How I Save 10 Hours of Investing Work Each Week Using AI

The exact workflows that replaced my most time-consuming research tasks

Hi there, investor! 👋

I used to spend most of my investing time on work that didn’t require me.

Reading through earnings releases line by line. Scrolling through 300-page annual reports hunting for the three paragraphs that actually mattered. Manually comparing numbers across quarters to spot a trend I could have seen in 30 seconds with the right tool. Summarizing earnings call transcripts just to arrive at a conclusion I could have reached faster.

That was the job. And most of it was grunt work.

I still do all of those things. I just don’t spend 10 hours a week doing them anymore.

This article is about exactly what changed, the specific workflows, the exact prompts, and the places where AI will mislead you if you’re not paying attention.

Read my previous article on how to set up Claude as your personal AI investment analyst here:

Let’s get into it 👇

First: What those 10 hours actually look like

If you run a concentrated portfolio of quality compounders seriously, meaning you actually read filings, track your thesis per holding, and think carefully before you act, your weekly research time probably breaks down something like this:

Earnings processing (releases, transcripts, filings): 3–4 hours

Annual report deep dives on new or existing positions: 2–3 hours

Monitoring existing holdings across quarters: 1–2 hours

Research on new ideas: 2–4 hours

Cutting through macro and sector noise: 1 hour

That’s 8–14 hours per week for someone doing this properly. Most of it is preparation: gathering, formatting, summarizing, comparing. Almost none of it is the actual thinking that drives investment returns.

The goal isn’t to do less. The goal is to spend those hours on judgment instead of formatting.

The mindset shift that makes this work

Before we get into the workflows, this needs to be said clearly.

Claude is not an analyst. It has no skin in the game, no track record, and no judgment built from watching businesses succeed and fail over decades. It has read everything and experienced nothing. It will give you a confident-sounding answer whether it knows what it’s talking about or not.

What it is (when used correctly) is the fastest research preparation tool that has ever existed for individual investors.

Think of it this way. The 10 hours you’re about to reclaim are hours that never required your judgment in the first place. What remains is the conviction calls, the thesis judgments, the decision to hold through a painful quarter or sell when something has broken in the business, those still take exactly as long as they should. AI should not touch those decisions.

The job of AI in your investment process is to handle the preparation so you can spend more time on the thinking. Keep that distinction sharp at all times, and this becomes enormously useful. Blur it, and you’ll make worse decisions than you did before.

Caveat: There is a value to reading all the documents yourself, you might find something that AI misses. So let me be clear, the best possible scenario is that you do everything yourself. But let’s be real, very few have the time, the discipline, and the fortitude to do that consistently over time. I prefer to spend my energy and cognition where it matters most: Judgement around specific investment decisions.

Workflow 1: Processing earnings in 20 minutes instead of 2 hours

Saves approximately 2–3 hours per week during earnings season

Earnings season is the most time-intensive period in any fundamental investor’s calendar. You own 12-20 positions. Each one reports. Each report has a press release, a set of financials, and a +60-minute earnings call transcript. Doing this properly, the old way, takes hours.

Here’s the new way.

What you do: Paste the documents of the earnings press release and the full earnings call transcript into Claude. Before you do, paste your investment thesis for that holding, the reasons you own it and the specific metrics you’re watching. Then run this prompt:

PROMPT 1: Earnings Processing

You are analyzing an earnings report for a company I own in my long-term quality growth portfolio. I am going to give you three things: my original investment thesis, the earnings press release, and the earnings call transcript. Your job is not to tell me whether the stock is a buy or sell. Your job is to help me understand whether my thesis is intact.

Here is my thesis for [COMPANY]: [Paste your thesis — 3–5 sentences on why you own it and what has to be true]

Here is the earnings press release: [Paste]

Here is the earnings call transcript: [Paste]

Please give me the following, structured clearly:

1. THESIS CHECK: For each assumption in my thesis, tell me whether this quarter confirmed it, contradicted it, or gave no clear signal either way.

