Uber's Rise From Ride-Hailing to a Global Tech Giant

Free cash flow yield of 6.3% and expected long-term earnings growth of +20%

Hi there investor 👋

Today we’re breaking down Uber Technologies 👇

The Rise of Uber Technologies

For much of the past decade, Uber was widely viewed as the most controversial company in Silicon Valley. The business burned tens of billions of dollars, fought regulators around the world, and struggled to convince investors that its model could ever produce sustainable profits. Critics often reduced the company to a simple question:

Is this really anything more than a taxi company with an app?

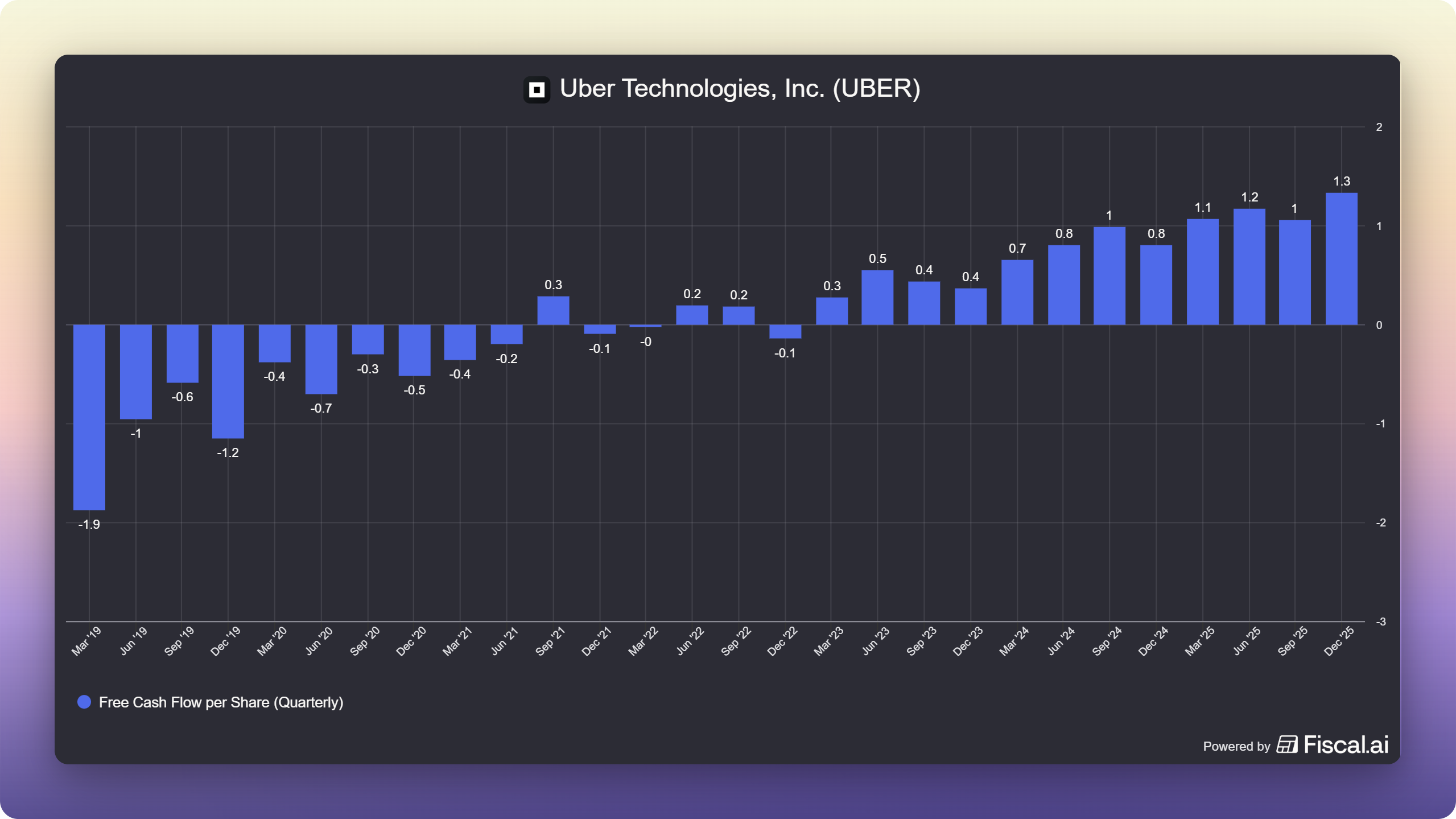

That narrative has slowly started to change. Over the past several years, Uber has transitioned from a high-growth, cash-burning startup into a large-scale global marketplace that generates significant free cash flow. In 2025 the company produced over $9.7 billion in free cash flow as the platform continued to scale and improve its efficiency.

