How I Built a Personal AI Analyst in 30 Minutes (And How You Can Too)

A step-by-step guide to turning Claude into your own quality investing research machine with prompts for every stage of your analysis.

Hi there, investor 👋

Here’s something I used to do every time I started researching a new stock.

I’d open the annual report. Read 40 pages of reporting jargon. Open a competitor’s filing. Try to hold both in my head simultaneously. Build a rough DCF in a spreadsheet. Go back and re-read the sections I’d already forgotten.

It worked. But it took forever. And the result was only great if I spent significant time and effort to make it happen.

Now I do most of that groundwork in Claude. Not because AI replaces my thinking (it definitely doesn’t), but because it dramatically accelerates the legwork so I can spend more time on what actually matters: forming a strategic long-term view of the business and if it fits into my portfolio.

This guide shows you exactly how I set it up. You can steal every prompt if you want to. I’ll use Constellation Software (CSU) as the running example throughout, since it’s a stock many of you know well and it’s a great test case for quality compounder analysis.

The setup in Steps 1–2 takes about 10 minutes once. After that, each new stock research session takes 5 minutes to get to a point that used to take 3-5+ hours.

Why Most Investors Use AI Wrong

If you’ve opened Claude or ChatGPT and typed “Tell me about Constellation Software,” you’ve experienced the problem.

You get a fluent, confident, surface-level summary. It reads well. It tells you nothing you couldn’t find on the Wikipedia page. It’s almost useless for serious investing.

Claude out of the box is a general-purpose assistant. It doesn’t know you’re a quality-focused investor who cares about ROIC, capital allocation, and durable competitive moats. It doesn’t know what you already know, what your investment horizon is, or what you’re trying to decide.

The difference between a generic AI response and a genuinely useful research session is context and structure. That’s what this guide is about.

The 5-Step Setup

Step 1: Choose the Right Tool and Plan

I use Claude’s pro plan to get access to the most powerful AI model. This guide will revolve around Claude. I’ve used multiple AI Models, but nothing comes close to Claude in my opinion.

Here’s why this matters for investors:

Claude handles very long documents better than most alternatives. You can paste or upload an entire 100+ page annual report and have a coherent conversation about it.

The Pro plan gives you access to Claude’s most capable models with a significantly larger context window. This is critical when you’re working with 10-Ks, earnings transcripts and competitor filings simultaneously.

Claude tends to be more careful about expressing uncertainty than alternatives, which matters when you’re making real financial decisions.

Important caveat

Claude’s knowledge has a training cutoff. It will not know last quarter’s earnings. Always provide recent documents yourself rather than relying on Claude’s own knowledge of current financials.

Step 2: Write Your Investor Identity Prompt

This is the most important step in the entire guide. If done right, it transforms Claude from a generic assistant into something that thinks like your analyst and provides tremendous value.

At the start of every research session, paste this prompt (customised to you) before you do anything else. It primes Claude with your investing philosophy, your framework, and the level of analysis you expect.

PROMPT 1: Your Investor Identity (customise and save this)

You are my personal investment research analyst. Here is my investing philosophy and framework. Please apply this throughout our entire conversation.

INVESTING PHILOSOPHY:

I am a long-term, quality-growth-focused investor with a 5-10 year holding horizon

I focus on businesses with durable competitive advantages (moats) and high returns on invested capital (ROIC consistently above 15%)

I look for companies that can reinvest a large proportion of earnings at high rates of return (compounders)

Capital allocation quality is a primary filter. I want management teams that think like owners

I am willing to pay a fair price for an exceptional business, but I am valuation-conscious

WHAT I CARE MOST ABOUT:

Quality and durability of the competitive moat

ROIC trends and reinvestment runway

Management incentives and capital allocation track record

Unit economics and margin structure

Key risks that could impair the thesis

WHAT I DO NOT WANT:

Surface-level summaries I could find on Wikipedia

Overly bullish framing, I want balanced, honest analysis

Vague qualitative statements without backing evidence

Financial projections stated as facts

Please ask clarifying questions if you need more context. When I give you a document or company to analyse, apply this framework throughout.

Save this as a text file and paste it at the start of every new conversation. It takes 10 seconds and it changes everything.