2. NUMBERS THAT MATTER: Pull out the 5–6 metrics most relevant to my thesis. Show me the current quarter, the prior quarter, and the same quarter last year. Flag any meaningful changes.

3. LANGUAGE SHIFTS: Compare the tone and specific language used by management this quarter vs. what I would expect from a business performing well. Flag any topics that received noticeably more or less emphasis than usual, any hedging language, or any guidance that was vaguer than in prior periods.

4. WHAT I SHOULD THINK ABOUT: Based purely on the information in these documents, not your own opinion about the company, what are the two or three questions a long-term investor should be sitting with after this report?

Do not give me a buy or sell recommendation. Do not tell me what the stock might do. Focus entirely on the business.

What this looks like in practice

When Constellation Software reported Q1 2026, I pasted my thesis, which centers on their ability to deploy capital at high returns through vertical market software acquisitions, sustain mid-single-digit organic growth, and grow free cash flow per share over time by +15% annually alongside the release and transcript.

Claude flagged immediately that organic recurring revenue growth had decelerated to approximately 4%, that management used notably more cautious language around M&A multiples than in prior calls, but that free cash flow available to shareholders had jumped 44% and the acquisition pipeline commentary remained constructive. It surfaced exactly the tension I needed to think about, in about four minutes.

What you still do yourself

Decide what the verdict means for your position. Claude told me organic growth was decelerating. It cannot tell me whether 4% organic growth at Constellation Software is a problem or a feature of their model at scale. That judgment is mine, built from years of following the business.

