What actually makes a business compound at 20%+ per year 🏰

The structural traits that separate true compounders from everything else

Hi there, investor 👋

Today, we’re breaking down the 5 traits that separate 20% compounders from ‘good’ companies.

Most investors know the basics by now.

High ROIC & ROIIC

Long reinvestment runway

Capital-light model

These are the entry requirements, the minimum spec for a quality growth business.

But they do not explain why some compounders deliver 12% annually and others deliver 20%.

The gap between good and exceptional is not ROIC. It is five things that are harder to see in a spreadsheet.

Let’s get into it 👇

Build a Market-Beating Portfolio of Quality Compounders, Now 30% Off

Many world-class compounders are currently trading at multi-year low levels. We do the work to identify the few that truly matter, businesses with durable moats, high returns on capital, and long reinvestment runways.

Inside the Premium service, you get:

💎 A focused portfolio of high-quality businesses

📈Clear buy & sell alerts

📚 Deep dives that actually explain why something works

📜 A repeatable framework you can use for life

Get 30% off before the price hike, and start building a portfolio designed to outperform over the next decade.

Don’t overcomplicate it. Own better businesses. Let time do the work.

1. Pricing power that nobody talks about: the annual price letter

The companies that compound at 20% do not just have pricing power. They exercise it systematically, every single year, without losing customers.

Most businesses raise prices occasionally. The great compounders raise prices as a matter of policy. FICO charges mortgage lenders a fee every time they pull a credit score. That fee has gone from a few dollars to over $10 in recent years, with essentially no pushback, because there is no alternative. The product is mandated by the lending process. Customers do not like the increases. They pay them anyway:

Brunello Cucinelli does the same thing at the other end of the market. The company raises prices 8 to 10% every year on cashmere goods that sell to ultra-high-net-worth buyers.

The price increases do not suppress demand. In some cases they stimulate it, because the customer base associates higher prices with greater exclusivity. The brand is the moat. The annual price increase is how the moat earns.

What to look for: a business where customers complain about price increases in earnings calls, analyst reports, or customer reviews, and then renew anyway. That is the signal. Annoyance without churn is pricing power (Even better if you don’t hear anything, like for Brunello customers).

2. The niche monopoly in a market nobody else wants

The most durable compounders do not dominate large, glamorous markets. They dominate small, boring ones that nobody else bothered to enter.

Judges Scientific is a collection of 30 scientific instrument companies making products like vacuum gauges, cryogenic equipment, and electron microscopes. Each subsidiary is the market leader in its niche.

The niches are so small that a competitor entering one would face years of development cost to capture a market worth a few million pounds. The economics of competition do not work. So nobody competes. This has allowed Judges to compound its free cash flow per share by +15% annually over the last decade:

