Bouvet: Bridging the Gap Between Business and Technology 💡

Fairly valued market leader with superb fundamentals 🧠

Hi partner! 👋

In case you missed our latest articles:

We are building a video course on quality growth investing 👨🏫

If you want to become a better investor, you might want to check out the Quality Growth System, it teaches you a complete system for finding, storing, ranking, and selecting the stocks with the highest quality and the lowest valuation to help you find quality compounders.

Sign up for an early release offer when the course releases:

Bouvet AS

Table of content

Business Model

Clients & Customer satisfaction

Revenue Streams

Capital light business model

The Stock

Stock-based compensation

Return on Invested Capital

Growing demand for the product or service

Market share

Growth drivers

Fundamentals

Management Team

Competitive Edge

Risk Factors

Valuation

Conclusion

Business Model

Bouvet is a consultancy firm that delivers a wide range of information technology and digital communication services to businesses in Scandinavia.

Bouvet offers a wide array of consultancy services to its clients:

Consulting services — IT & Management consulting

Development services — Software development, System integration, Cloud Solutions, Infrastructure

Project Management

Design & UX

Data analytics & Business intelligence

Bouvet differentiates itself from other consultancy companies through its superior corporate culture where the best technologists thrive. Bouvet is able to attract and retain top talent by providing a great work environment, profit-sharing programs, and training programs to develop their talent.

Employees are loyal to Bouvet — This is important as their employees are its most valuable assets.

Their top talent and expertise combined with a long-standing relationship with Norway’s largest corporations give them a unique edge that is not easy to replicate.

There are countless technology-related consultancy firms. But Bouvet stands out as a clear market leader in the Norwegian market.

Clients & Customer satisfaction

Bouvet holds multiple long-term relationships and rolling contracts with large businesses in Norway. To name a few: Innovasjon Norge, Lyse, Eress, and Norwegian Water Resources and Energy Directorate (NVE).

Their client base is a healthy mix of the public sector (43%) and private sector (57%).

Both are in need of digitalization, but the public sector companies are in deep need of digitalization. Government & Oil/Gas companies have made significant investments in the last 5 years, boosting Bouvet sales.

Bouvet’s customer satisfaction score from its clients:

Revenue Streams

Bouvet is a well-diversified consultancy firm with many financially strong clients, like Statnett, The Norwegian Forces, and Equinor.

Oil & Gas represents 40.7% of their business (Growing 21.3% YoY)

Power Supply represents 18.7% of the business (Growing 40% YoY)

Public admin represents 17.6% of the business (Growing 11.7% YoY)

Service industry represents 5.2% of the business (Growing 1.6% YoY)

The Oil & Gas segment is the largest segment for Bouvet. This is a double-edged sword. In good times, companies like AkerBP, Equinor, and Var Energi will invest heavily in new projects where Bouvet’s expertise is needed. But in bad times (when the price of oil tanks like in 2015), there is a full stop in consultancy spending.

Bouvet is likely to be affected by an economic downturn, but its diversified clientele will work as a limiting factor to a substantial downside.

Capital light business model

Bouvet spent NOK28.9 million on Capital Expenditures in 2023, up from NOK26.7 million in 2022.

If we compare this to the cash from operations of NOK506.1 million and NOK321.9 million, we get the following:

Capex/OCF 2023: 5.7%

Capex/OCF 2022: 8.3%

This is well below our target of sub 20%.

Bouvet’s revenue in 2023 was NOK3.525 billion, and 3.085 billion in 2022. Comparing:

Capex/Revenue: 0.82%

Capex/Revenue: 0.86%

Bouvet runs a capital-light business model.