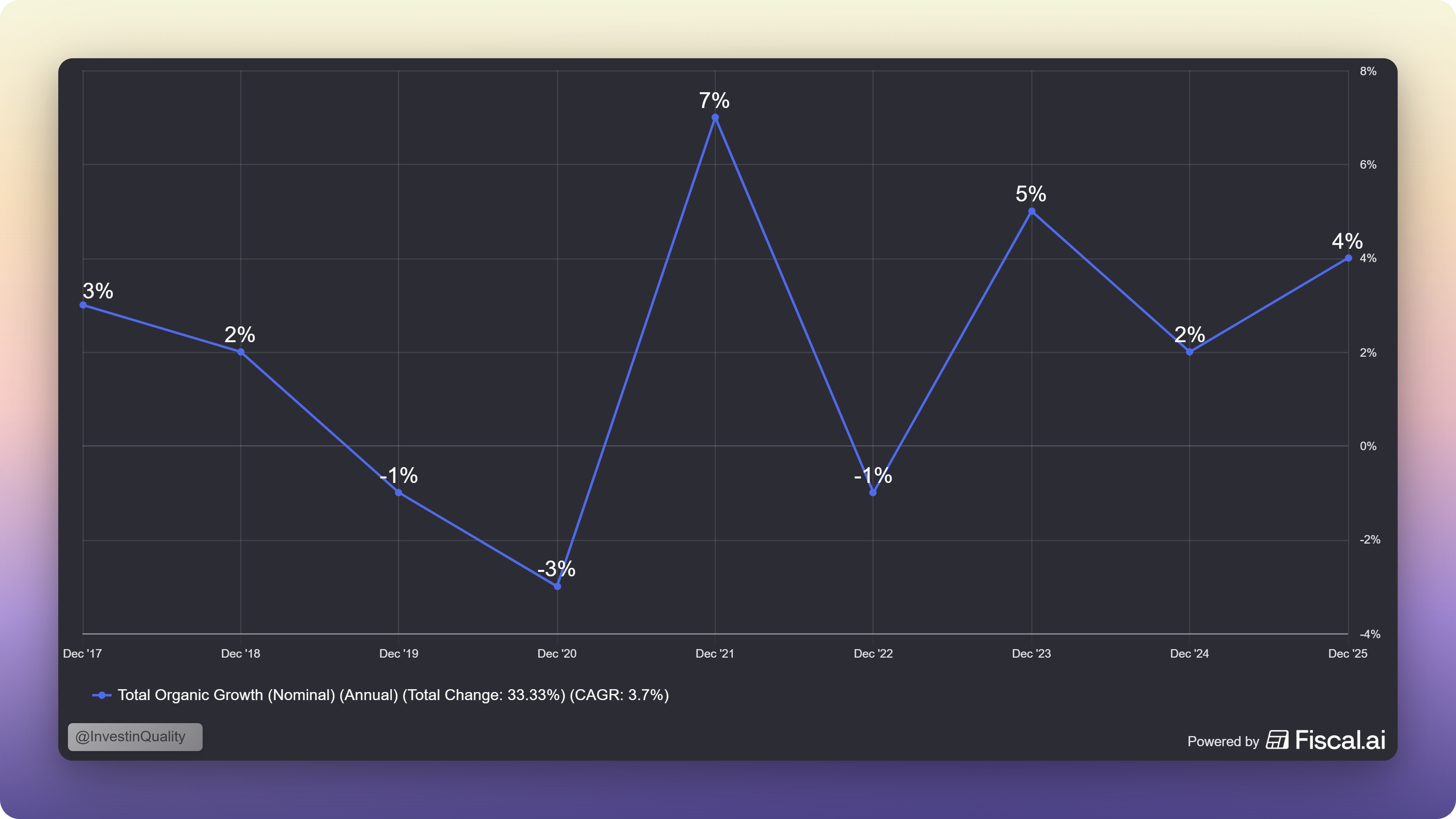

Looking at the data since 2017, a 4% organic growth is actually in the higher range of what Constellation has delivered:

Where this goes wrong

Claude will sometimes misread numbers from a pasted document, particularly when tables are involved. Always verify the specific figures it pulls against the actual press release. Never trust a number Claude gives you without checking the source.

Workflow 2: Annual report deep dives in under an hour

Saves approximately 2 hours per company

The annual report is the most important document a public company produces. It is also, for most companies, 80% repetitive. Risk factor sections that haven’t changed in four years. Legal disclosures. Compensation tables. Pages of accounting policy notes that apply to almost no investment decision you will ever make.

The skill in reading an annual report is knowing what to look for. Claude doesn’t develop that skill for you, but once you have it, Claude can find the relevant sections faster than any human.

What you do: Upload the annual report PDF directly into Claude, or paste the sections most relevant to your analysis. Then run this prompt:

PROMPT 2: Annual Report Deep Dive

I am a long-term quality growth investor analyzing the annual report for [COMPANY]. I am going to upload the full report. I want you to help me extract the information most relevant to a fundamental long-term investor.

Please work through the report and give me the following:

1. BUSINESS MODEL CLARITY: In 150 words or fewer, explain how this business makes money, who its customers are, and what makes them come back. Use only the language from the report, do not add your own assumptions.

2. ROIC AND CAPITAL ALLOCATION: Find every reference to return on invested capital, return on equity, capital expenditure, acquisitions, and buybacks. Summarize how management is allocating capital and whether there is any commentary on the returns they expect from that allocation.

3. COMPETITIVE POSITION: Pull the specific language management uses to describe their competitive advantages. Do not paraphrase, quote the exact phrases they use. Then flag any language that sounds defensive, hedged, or notably weaker than you would expect from a business with a strong moat.

4. RISK FACTORS THAT ARE ACTUALLY NEW: Compare the risk factors section against what a standard company in this industry would typically disclose. Flag any risks that appear specific to this company’s current situation, not generic industry risks that every company lists.

5. WHAT CHANGED FROM LAST YEAR: If I provide last year’s annual report as well, identify the three to five most meaningful changes in language, emphasis, or disclosure between the two years.

Flag any sections where the document quality made it difficult to extract reliable information.