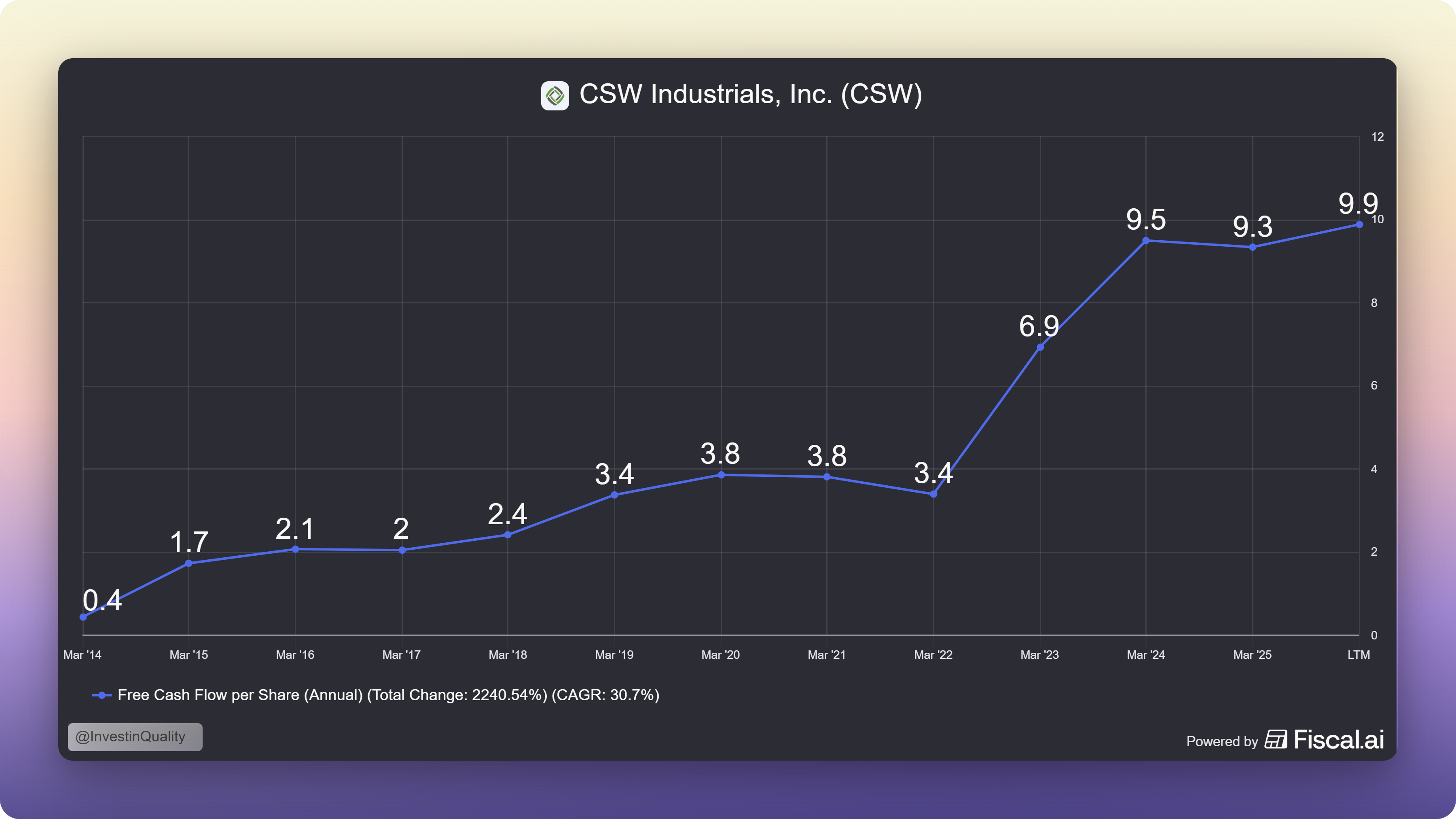

CSW Industrials makes products like HVAC dampers, plumbing solutions, and industrial sealants. Not exciting. But in the specific segments it occupies, it has dominant market share, 45% gross margins, and a customer base that has been buying from it for decades.

Switching costs are not contractual. They are practical. Nobody on a job site wants to re-specify a component that has worked fine for twenty years.

The result? +30.7% annual growth in free cash flow per share since 2014:

The pattern is the same across the best compounders: dominant position in a market too small to attract serious competition, with switching costs that make the dominant position self-reinforcing.

Rightmove has 80% of UK property listings. A competing portal would need to convince buyers and sellers to switch simultaneously. Neither will until the other does first. The niche locks in.

What to look for: operating margins that seem too high for the industry, combined with revenue that is almost entirely from repeat customers. That combination only exists when competition is structurally absent.

3. The decentralised operator model as the actual moat

Some businesses have a moat because of what they sell. The best serial acquirers have a moat because of how they are organised.

Lifco has 275 subsidiaries across dental equipment, demolition tools, and document management.

The businesses have almost nothing in common except one thing: they are all run by the people who built them, with their own P&Ls, their own hiring decisions, and their own capital within defined limits.

Head office in Stockholm has fewer than 20 people. The subsidiaries do not feel like subsidiaries. They feel like owner-operated businesses, because they are.

This structure produces two advantages that do not show up in any single year’s numbers.

First, it retains entrepreneurial talent. Founders who sell to Lifco stay. They keep equity-like incentives and operational independence. The alternative is selling to a private equity firm and being managed to a budget. Lifco wins that decision most of the time.

Second, the model scales without diluting returns. Each new acquisition is independent. There is no integration cost, no cultural homogenisation, no bureaucratic drag. The 275th acquisition is as clean as the first.