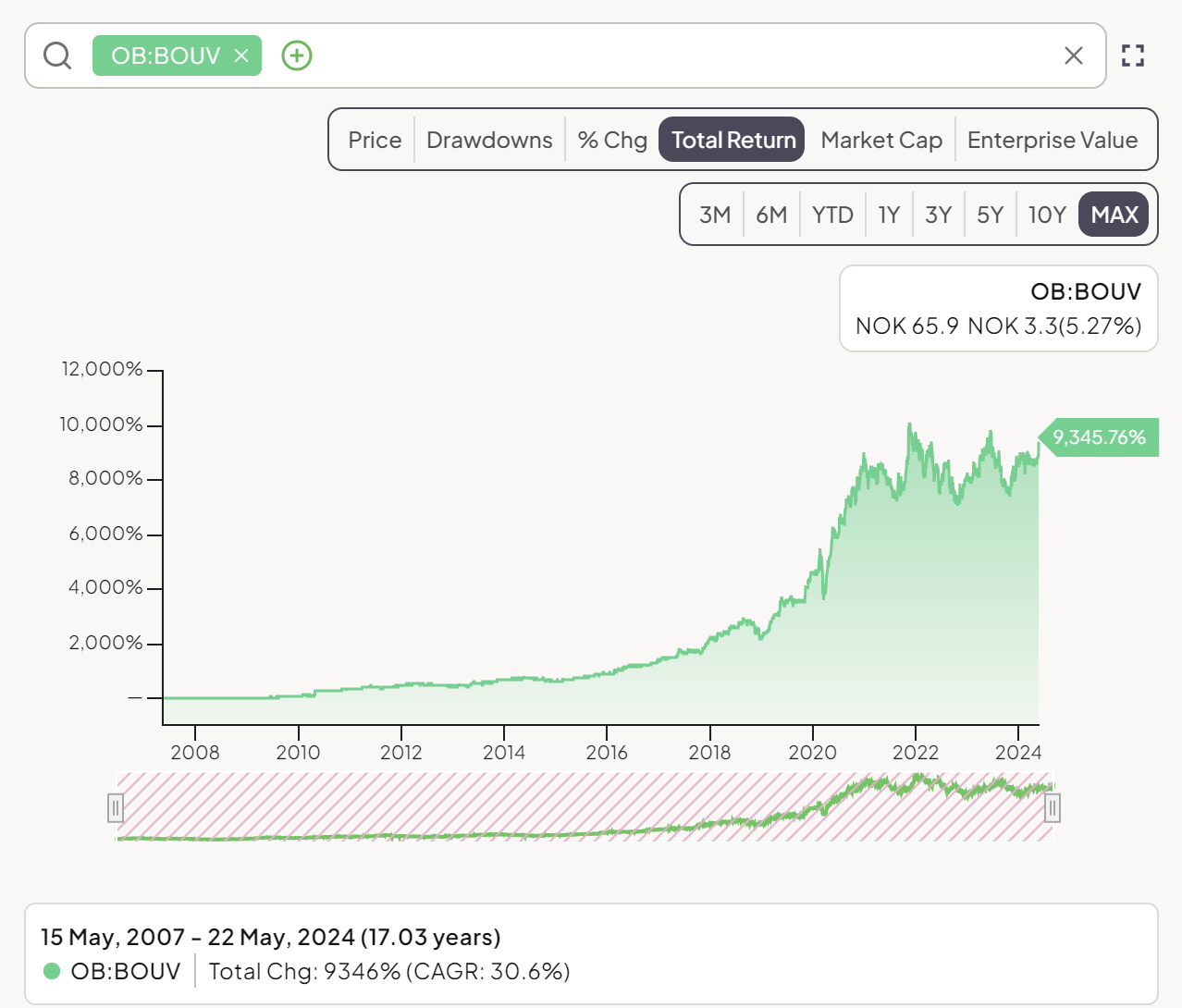

The Stock of Bouvet

Bouvet is a quality IT consultancy business that has seen impressive compounded annual growth rates since inception. The CAGR is 30.6% since 2007:

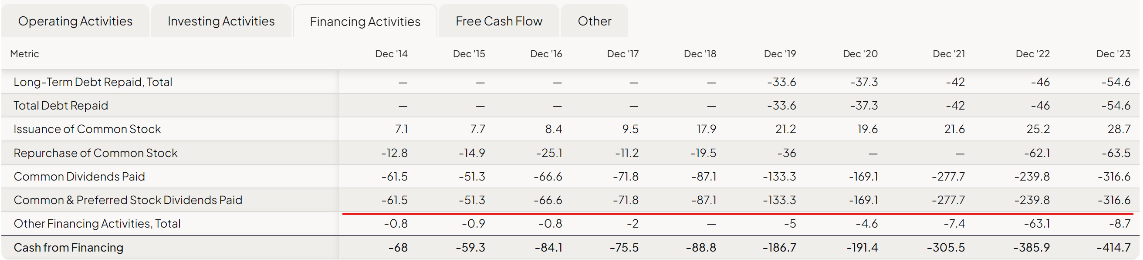

Stock-based compensation

Bouvet uses incentive programs to attract and retain top talent. In 2023, they spent 28.7 million on their employees, and in 2022, 25.2 million.

Stock-based compensation as a percent of operating cash flow:

SBC / OCF 2023: 5.67%

SBC / OCF 2022: 7.8%

This is within reason. We prefer this number to be below 10%.