What this looks like in practice

When I was going deeper on MercadoLibre ahead of their Q1 2026 results, I used this prompt against their most recent 20-F. Claude pulled out the specific language management used around their fintech flywheel, the way Mercado Pago and the credit business reinforce the commerce platform, and flagged that the risk factor language around credit portfolio quality had become meaningfully more specific than in the prior year’s filing. That was a signal worth investigating further. It would have taken me two hours to find it manually. It took Claude four minutes.

What you still do yourself

Evaluate whether what Claude found is good or bad. It can tell you that credit risk language became more specific. It cannot tell you whether that reflects prudent disclosure or a genuine deterioration in the underlying portfolio. That requires your own judgment, your own reading of the fintech lending environment, and your own view of management’s track record.

Where this goes wrong

Two places. First, Claude sometimes misreads PDFs, particularly tables, footnotes, and anything in a non-standard format. Always check the numbers it extracts against the source document.

Second, and more importantly: Claude has a bias toward sounding thorough. It will give you a confident summary even when the source material is ambiguous or the answer isn’t clear. If you ask it whether the competitive position is strong, it will give you a structured answer. That answer may or may not reflect reality. The confidence of the output is not evidence of its accuracy. Read the sections that matter yourself. Use Claude to find them faster.

Workflow 3: Monitoring your existing holdings without drowning

Saves approximately 1–2 hours per week

This is the part of investing that almost no one covers, and the part where most individual investors are genuinely weakest. Not finding stocks. Holding them.

You own a portfolio of stocks. Each one has a thesis. Each one reports every 90 days. The question every single quarter is the same: did anything change? And it’s hard to answer consistently, because your memory of why you bought something three years ago is imperfect, and the quarterly noise makes it easy to drift from your original reasoning without noticing.

The solution is a thesis document for each holding that you update quarterly. Claude makes this both easier to build and faster to use.

Step one: Build the thesis document. For each holding, run this prompt:

PROMPT 3A: Extract My Core Thesis Assumptions

I own [COMPANY] as a long-term holding in my quality growth portfolio. Here is why I bought it: [Paste your original investment notes, even if rough]

Based on what I’ve written, identify the three to five core assumptions that have to be true for this investment to work out over a five to ten year horizon. Be specific, not “the business needs to keep growing” but the actual mechanisms and metrics that would tell me whether the thesis is intact or broken.

For each assumption, tell me: what would confirming evidence look like in a quarterly earnings report? What would contradicting evidence look like?

Present this as a structured checklist I can use every quarter.

Save that checklist. Then every quarter, after earnings, run this:

PROMPT 3B: Quarterly Thesis Check

Here is my thesis checklist for [COMPANY]: [Paste the checklist from Prompt 3A]

Here are the Q[X] 2026 earnings results: [Paste the press release and any relevant transcript sections]

For each assumption on my checklist, tell me:

— CONFIRMED: evidence from this quarter that supports the assumption

— CONTRADICTED: evidence from this quarter that challenges the assumption —

NO SIGNAL: the quarter gave no clear information either way

At the end, give me a one-line verdict:

THESIS INTACT / THESIS WEAKENED — WATCH / THESIS BROKEN — REQUIRES DECISION.

Do not tell me what to do with the position. Tell me what the evidence says.

What this looks like in practice

My thesis on Kinsale Capital rests on three things: their ability to underwrite non-standard E&S risks at a combined ratio well below the industry, their cost advantage relative to larger competitors, and premium growth that reflects both market share gains and pricing power. When Q1 2026 showed commercial property premiums falling 28% on heightened competition, Claude flagged it immediately as a contradiction of the market share assumption, while also noting the combined ratio had improved to 77.4% and reserve development remained favorable, both confirmations of the underwriting discipline assumption. The verdict: THESIS WEAKENED — WATCH. That’s exactly right. Not broken. But worth monitoring closely.