Addtech, Diploma, and Kelly Partners Group run versions of the same model. REQ Capital’s research on Nordic serial acquirers found that decentralisation was one of the three primary drivers of their 19% 20-year CAGR, alongside capital allocation discipline and owner-operator culture.

What to look for: subsidiary managers who have been with the business for ten or more years after acquisition, low head office headcount relative to group revenue, and management commentary that describes acquired founders as partners rather than employees.

4. The capital allocator who gets better with age

In most industries, competitive advantage erodes over time. In programmatic acquisition, it compounds.

The best capital allocators, Mark Leonard at Constellation Software, Carl Bennet at Lifco, Brett Kelly at Kelly Partners, get measurably better at buying businesses as the years go on. They build proprietary deal flow. They develop pattern recognition for which businesses will integrate well and which will not. They build reputations in their target sectors as the preferred buyer, which means they see more deals at better prices than anyone else.

Constellation Software has acquired over 800 vertical market software businesses. The institutional knowledge from those 800 acquisitions, what to pay, what to fix, what to leave alone, is not replicable. A new entrant trying to compete in VMS acquisition starts with zero. Constellation starts with three decades of accumulated judgment. That gap widens every year.

The proof is in the pudding, just look at how Constellation stack up versus other serial acquirers. Usually, you see a correlation between how large the acquisition spend is, and the return the acquirer will get on their capital spent.

However, for Constellation, it has managed to keep a best in class ROIC + 1/2 organic growth rate despite its size.

This is what makes the ROIIC story so important for serial acquirers specifically. The question is not just what returns they earn on new capital today. It is whether the returns on new capital are stable or improving as the business matures. For the best operators, the answer is improving, or at least maintaining despite larger acquisition spending.

What to look for: acquisition multiples that have remained consistent over a decade despite a competitive deal market, suggesting proprietary sourcing rather than auction participation. Also: founders who reinvest proceeds into the acquirer’s stock after selling their business. That is the clearest possible signal of trust in the capital allocator.

5. The business that gets harder to kill every year

The final trait is the one that most distinguishes a 20% compounder from a 12% one over a full decade. The business becomes more defensible every year it operates.

This is different from a business that just survives. A company can have stable revenues for twenty years without becoming harder to displace. What the great compounders build is a system where every new customer, every new product, every new acquisition makes the existing base more valuable and the switching cost higher.