Step 3: The Annual Report Deep-Dive

Now the real work begins. Upload or paste the company’s most recent annual report (or 10-K for US companies). For CSU, this is their annual letter to shareholders plus the full financial statements.

Don’t ask Claude to “summarise” it. That’s the generic approach that gives you generic results that are low value. Instead, use a structured prompt that mirrors how a good analyst actually reads a filing.

PROMPT 2: Annual Report Deep-Dive

I have uploaded Constellation Software’s [YEAR/QUARTER X] report. Please analyze it using my investing framework and answer the following:

1. MOAT ASSESSMENT

What are the primary sources of competitive advantage?

What evidence in this report supports or challenges the moat thesis?

Has the moat strengthened or weakened compared to prior years? If any change, what is the reason?

2. CAPITAL ALLOCATION

How did management deploy capital this year (acquisitions, buybacks, reinvestment)?

What is the ROIC on recent acquisitions, and how does this compare to historical returns?

Are there any signs of capital allocation discipline deteriorating?

3. FINANCIAL QUALITY

Summarise the key metrics: revenue growth, Gross/Operating/FCF margins, free cash flow conversion, ROIC

Are there any accounting choices that warrant scrutiny (revenue recognition, capitalised costs, goodwill treatment)?

How does FCF compare to reported earnings?

4. MANAGEMENT COMMENTARY

What did management say about the business that was notably honest, straight-forward, or forward-looking?

Were there any significant omissions or areas where they were evasive?

5. KEY RISKS MENTIONED (OR NOT MENTIONED)

What risks did management acknowledge?

What risks do you think are underemphasised or absent from their discussion?

Please be specific and cite the relevant sections of the report where possible.

This prompt alone will get you 80% of the way through a first-pass analysis. The output won’t be perfect, but it will be structured, consistent to the framework you want, and far faster than reading the full document yourself from scratch.

Step 4: The Red Flag Check (Steelman the Bear Case)

This is a crucial step, and will often be extremely valuable.

After you’ve built a positive view of a company, confirmation bias kicks in hard. You start reading everything through a bullish lens (I’ve fallen into this trap many times). Claude can help you fight this by being instructed to argue against you.

PROMPT 3: Steelman the Bear Case

Now I want you to switch roles. Forget the positive framing. Your job is to build the strongest possible bear case for Constellation Software.

Specifically:

What are the 3-5 most credible risks that could permanently impair the thesis?

Is there any evidence in the annual report that the moat is narrowing or that reinvestment returns are declining?

What would have to be true for CSU to be a value trap rather than a compounder?

Are there any red flags in the financial statements that a bull might rationalise away?

If you were a short seller, where would you focus your research?

Be direct and don’t soften the analysis. I want to understand what could go wrong.

The quality of Claude’s bear case will depend heavily on the quality of the document you gave it. If you also upload a short-seller report or a critical analyst note, add that to the conversation before running this prompt.

Step 5: Build Your Valuation Scenarios

I don’t use Claude to build my actual discounted cash flow. I do that in a spreadsheet where I control the inputs. But I use Claude to stress-test my assumptions before I build it, this catches lazy thinking before it manifests into a valuation model.