Today, the investment debate around Uber is very different than it was just a few years ago. The key question is no longer whether the company can survive. Instead, investors are beginning to ask whether Uber could become a durable long-term compounder built on a global logistics marketplace.

Join the Premium Research

Free subscribers get occasional articles.

Premium Members get the full investing framework.

Including:

💎 Full Portfolio Access (80% of my net worth invested alongside members)

📢 Real-Time Buy & Sell Alerts

📊 Monthly Portfolio Factsheets

🏰 Quality Deep Dives

📘 Complete Research Archive

Everything is built around one goal:

Identifying businesses capable of compounding capital for decades.

Become a Premium Member👇

Note: The price will increase 50% on April 1st.

Understanding What Uber Is

To understand the investment case, it helps to step back and think about what Uber actually does. On the surface, the company offers ride-hailing and food delivery services, but those products are only the visible layer of the business. Fundamentally, Uber is a platform that coordinates supply and demand across large transportation networks.

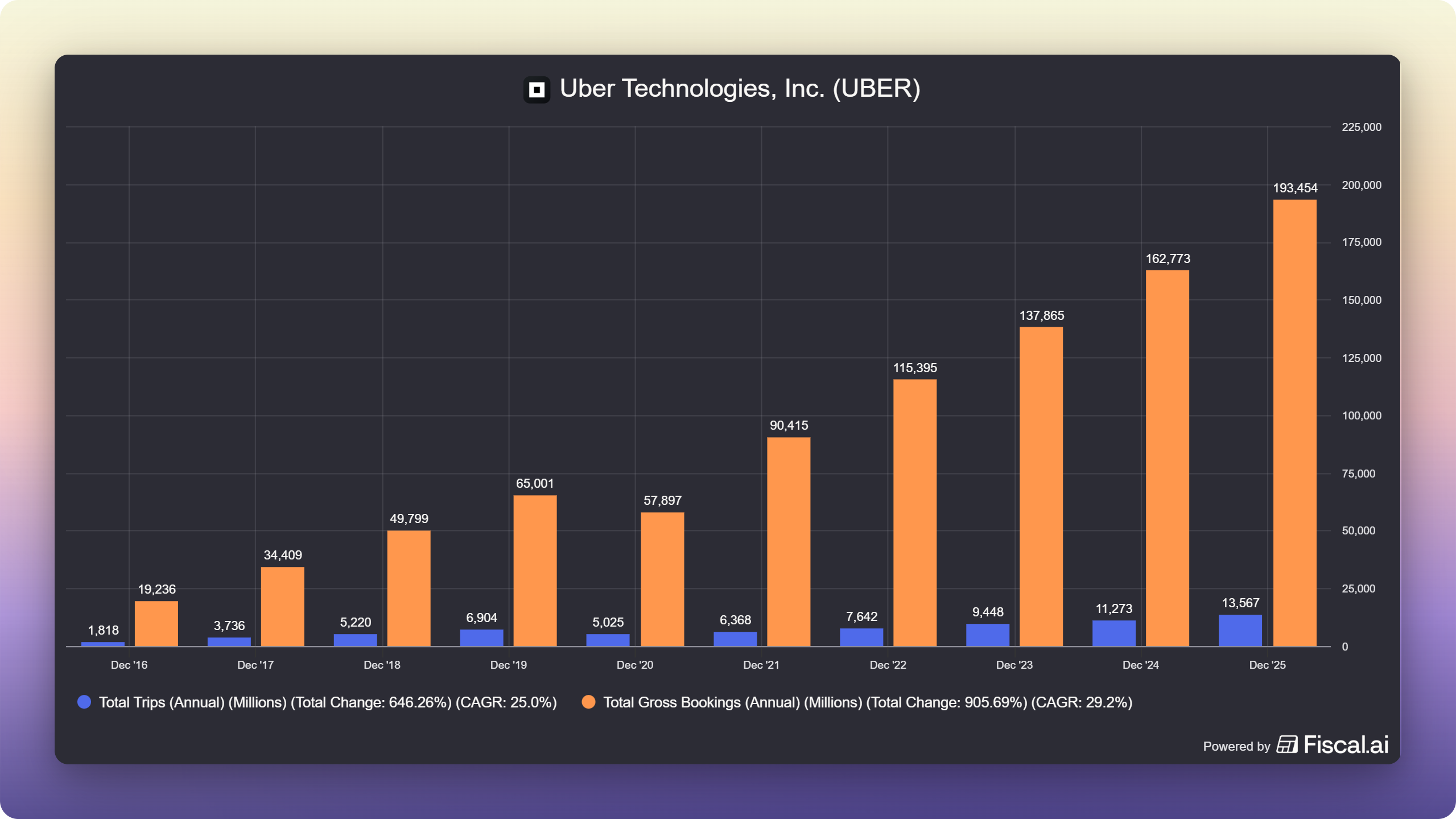

The platform connects three key groups: riders, drivers, and merchants. Through its marketplace algorithms, Uber continuously balances these groups by adjusting prices, optimizing routes, and matching supply with demand in real time. This system now operates across more than 70 countries and roughly 10,000 cities, making Uber one of the largest mobility platforms in the world.

The scale of the network is significant. In 2025, Uber had $193 billion in Gross Bookings across its platform and completed more than 13 billion trips annually. That level of transaction volume gives Uber a massive dataset on traffic patterns, rider behavior, delivery logistics, and urban mobility, which improves the efficiency of the marketplace over time.

