My 6-step checklist to build a $100,000+ stock portfolio in 2026 📈

Most investors start with valuation. That's the wrong first question. Here's what to do instead.

Hi investor👋

You have already made the most important decision.

You are not here asking whether you should invest. You are ready to get started.

Let’s make a few assumptions:

You have ~$10,000 ready to put to work

You are willing to add $1,000 every month until you get there.

The only question left is how to do it right.

Let us run the numbers first. Starting with $10,000 and adding $1,000 per month, you need roughly 15% annualised returns to hit $100,000 in around 5 years. That is a real number. Not guaranteed, but absolutely achievable with a disciplined process.

I know because I started my own stock portfolio in 2014 with less than $1000.

Here is exactly how I would approach it if I were starting today.

Step 1: Pick your investing style, learn it deeply, and set your criteria ✅

Before you buy a single share, you need to decide what kind of investor you are going to be. Not what sounds impressive at a dinner party (Like investing in the next big thing). What you will actually stick to when your portfolio is down 50% and every instinct tells you to do something.

There are three realistic options for an individual investor starting where you are.

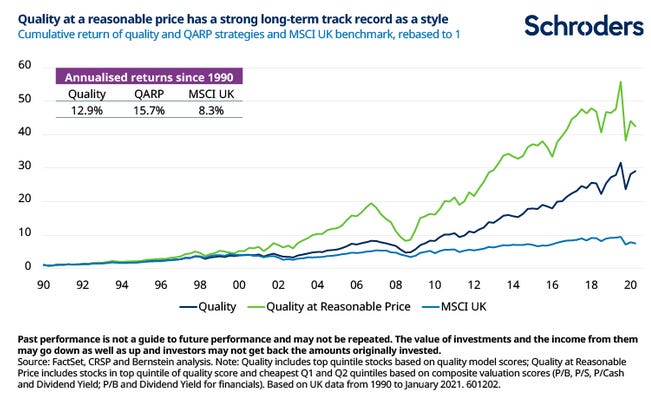

Quality growth investing. You buy exceptional businesses with durable competitive advantages and high returns on capital, hold them for years, and let compounding do the work. This is my approach. It requires patience and the ability to sit through volatility without panicking.

The investing style has performed well over the long-term and have many psychological advantages that makes investing less stressful (I wrote a book on quality growth investing if you’re curious).

Index investing. You buy a low-cost ETF tracking the S&P 500 or MSCI World, add your $1,000 every month, and accept market returns. This beats most active investors over time. If you are not willing to put in genuine research hours every week, this is the right answer and there is no shame in that.

This strategy has been amazing over the past 10-20 years, but at the current valuation I have strong doubts that you will see the same returns from investing in an index fund as you have in most recent history.

A hybrid approach. You put 60-70% into a core index ETF and deploy the rest into your highest-conviction individual stock ideas. You get a safety net while building real stock-picking skills.

The worst outcome is mixing approaches reactively. Buying index ETFs when you are nervous, switching to individual stocks when you feel confident, and never developing real competence in either.

Pick one. Write down your strategy and allocation, and define your criteria in advance.

There are hundreds of other investing strategies that can work: value investing, micro cap investing, growth investing and so on. Pick what suits your temperament and curiosity the most.

Your buying criteria should answer:

What kind of business qualifies?

What financial characteristics must it have?

What price is too high to pay regardless of quality?

Your selling criteria matter just as much. Write these down before you buy anything. Common and valid reasons to sell:

The original thesis has broken, a clearly better opportunity exists elsewhere, the position has grown so large it creates unacceptable risk, or you simply made a mistake and the business is not what you thought. Price going down is not a selling reason. The business getting worse is.

This is easy in theory, but hard in practice. I’ve had my fair share of mistakes from thesis drift in the past myself.

Having these written before the market turns volatile is what separates investors who build a system around their portfolio and compound over decades, and those who have an occasional good year with inconsistent returns.