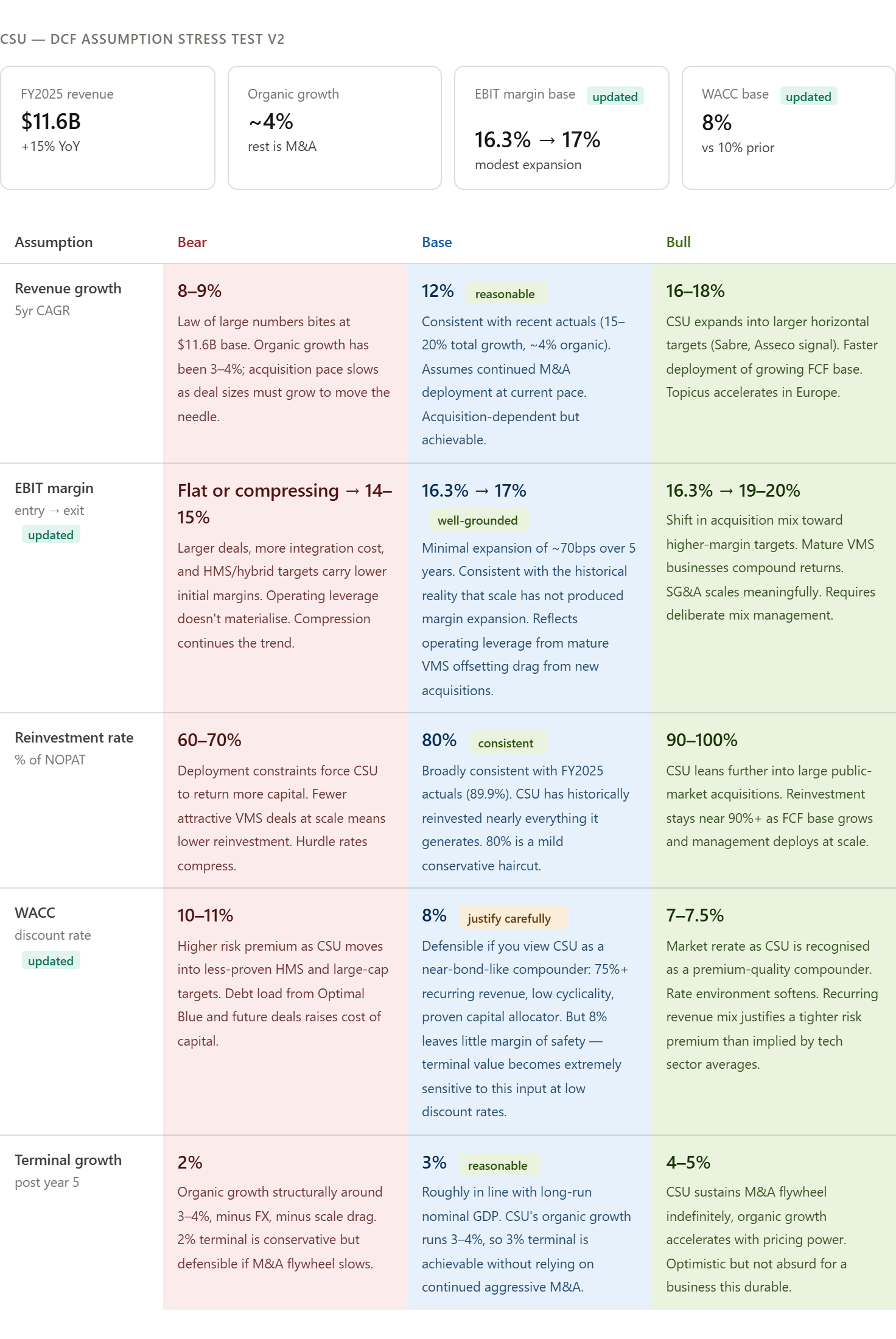

PROMPT 4: DCF Assumption Stress Test

Based on your analysis of Constellation Software, help me stress-test my valuation assumptions.

My base case assumptions:

Revenue growth: 12% per year for 5 years, then 3% terminal

EBIT margins: expanding from 16.3% to 17% over 5 years

Reinvestment rate: 80% of NOPAT

WACC: 8%

Please:

Challenge each assumption. Are they consistent with the company’s historical trajectory?

Define a realistic bull case and bear case for each key input

Identify which single assumption has the biggest impact on intrinsic value

Flag any assumptions that seem inconsistent with each other

Present this as a structured table with three columns: Bear / Base / Bull, with brief rationale for each.

Fill in your own numbers before running this. The output gives you a structured framework you can take directly into your spreadsheet model.

The result from my Constellation Software examples 👇

Claude acts as my sparring partner for my assumptions, giving me pointers to consider for each of the assumption I have given it.