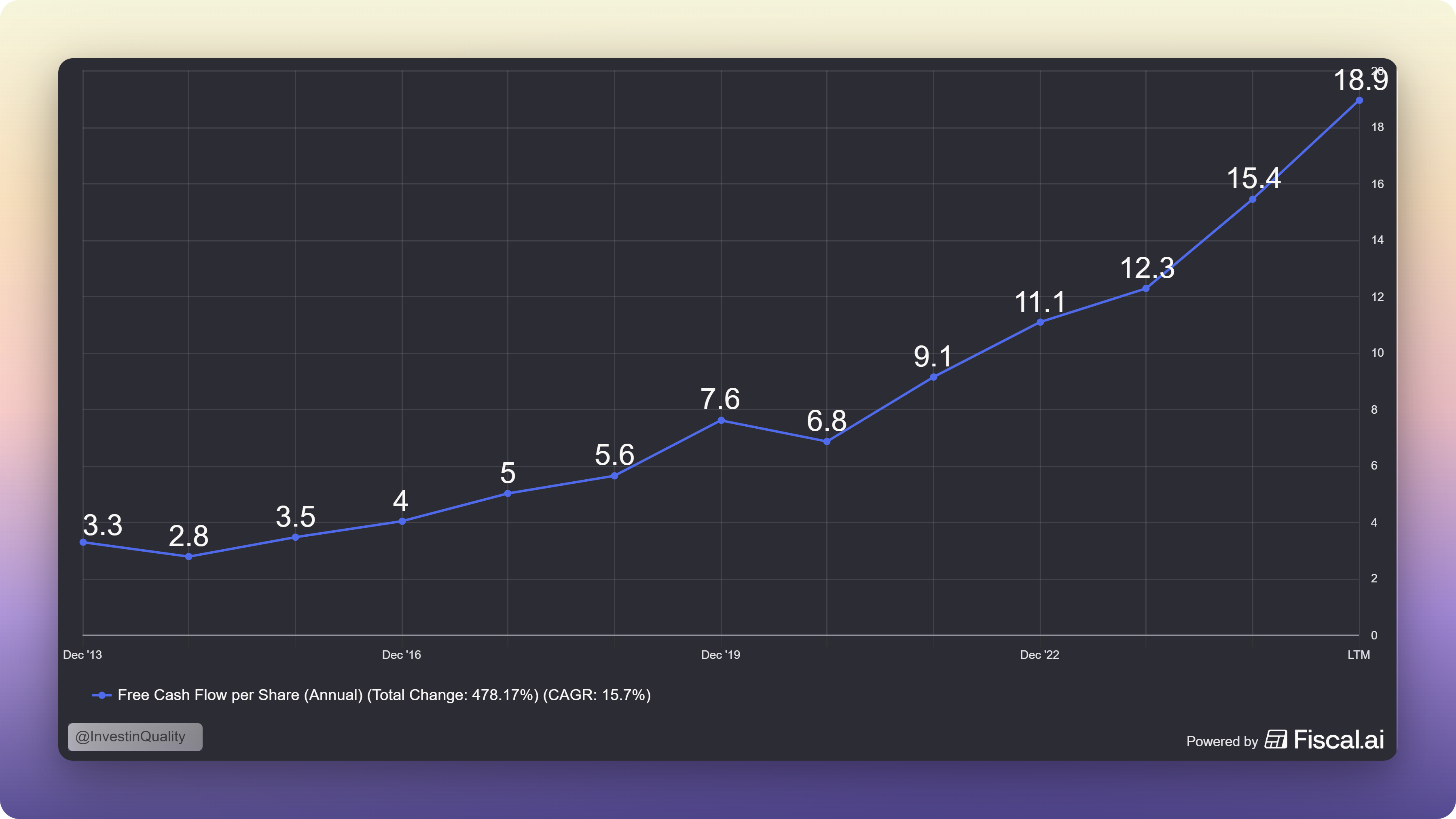

Mastercard is the clearest example at scale. Every merchant that accepts Mastercard increases the value of the network to every cardholder. Every cardholder that carries a Mastercard increases the value of acceptance to every merchant.

The network has been growing for sixty years and the flywheel has not slowed. Adding the 100 millionth merchant does not cost Mastercard anything. It makes the network worth more to everyone already on it.

Mastercard is one of the most consistant compounders with an annual free cash flow per share growth of 15.7% since 2013:

Topicus does this in European vertical market software. Each new VMS acquisition adds another sector to the platform. That makes Topicus a more credible acquirer for the next sector because it can demonstrate operational success in adjacent ones. The track record is the moat. The moat is built by the acquisitions. The acquisitions are made possible by the moat.

What to look for: net revenue retention above 100% in software businesses, meaning existing customers spend more each year without the company doing anything. In non-software businesses, look for revenue per customer that grows consistently year over year, not from upselling campaigns but from natural usage expansion.

Putting it together

The ROIC framework tells you whether a business is good. These five traits tell you whether it is exceptional.

Pricing power that is exercised annually without churn

A niche so small that competition is irrational

A decentralised model that scales without losing what made it work

A capital allocator whose judgment compounds alongside the business

And a flywheel that gets harder to stop every year it runs

When you find all five, the valuation question almost takes care of itself. A business with a 20% earnings CAGR and these structural characteristics will look expensive every year and cheap in hindsight every decade. That is the nature of compounding. The market prices the next twelve months. You are buying the next ten to twenty years.

That’s it for this time, let me know what you think in the comments below or by replying to this email!

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Disclaimer:

This newsletter is for informational purposes only and does not constitute financial, investment, or other professional advice. The views expressed are solely the author’s opinions and may change without notice.

Investing in securities involves risk, including the potential loss of capital. Past performance is not indicative of future results.

The author may hold positions in securities mentioned. Readers should do their own research and consult a licensed financial advisor before making investment decisions.

A lot of investors stop at high ROIC. The advantage is durability, reinvestment at scale. If returns hold as capital grows, you’ve found a real compounder.

I liked your "Putting it together" summary. Very well written and useful. Thanks for providing this information.