Build a Market-Beating Portfolio of Quality Compounders, Now 30% Off

Many world-class compounders are currently trading at multi-year low levels. We do the work to identify the few that truly matter, businesses with durable moats, high returns on capital, and long reinvestment runways.

Inside the Premium service, you get:

📜 A repeatable investing framework you can use to compound effectively

💎 Full access to the Quality Growth portfolio

📈 Clear buy & sell alerts

🌍 Access to the Quality Growth investable universe and watchlist

📚 Deep dives on compounders that focus on the most important factors

Get 30% off before the price hike, and start building a portfolio designed to outperform over the next decade.

Don’t overcomplicate it. Own better businesses. Let time do the work.

Step 2: Learn to identify great businesses✅ (Dont start with valuation)

This is where most new investors go wrong. They open a stock screener, sort by P/E ratio, and ask “is this cheap?” That is the wrong first question.

Quality comes first. Valuation comes later.

A mediocre business at a cheap price is still a mediocre business. An exceptional business at a fair price can compound wealth for decades. The order matters enormously.

So what makes a business genuinely great?

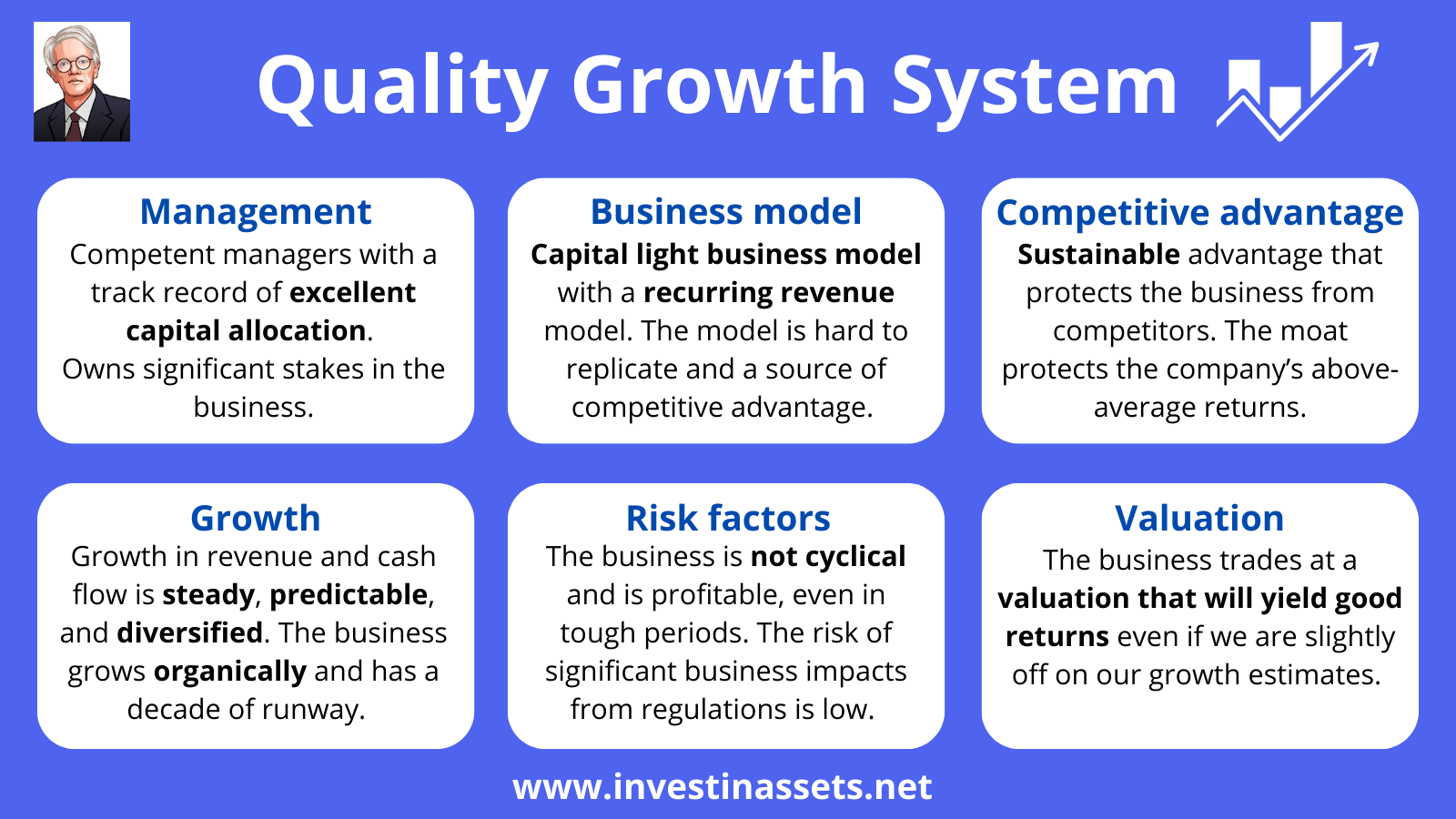

There at Invest in Quality, we look at 6 pillars:

Honest, capable management.

Read five years of annual reports. Do they do what they said they would do? Are they candid about mistakes? Do they own meaningful amounts of stock? Are they buying back shares when the price is cheap or issuing new shares when the price is high? Actions reveal character far more reliably than words.

Here are 5 great founder-led businesses:

Business model

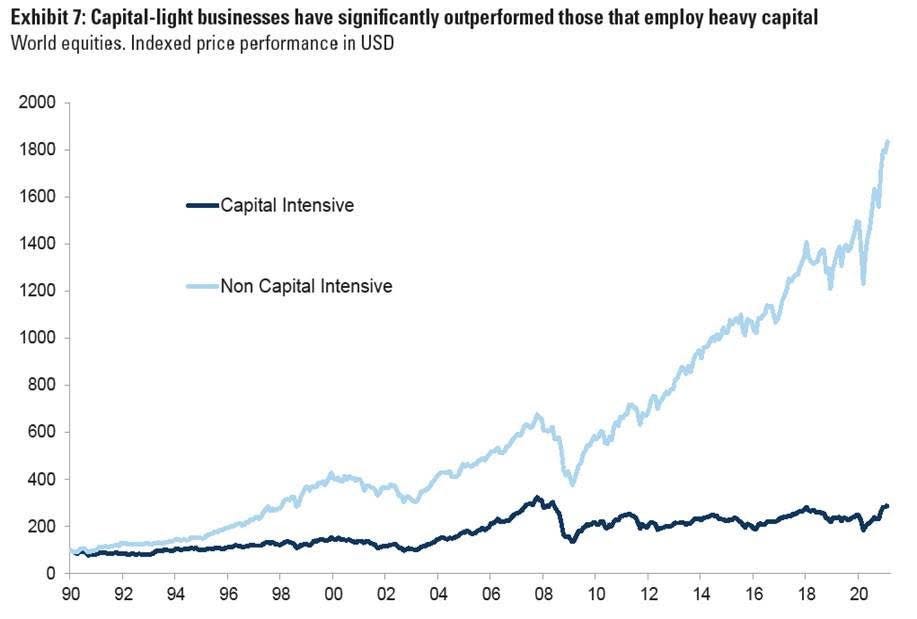

The best businesses don't need to constantly fight for every dollar of revenue. They've built models that are capital light. This means they can grow without endlessly reinvesting heavy amounts back into the business. They often collect recurring revenue from customers who come back year after year. When a business model is also hard to replicate, it becomes a source of durable competitive advantage in itself.