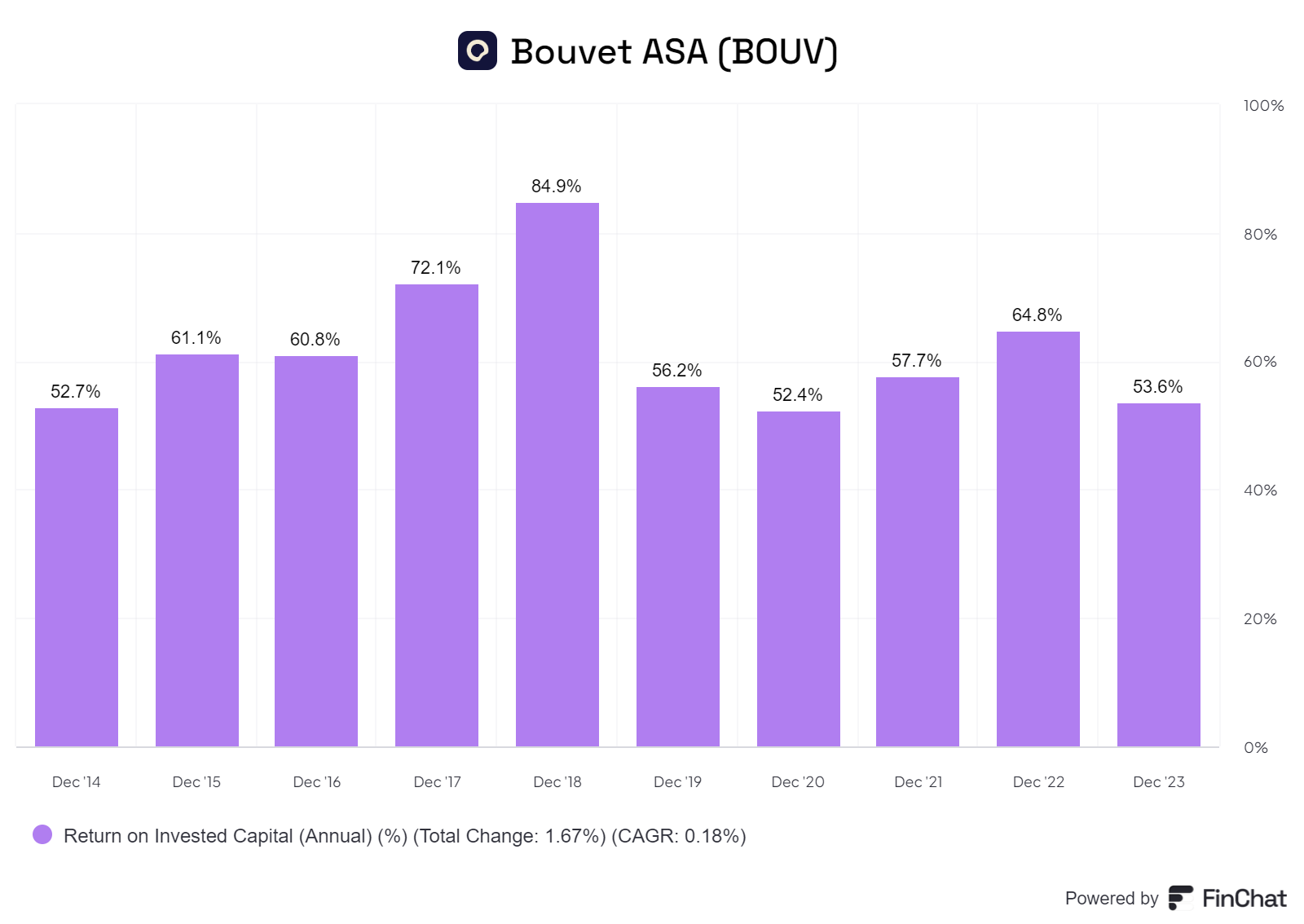

Return on Invested Capital

Bouvet boasts industry-leading returns on invested capital with persistent +50%

Return on invested capital:

Bouvet is unable to reinvest all of its earnings into the business like a true compounder. Most excess capital is allocated to stock buybacks and dividend payments.

They do however make the occasional small acquisitions of smaller specialized consultancy firms.

Growing demand for the product or service

The overhanging secular trend that is beneficial for Bouvet is digitalization.

More businesses want to become digital to save time, effort, and resources. The main emerging fields that are of interest:

Cloud computing

Artificial Intelligence

Automation

Internet of Things (IoT)

Large entities like Lyse, Lyse Tele, Equinor, and AkperBP have been investing heavily in Cloud Computing to get more of their non-core internal services in the Cloud. Bouvet is the preferred partner to support this transition.

AI & Automation is what is on everyone’s mind. Companies want to learn how they can leverage AI and automation to reduce their overhead while making better and more accurate decisions in their operations.

Market share

The Norwegian consultancy market consists of multiple consultancy firms, including Capgemini, Sopra Steria, Accenture, Tieto Evry, and Webstep. We are not able to get a grasp of the international company’s market share, but we can view the regional players.

Bouvet is growing at a healthy rate, with 14.3% revenue growth in 2023 YoY. The total NOK amount is close to NOK500 million.

Webstep is also growing at a healthy clip, although historical growth is much lower, and its revenue base is much lower, increasing its revenue by NOK115 million in 2023.

TietoEvry is a stalwart with very low organic growth. The huge jump in 2020 was a merger between Tieto and Evry.

This indicates to us that Bouvet is able to take market share. It is clearly adding the most NOK and is growing faster than the competition despite its size.

Keep in mind that we are not able to view Accenture, Capgemini, and Sopra Steria’s numbers for market share. But we can assume that their presence is lower. Accenture does not even have an office in the Stavanger region (Where the large oil & gas businesses reside).

The rest of the article is for Premium subscribers, consider joining us. Read more here.