This is how I would proceed:

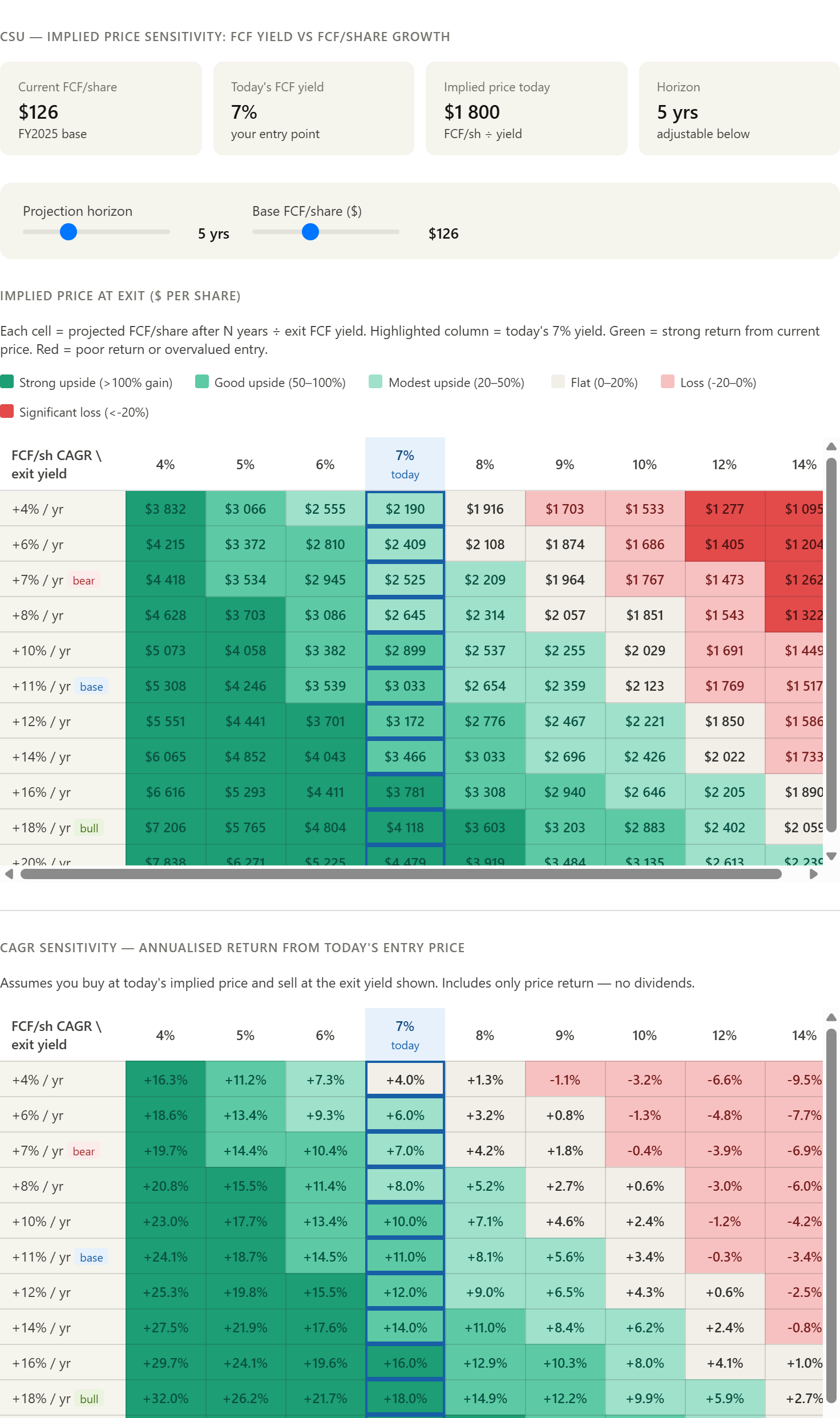

What would be the FCF per share growth for CSU in each of the scenarios?

Claude then does the calculations based on my inputs, and creates visuals and graphs to make it more professional looking.

I would follow this up with a sensitivity analysis to better understand how movements in FCF per share growth and FCF yield will affect the return.

Note: Always give Claude current numbers like today’s stock price, or for this case, today’s FCF yield.

My prompt (Claude now has all the context, and you can ask it to do what you want and get accurate results):

Create a sensitivity analysis with different valuation and growth points (FCF per share growth and FCF yield). Today’s FCF yield is 7%.

How awesome is that?

I now have a well put sensitivity analysis on Constellation Software that is basically ready for presentations or a report.

If you want it in excel or Power Point format, you can just ask Claude to create the document for you with the proper formatting.

This used to take an analyst hours to do. Claude can now do this for you in a few minutes, with the right prompts and correct reporting documents.

