing the business and the investment case:

Our conclusion at the time was that the high quality diabetes and weight loss leader was somewhat overvalued.

After news broke of its recent report, the stock plunged -20%. The stock is now down ~-43% from its top. So naturally, we have to take another look to determine if the risks have materialized, or if the stock is now worth having in our portfolio.

Let’s get into it👇🏻

What’s Behind Novo Nordisk’s Stock Drop?

Novo Nordisk’s CagriSema Falls Short—Is the Market Overreacting?

Novo Nordisk’s highly anticipated CagriSema just wrapped up Phase 3 trials, posting an average weight loss of -22.7%—a solid result, but short of the -25% target. The market didn't take kindly to the miss, triggering a sell-off in Novo’s stock. But is the reaction justified?

Competition Heats Up: Zepbound vs. Wegovy

A recent head-to-head study comparing Novo’s Wegovy and Eli Lilly’s Zepbound revealed a surprising gap in effectiveness. Zepbound showed a -20.2% weight loss, significantly outperforming Wegovy’s -13.7%. This puts Lilly in a strong position to grab market share, raising concerns about Novo’s long-term dominance.

Wall Street’s High Expectations & Novo’s Valuation

Despite CagriSema delivering promising results, they weren’t quite strong enough for Wall Street’s lofty expectations. Add in Novo’s already-stretched valuation, and the reaction starts to make sense. Investors are now facing a new risk: increasing competition from Lilly, which could chip away at Novo’s dominance in the weight-loss drug market.

Was the Sell-Off Overdone?

A 2.3% miss on weight loss targets isn’t a disaster, but with high expectations baked into the stock price, any weakness gets magnified. While the long-term obesity drug market is still Novo’s to lose, competition is intensifying. Whether this dip is a buying opportunity or the start of a deeper correction remains to be seen.

Would you buy the dip, or is Novo’s run starting to slow down? Drop your thoughts below.

Why this dip might be a opportunity for long-term investors

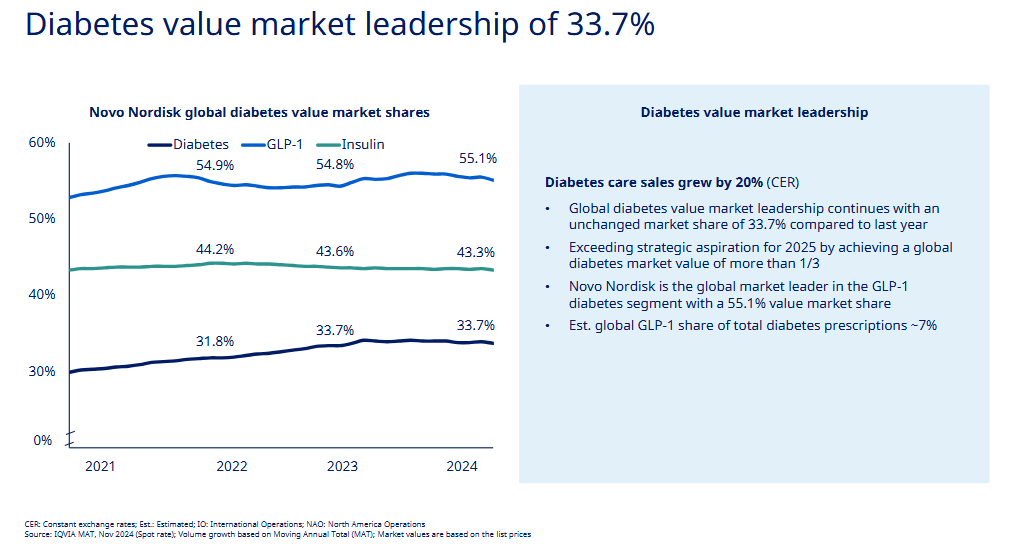

Novo Nordisk is still the market leader in diabetes and weight-loss drugs.

The company controls 55.1% of the GLP-1 market, 43.3% of the insulin market, and 33.7% of the Diabetes market.

Despite increased competition from Eli Lilly, Novo Nordisk’s market share remains stable.

The growing demand for these product is a driver for continued sales and growth in the years to come.

Novo Nordisk is ramping up its production capacity

Due to the growing organic demand for its products, Novo ramped up investments in 2024 to meet the demand and improve its supply chain.

Novo are building a new 170.000 square meter production facility in Denmark, and expanding its production facilities in Brazil, France, China, and the US.

Sustainable growth & high solid margins

The business guides for revenue growth of 16% - 24% with operating income increasing 19% - 27%.

Novo’s gross margins remain stable at 85% (!), operating margins at 48.2% and free cash flow margins at 25.4% (FCF margin is lower due to the increased Growth CapEx investments).