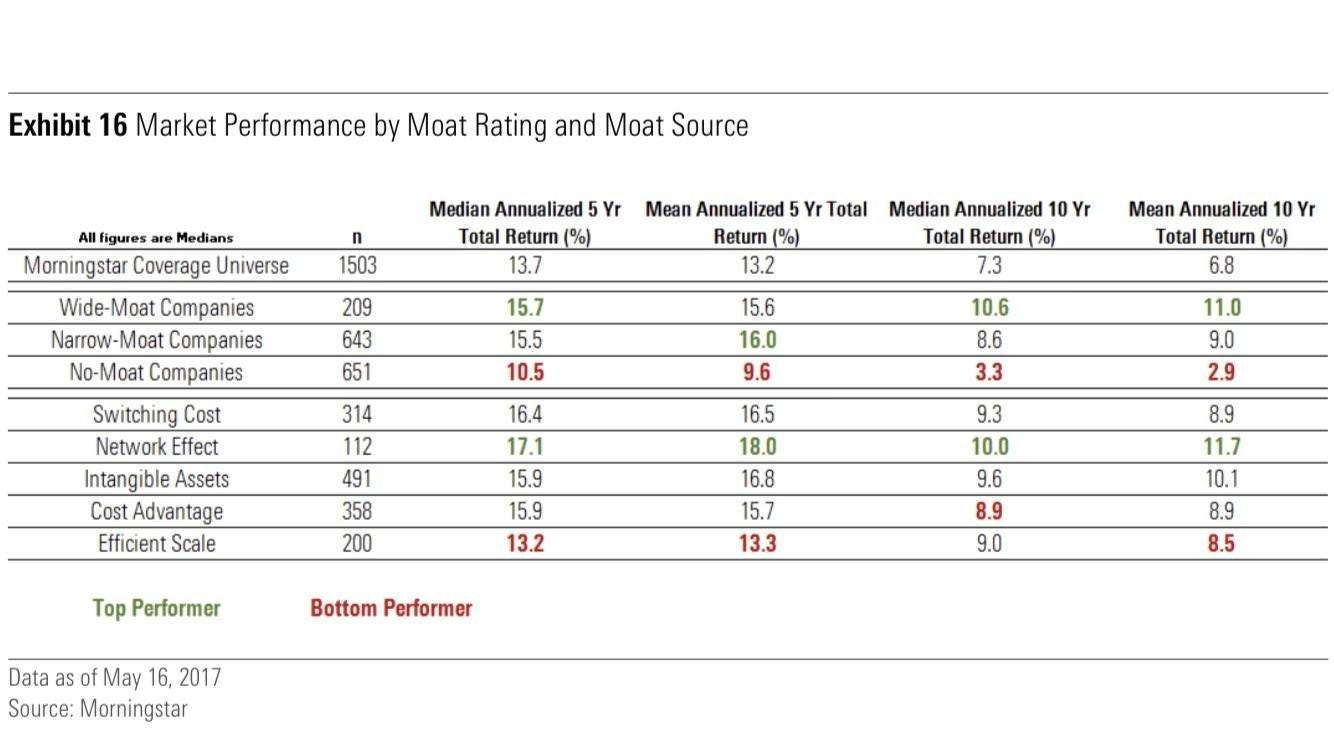

A sustainable competitive advantage.

Something structural that protects those returns from competition over time. The most durable moats are network effects (Mastercard becomes more valuable to cardholders every time a new merchant joins, and more valuable to merchants every time a new cardholder joins), switching costs (once a local government agency runs on one of Constellation Software’s VMS businesses, the cost and risk of switching is enormous and costly), cost advantages at scale, and intangible assets like brand or regulatory licences that take decades to build.

Growth

We’re not chasing hypergrowth stories that depend on a single product or a single market. We want growth that is steady, predictable, and diversified. The kind that shows up reliably in both good years and bad. Organic growth is especially valuable because it signals that customers genuinely want more of what the company offers, not that the business is buying growth through expensive acquisitions. A decade of clear runway ahead means the compounding has plenty of room to run.

Risk factors

Every business carries risk, but not all risks are equal. The businesses we want to own are non-cyclical, or at least less prone to the economic cycle (No business is completely non-cyclical).