Where this goes wrong

The thesis checklist is only as good as the thesis you give Claude to start with. If your original investment notes are vague, like “Kinsale is a great compounder with a good management team”, the checklist will be vague too. Garbage in, garbage out. The discipline of writing a specific, falsifiable thesis for each holding is the work. Claude just helps you track it.

Workflow 4: First-pass screening on a new idea in 30 minutes

Saves approximately 1–2 hours per new idea

Every serious investor has the same problem with new ideas: there are more interesting businesses than there is time to investigate them properly. The first-pass filter, is this worth two weeks of serious research? Is itself time-consuming.

Claude helps with the workload.

PROMPT 4: Cold-Start Business Assessment

I am a long-term quality growth investor. I look for businesses with durable competitive advantages, high and consistent returns on invested capital (above 15%), the ability to reinvest a large proportion of earnings at high rates of return, and management teams with a track record of excellent capital allocation.

I have just come across [COMPANY] and know very little about it. I am going to paste the two most recent quarterly reports, and the most recent annual report, and other relevant information I have. I want you to help me decide whether this deserves serious further research.

Please give me:

1. BUSINESS MODEL: How does this company make money? Who are its customers and why do they pay?

2. INITIAL QUALITY FILTER: Based on the financials provided, what do the ROIC, gross margins, operating margins, and FCF conversion look like? Are these consistent over time or volatile?

3. POTENTIAL MOAT: Based on the business description, what are the possible sources of competitive advantage? Be honest, if the moat is unclear or weak, say so.

4. REINVESTMENT RUNWAY: Is there an obvious long runway for reinvesting earnings at high rates of return? What would drive that reinvestment?

5. INITIAL RED FLAGS: What are the two or three things about this business that a quality growth investor should be most concerned about?

6. VERDICT: On a simple scale — PASS (not worth further research), INTERESTING (worth a deeper look), COMPELLING (this has the hallmarks of a quality compounder) where does this sit? Explain your reasoning in two sentences.

Be direct. I would rather you tell me a business doesn’t qualify than dress it up.

Where this goes wrong, and this is important

This is the workflow where AI is most dangerous. Claude will give a confident assessment of a business’s competitive advantages based entirely on the information you give it and its training data. It has no ability to assess whether a moat is real in practice, whether customers actually stay, whether pricing power holds under pressure, whether the culture that drove the returns is still intact. A confident “COMPELLING” verdict from Claude on a new idea means almost nothing without your own independent judgment. Use this as a filter, not a conclusion. The serious work still starts after this prompt.

Workflow 5: Cutting through macro and sector noise

Saves approximately 1 hour per week

The financial internet produces infinite content. Most of it is on the interest rate takes, the tariff commentary, the recession probability estimates. This will often never matter for the long-term value of the businesses you own. The trap is reading all of it anyway.

When something from the macro might matter for a specific holding, use Claude to assess the actual business-level impact quickly, rather than reading twelve articles that all say the same thing.

PROMPT 5: Business-Level Macro Impact Assessment

I own [COMPANY] as a long-term holding. Here is a brief description of their business model and the key drivers of their economics: [2–3 sentences on the business]

[MACRO EVENT] is being widely discussed as a potential risk or opportunity for businesses like this. Please help me think through the actual business-level impact.

1. DIRECT EXPOSURE: Does this company have direct revenue, cost, or operational exposure to [MACRO EVENT]? Be specific, what percentage of revenue, what cost lines, what geographies?

2. SECOND-ORDER EFFECTS: What are the less obvious ways this could affect the business, customer behavior, competitor positioning, input costs, regulatory response?

3. WHAT WOULD HAVE TO BE TRUE: For [MACRO EVENT] to materially impair this company’s earnings power over a five-year horizon, what would have to happen? How likely does that chain of events seem?

4. WHAT MANAGEMENT HAS SAID: If I paste recent earnings call commentary, identify exactly what management said about this topic and whether their response sounds prepared and thoughtful or vague and evasive.