After you’ve done this one time, this process will take you less than 5 minutes, and you can refine the prompts over time to fit your style or needs.

The Prompt Playbook: Save These

Here are three additional prompts I use regularly that didn’t fit into the five steps above. These are worth saving to a text file alongside your identity prompt.

Competitive Comparison

PROMPT 5: Head-to-Head Competitor Analysis

Compare Constellation Software and [COMPETITOR] across the following dimensions:

Business model and moat source

ROIC and capital allocation approach

Revenue quality (recurring vs. transactional, switching costs)

Management quality and incentive structure

Valuation: what growth and returns are currently priced in for each?

Where the two companies differ most significantly, explain why that difference matters for long-term compounding.

Earnings Call Analysis

PROMPT 6: Earnings Call Deep-Read

I am uploading the transcript from Constellation Software’s most recent earnings call. Please:

List the 3 most important things management said (that weren’t already in the annual report)

Identify any language changes from prior quarters — are they more cautious, more confident, or evasive on any topic?

What questions from analysts were most revealing, and how did management respond?

Were there any non-answers or deflections that warrant follow-up research?

Does anything in this call change the thesis materially? If so, how?

Initial Screening

PROMPT 7: 5-min analysis (before deep research)

I am considering researching [COMPANY NAME] more deeply. Before I invest significant time, please give me a rapid quality screen:

What business does this company operate, and what is the proposed source of competitive advantage?

Is there publicly available evidence that ROIC is consistently above the cost of capital?

What are the two or three biggest reasons this might NOT be a quality compounder?

Is this a business I would need to monitor quarterly (high execution risk) or one where the moat is structural and durable?

Based on this screen, give me your honest assessment: is this worth a deep dive, or are there structural issues that make it unlikely to meet a quality compounder framework?

What Claude Can’t Do (Very important)

This section matters as much as the prompts.

Claude can hallucinate specific numbers. Always verify financial figures against the source document. Never use a number Claude states without checking the original filing.

Claude doesn’t know what happened last quarter. Its training has a cutoff date. For anything recent, you must provide the documents yourself (I prefer to always provide documentation).

Claude can’t tell you what a stock is worth. It can help you stress-test assumptions, but the judgment call on valuation is yours.

Claude is susceptible to the quality of what you give it. A well-written, honest annual report produces better analysis than a PR-heavy one. Garbage in, garbage out.

Claude doesn’t replace pattern recognition built over years of reading businesses. It accelerates research. The decision maker and analyst is still you.

Claude and AI is a tool that can enhance a great thinker into an exceptional one. By taking the grunt work for you, it frees up time to focus on the truly important questions.

The right mental model

Think of Claude as a very well-read intern who has read everything but experienced nothing. They can synthesise documents faster than any human, structure frameworks clearly, and challenge your thinking. But they have no skin in the game, no track record, and no judgment built from watching businesses succeed and fail over decades. That judgment is yours.

Where to Start Today

Don’t try to implement all five steps at once. Here’s the minimum viable version:

Copy Prompt 1 and customise it to your own investing philosophy. Save it as a text file.

Pick a stock you already know well and upload its latest annual report.

Run Prompt 2 and Prompt 3 back to back. See whether the analysis surprises you, and whether it catches anything you missed.

That’s it. The whole thing takes 25 minutes for a stock you’re already familiar with. Once you’ve done it once, the workflow becomes second nature.

If you build something useful on top of this, a prompt I haven’t included, a workflow that works better for a specific type of business, leave it in the comments below or reply to this email.

Marius

Whenever you are ready, this is how I can help you:

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Essentials of Quality Growth — Join more than 300 investors who have bought the guide. Essentials of Quality Growth Investing is a multi-step guide for building a stock market portfolio of 10-20 high-performing quality compounders.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

(Free) How to analyze the financial statements — Learn how you read & analyze the balance sheet, income statement, and cash flow statement.

Promote yourself to +15.000 stock market investors (42% open rate) — Contact us via: investinassets20@gmail.com

Using Claude as a pre-research accelerator is an underrated move. The prompts for DCF context and competitor mapping save hours of filing work. Thoughtful guide.

The edge is no longer access to information.

It is structuring workflows that turn overwhelming data into repeatable decision frameworks faster than consensus adapts.