These businesses are profitable even through tough periods, which means they don’t need external capital to survive a downturn. And crucially, they operate in industries where regulation is unlikely to suddenly change the rules of the game. We’re looking for businesses that sleep well at night, so you can too.

And, ultimately, we want to look at the valuation:

After all pillars check out, valuation becomes the final question. Notice that it’s the last question, not the first. We’re not looking for a bargain-bin price. We’re looking for a price that makes mathematical sense: one where even if our growth estimates are a little optimistic, the returns will still be solid. A quality business bought at a fair price beats a mediocre business bought at a cheap price almost every time, over the long run.

A simple starting filter:

5 year ROIC of +15%

5 year revenue growth of +10%

Stable or expanding operating margin

The list will be short. Everything on it is worth understanding much more deeply.

Step 3: Build a focused portfolio of high-conviction ideas that fit your style ✅

You do not need 30 stocks. You need 10 to 15 businesses you understand so well that you could explain each one without looking anything up. The moat, the growth drivers, the key risks, and why you still own it despite those risks.

With $10,000 to start, I would build positions in 5 to 7 businesses initially and expand toward 10 to 15 as your monthly contributions accumulate. Starting too diversified means your winners cannot meaningfully move the needle, and you never develop genuine depth of knowledge in anything you own.

Concentration is not recklessness. It is conviction. The investors who build serious wealth over time own fewer things, not more. Knowing what you own means you can hold through volatility instead of selling at the exact wrong moment.

A practical structure for your starting position: your top 3 ideas get the most capital, roughly 15-20% each. Your next 4-6 ideas get 5-10% each. Keep a small cash position of 5-10% to deploy when quality businesses go on sale, which they do regularly and for reasons that have nothing to do with the underlying business.

When your $1,000 monthly contribution arrives, direct it toward whichever position currently offers the best combination of conviction and value. Not necessarily the one that has fallen the most. The question is always: where does the next dollar work hardest?

One rule worth writing on a card and keeping at your desk: if you cannot write three paragraphs explaining why you own something without looking anything up, you do not know it well enough to own it. Owning things you do not understand means fear fills the gap that knowledge should occupy. You will sell at exactly the wrong time.

Step 4: Valuation. Is this the right time to buy? ✅

You have identified a great business. Now the question is: at what price does it become a good investment?

Even exceptional businesses can be poor investments if you overpay. A company growing earnings at 15% per year is still a disappointing investment if you paid a price that assumed 25% growth indefinitely. Valuation does not change the quality of the business. It determines the return you will earn from owning it.

My approach is a simple three-scenario framework. I model what I think the business looks like in 5 years under a bear case, a base case, and a bull case. For each scenario I estimate revenue, margins, and earnings. Then I work backwards: what price would I need to pay today to earn a 12-15% annualised return in my base case?

If the current price requires the bull case just to earn a fair return, I wait.

A few practical tools worth learning properly:

Free cash flow yield. Take the free cash flow per share and divide by the stock price. A FCF yield of 4-5% on a high-quality compounder growing at 12-15% is often attractive. A FCF yield of 1-2% on a slower grower usually is not.

Many investors like to compare the free cash flow yield with the risk free rate, which usually means the US 10 year treasury yield (Currently 4.285%). This is the yield you can get risk free. Is the investment worth it with all its inherent risks if you get a FCF yield below this level? That is the game.

Here is Novo Nordisk’s FCF yield, going from an unattractive range of ~1.5%, to 5.5%:

Price-to-earnings relative to growth (PEG ratio). Divide the P/E by the expected earnings growth rate. A PEG below 1 on a quality business is worth looking at seriously. Above 2 requires confidence in the growth trajectory and the sustained quality of the business (ROIC and margins holding up).