Give me a one-paragraph conclusion on whether this macro event deserves to change my view of the long-term thesis.

What this looks like in practice

When tariff concerns were dominating financial media in early 2026, I ran this prompt for LVMH. Claude quickly surfaced that Fashion & Leather Goods had direct exposure to transatlantic goods flows, that China recovery remained the bigger driver of the thesis, and that management’s Q1 commentary had been notably vague on the North America impact. That was a useful 10-minute framing that let me stop reading tariff articles and focus on the actual questions that mattered for the position.

What the reclaimed time is actually for

Saving 10 hours a week sounds like the goal, but its not.

The goal is to spend those 10 hours on the work that actually drives investment returns over decades. The reading that builds pattern recognition, the thinking that develops conviction, the uncomfortable questions about what you might be wrong about in your highest-conviction positions.

The investors who compound wealth seriously over a long period aren’t faster at grunt work. They spend more time thinking clearly about fewer, better questions. AI just gets you there faster.

What you should never use AI for

This section matters as much as everything above it.

Never use AI to decide whether to buy or sell. Claude will give you a structured answer to any question you ask, including “should I add to this position?” That answer is worthless. It has no skin in the game, no understanding of your portfolio construction, no memory of what you paid, and no ability to weigh qualitative factors that only come from years of following a business. The buy and sell decisions are yours. Permanently.

Never trust a number Claude gives you without checking the source. Claude fabricates figures with complete confidence. It will cite a ROIC of 23% for a company whose actual ROIC is 14%. It will pull a revenue figure from the wrong quarter. It will confuse operating income with net income. Every single number that matters (every number you might act on) needs to be verified against the primary source.

Never use AI as a substitute for reading the filings yourself. Claude’s summaries flatten nuance. An earnings call transcript has texture, the pause before an answer, the question that gets deflected, the topic that the CEO rushes past. You only catch that if you’ve read enough transcripts to know what normal sounds like. Claude has never read a transcript with skin in the game. You have. Use Claude to find the sections worth reading carefully. Then read them carefully.

Never use AI on questions where the answer requires judgment about the future. “Will Novo Nordisk maintain its competitive position in GLP-1s?” is not a question Claude can answer. It will give you a confident framework and a balanced conclusion. That conclusion is constructed from patterns in its training data, not from any genuine understanding of pharmaceutical competitive dynamics, patent cliffs, or the likelihood that oral Wegovy changes the category. On questions of qualitative judgment about the future, Claude is confidently mediocre. Your own reading, thinking, and pattern recognition (Even if its not perfect) is more valuable.

Never let AI make you feel like you’ve done the work when you haven’t. This is the most subtle and dangerous failure mode. Running five prompts and getting five structured outputs feels like research, but its not. It’s “organized preparation”. The research is what happens when you sit with the questions those outputs raise and think hard about what you actually believe.

Final Thoughts

Investing well is a craft. It rewards patience, judgment, and the ability to think clearly about businesses over long periods of time. None of that can be automated. None of it should be.

But the hours you spend reformatting tables, skimming risk factors, and manually comparing numbers across eight quarters? Those hours were never doing the work. They were just the cost of accessing the work.

AI eliminates that cost. What you do with the time it gives back is still entirely up to you.

The prompts above are a starting point, not a system. Your system will develop as you use them, refine them, and figure out where they work for your process and where they don’t. Start with the earnings processing prompt this quarter. Build from there.

Ten hours is a lot of thinking time to give back to yourself every week. Use it well.

The prompts from this article, ready to copy:

Prompt 1: Earnings Processing

Prompt 2: Annual Report Deep Dive

Prompt 3A: Extract My Core Thesis Assumptions

Prompt 3B: Quarterly Thesis Check

Prompt 4: Cold-Start Business Assessment

Prompt 5: Business-Level Macro Impact Assessment

(Save these to a text file and customise them to your own portfolio and investing philosophy before your first use.)

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com