Analysts expect Novo to grow significantly in the coming years with the following estimates:

A forward PE of 22.2x is a fair price to pay for a potential multi-year growth story like Novo Nordisk. The valuation has come down after it reached an all time high of DKK1002 in June of 2024.

3 Biggest Risks for Novo Nordisk Investors

Eli Lilly’s Growing Threat: Novo has led the weight-loss drug market, but Lilly’s Zepbound is outperforming Wegovy in studies. If Lilly keeps gaining ground, Novo’s dominance and pricing power could take a hit.

Production Bottlenecks: Demand for GLP-1 drugs is growing, but Novo can’t scale production fast enough. Supply shortages could slow revenue growth and push patients toward alternative products.

Regulatory & Insurance Risks: Governments and insurers may limit coverage for weight-loss drugs, making them less accessible. Plus, regulatory delays (like FDA approval for Awiqli) could stall Novo’s expansion.

Novo is still a powerhouse, but these risks could shake up the long-term outlook.

Valuation: Buy the dip?

The LTM PE and P/OCF has reached levels close to their 5 year lows.

This does not mean it can’t go any lower, but the risk is significantly lower now than when PE was at +50x LTM.

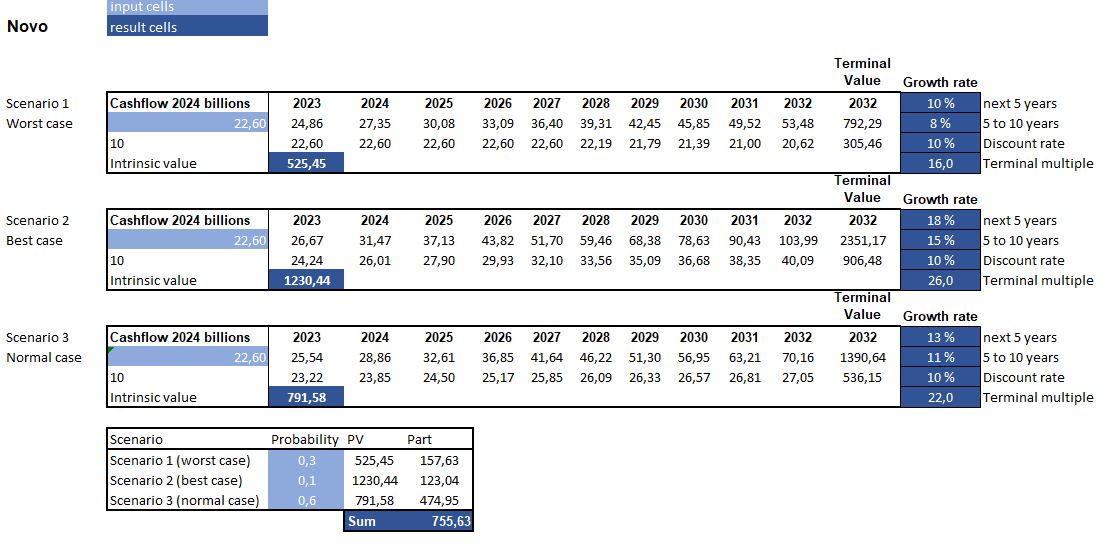

Using a simple discounted cash flow model with 3 different scenarios, we believe Novo Noridsk is undervalued.

The inputs used are earnings per share of DKK22.60.

The growth inputs are reduced somewhat from our previous analysis to reflect the risk of increased competition and potential market share loss.

Current price: DKK587

Fair value: DKK755.63

Upside: +28.72%

Suggested CAGR from normal scenario: 14%

Final thoughts

Novo is currently in a strong down trend that could continue. Therefore, it might be wise to plan out purchases tactically if you want to take a position.

A good strategy is to plan for 3-4 purchases of equal size and purchase at different times. If the price continues to fall, you get a better price for each purchase. If the price goes up, you might want to keep purchasing regardless—but whos complaining about making money?

Here are some price levels that have shown resistance in the past:

Do you want to follow our market-beating quality growth portfolio? You should join the premium newsletter where we provide detailed valuation breakdowns of high quality stocks:

Read more about premium here.

Whenever you are ready, this is how I can help you:

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Essentials of Quality Growth — Join more than 250 investors who have bought the guide. Essentials of Quality Growth Investing is a multi-step guide for building a stock market portfolio of 10-20 high-performing quality compounders.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

(Free) How to analyze the financial statements — Learn how you read & analyze the balance sheet, income statement, and cash flow statement.

Promote yourself to +10.000 stock market investors (45% open rate) — Contact us via: investinassets20@gmail.com

Interesting article.

Have you performed a DCF calculation to determine whether the current valuation is worth buying or not?

Great stuff, thanks. Restacking.