5 businesses with a PEG of <1 according to Fiscal.ai:

Nvidia NVDA 0.00%↑

Taiwan Semiconductor TSM 0.00%↑

Samsung Electronics $SSNL.F

Eli Lilly LLY 0.00%↑

Micron Technology MU 0.00%↑

Owner’s earnings yield. Take net income, add back depreciation and amortisation, subtract the maintenance capital expenditure required to sustain the current business. Divide by market cap. This strips out accounting noise and tells you what the business actually earns for owners in cash terms. It is Buffett’s preferred measure and it is worth understanding.

The downside with owner’s earnings is that most companies don’t disclose what capital expenditure it needs to maintain the business, and what is for growth initiatives, so it has an element of subjectivity.

The goal is not to find the perfect entry point. The goal is to avoid paying prices that guarantee disappointment, and to act decisively when high-quality businesses go on sale.

So, to keep things simple:

A business with a FCF yield / Owner’s earnings yield above the risk free rate, and with a PEG close to 1 is very attractive.

Caveat: Many businesses with a PEG close to 1, will have a low FCF yield because it is in a growth phase, investing a lot in growth initiatives through CapEx. This suppresses FCF significantly.

Step 5: Create a real system for buying and selling ✅

The biggest destroyer of long-term returns is not picking the wrong stocks. It is making emotional decisions in the absence of a framework.

You need a written system. Before you deploy any capital, write down the answers to these questions for each position:

Why am I buying this business?

What would have to be true for this to be a +15% compounded annual growth rate return over 5 years?

What are the three biggest risks to the thesis?

What specific events or data points would cause me to sell?

What is my maximum position size?

When the stock drops 25% in a month and it will, at some point, you do not have to make a decision under pressure. You return to the document and ask: has anything on this list changed? If nothing has changed, hold or add. If something has changed, reassess.

For buying: deploy capital in tranches, not all at once. When a business you want to own reaches a fair price, start a position with 1/3 or 1/4 of your intended allocation. If it continues to fall and the thesis remains intact, add the rest. This removes the paralysis of trying to time a perfect entry.

For selling: set a high bar. Selling because a stock has gone up a lot is one of the most expensive mistakes long-term investors make. The real compounding happens in the later years of ownership. Sell when the thesis breaks, when you find a clearly superior alternative, or when the position has grown so large it creates genuine risk for your overall financial situation.

For example, I sold my Apple position in 2018 because I felt the valuation was stretched:

For your $1,000 monthly contribution: make this decision analytically, not emotionally. Every month, look at your watchlist and your existing positions. Where is the highest-quality business trading at the most attractive price relative to what it is worth? That is where the new capital goes. Some months that is adding to an existing position. Some months it is starting a new one. The decision should always be rational.

Step 6: Track what matters. Build your investor dashboard ✅

Most investors track the wrong thing. They check their portfolio value every day, watch it move up and down, and make themselves anxious and reactive. The daily number is almost entirely noise.

What actually tells you whether you are succeeding is different.

What to track for your portfolio:

Your CAGR since inception, updated monthly. This is the number that tells you whether the strategy is working over time. Short-term performance is almost meaningless on its own.

But even CAGR over a few years can be misleading, it is far better to find a proxy for your portfolio that tells you more about how well the businesses are performing. A proxy that Warren Buffett used when he ran Berkshire was ‘look-through’ earnings. It is simple: The amount of shares you own of a stock multiplied with the earnings per share. Then you get a earnings proxy of what your portfolio is making. This should be tracked over the years to see if it is growing.

If look-through earnings is up 16% CAGR, but stock price is only up 10% CAGR, you can argue that the growth in earnings is more important for long-term returns.

What to track for each business:

This is where most investors stop short, and it is the most important part of the whole process. Build a simple Google Sheets tracker with one row per company. Update it after every quarterly earnings report. You are looking for trends, not perfection.

Here’s what I track:

Revenue growth

Earnings per share growth

Free cash flow per share growth

ROIC/ROCE/ROE

Gross & operating margins

Net debt to free cash flows

Interest Coverage

Change in shares oustanding

A business where revenue growth is slowing, margins are compressing, and ROIC is declining deserves serious scrutiny even if the stock price has not moved yet. The fundamentals lead the stock price, not the other way around.

The proxy that matters most: for each business you own, identify the one metric that is the clearest signal of whether the thesis is working. For a payments business like Mastercard, it is payment volume growth. For an industrial compounder like CSW Industrials, it is organic revenue growth and EBITDA margin trend. For a software business, it is net revenue retention. Know the proxy. When that number deteriorates, everything else deserves a second look.

What to ignore entirely: daily price movements, macro predictions, whether the market is expensive in aggregate, and what other investors are doing. None of these determine your long-term outcome. The quality of the businesses you own and the price you paid for them does.

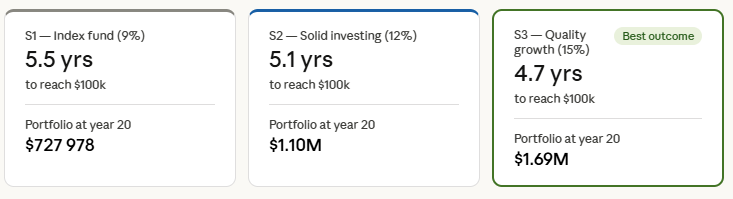

How long will it actually take?

Let us run the real numbers on your situation. Starting with $10,000 and adding $1,000 every month.

We have 3 scenarios, index investing at 9%, investing in stocks with a 12% annual return, and Quality Growth investing with a 15% CAGR:

Now, the difference is not huge to get to your first $100k. With a 9% return it takes 5.5 years, 12% return it takes 5.1 years, and 15% it takes 4.7 years.

This is because what you invest every month at this point is more important than getting a few more percentages of return.

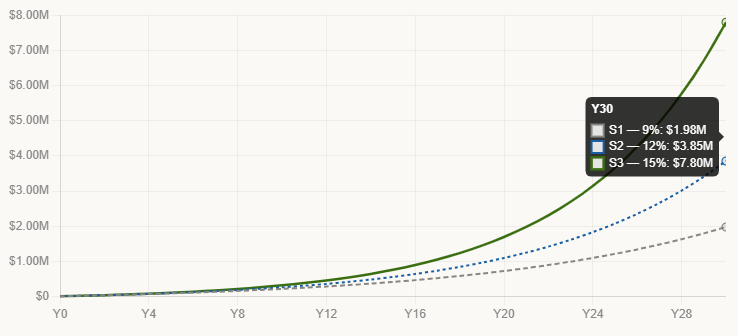

The interesting effect happens later in the compounding journey. Just look at the difference after 20 years:

8% CAGR: $727k

12% CAGR: $1.1M

15% CAGR: $1.69M

The real magic of compounding happens in the really long-term.

This is the difference after 30 years:

The first $100,000 is the hardest part. Every month your contributions represent a large share of the total. Once you get there, compounding starts doing more of the work than you do. The journey from $100,000 to $1,000,000 is where the real magic of long-term investing becomes visible.

Remember what Charlie Munger said:

The honest truth about getting there

The checklist is simple. Following it is not.

March 2026 was a brutal month for my portfolio. Everything was down. Many of my holdings saw drops of more than 10%. Nearly every position faced selling pressure.

But I kept buying.

Not because I am reckless or indifferent to losses. Because I know what I own, I know why I owned it, and I know exactly what would actually make me sell a position. The prices told me the market was anxious. The businesses fundamentals told me nothing had changed except the markets emotional state.

This is the game of investing.

Build the system before you need it. Follow it when it is uncomfortable. Let compounding do the rest.

The $100,000 is not the destination. It is where the real ‘joys of compounding’ journey begins.

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Built something I think you’ll find useful: https://automatedalpha.substack.com/p/i-reverse-engineered-the-buffettmunger

👍