A Platform Built Around Two Core Businesses

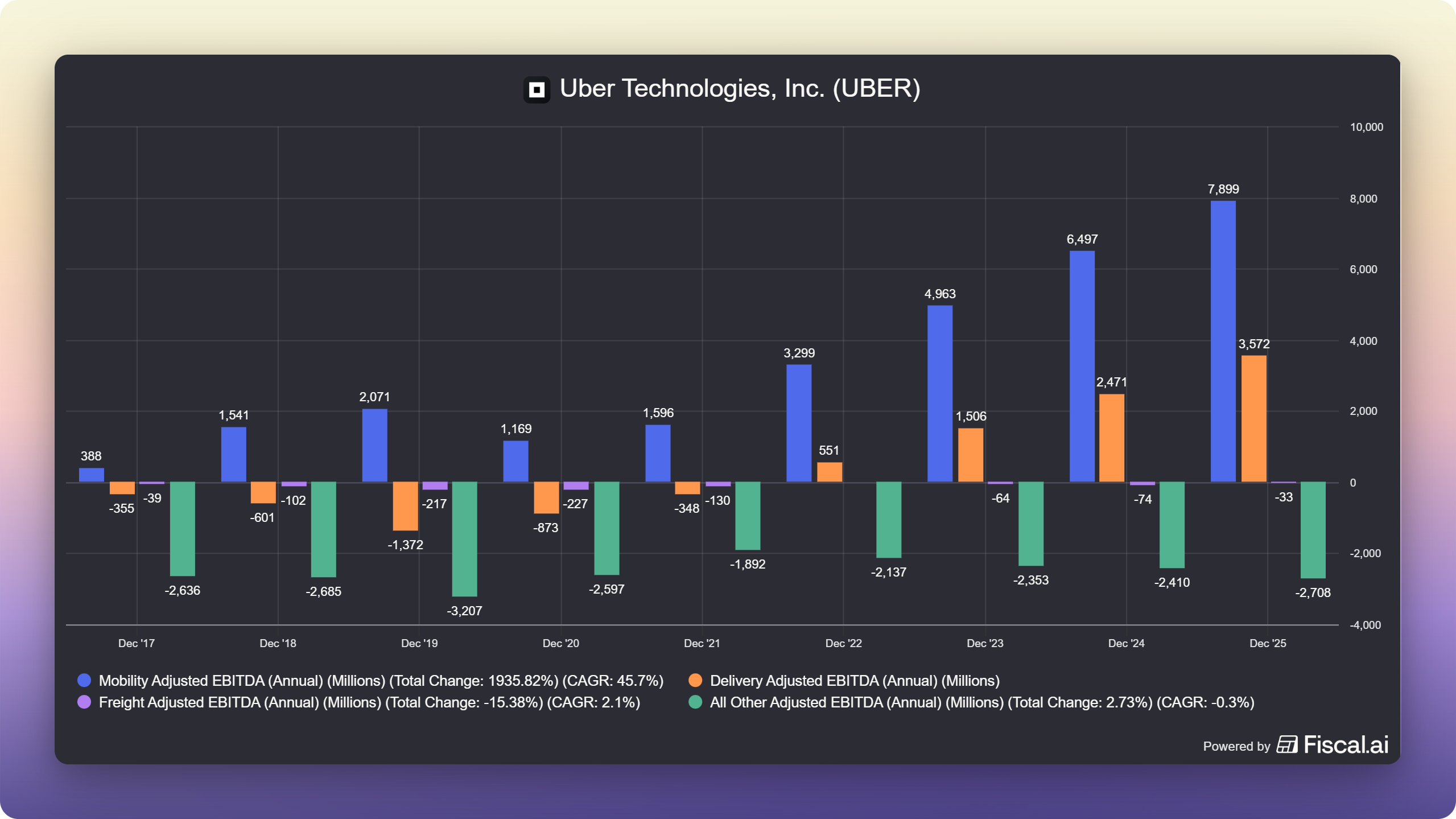

Uber’s business today revolves around two major segments: Mobility and Delivery. Mobility refers to the traditional ride-hailing service that connects riders and drivers, while Delivery includes food, grocery, and retail deliveries through Uber Eats. Both segments operate on the same underlying infrastructure, allowing Uber to leverage its driver network and logistics software across multiple services.

Mobility remains the company’s most profitable business. In 2025, Uber’s mobility segment generated an adjusted EBITDA of $7.9 billion, exceeding delivery’s adjusted EBITDA of $3.5 billion. This is largely because rides require less coordination than restaurant logistics and involve fewer middlemen. However, delivery has grown rapidly and now represents a massive marketplace in its own right, with tens of billions of dollars in annual bookings.

Uber also reports a smaller category called “All Other Adjusted EBITDA,” which includes businesses outside its core Mobility and Delivery segments. This category primarily contains Uber Freight, advertising, and newer platform initiatives that are still scaling. Because these businesses require ongoing investment, the segment has historically produced negative EBITDA. However, some of these initiatives could become meaningful profit contributors as Uber’s platform continues to mature.

The key strategic insight is that these businesses reinforce one another. Drivers can switch between delivering food and transporting passengers depending on demand conditions, which increases utilization and reduces idle time. At the same time, consumers who already have the Uber app installed are far more likely to use Uber Eats, lowering customer acquisition costs across the platform.

The Product Innovation That Created a Marketplace

From a product perspective, Uber’s breakthrough was incredibly simple. Before Uber existed, urban transportation systems were often fragmented and inefficient, with riders struggling to find available taxis and drivers wasting time waiting for passengers. Uber introduced a real-time marketplace that instantly matched drivers and riders through a smartphone app.

Three innovations were particularly important. First, the platform enabled riders to instantly discover available drivers, allowing riders to see nearby drivers in real time. Second, Uber introduced dynamic pricing, which adjusts fares based on demand and helps balance the marketplace during peak periods. Third, the company removed friction from payments by integrating automated billing directly into the app.

Together, these features created a transportation marketplace that was far more efficient than traditional taxi systems. Waiting times fell dramatically, driver utilization increased, and riders gained a predictable and transparent experience. These improvements helped Uber achieve global product-market fit remarkably quickly, turning the service into a daily habit for millions of users.

Why Marketplace Network Density Matters

The economics of Uber’s platform improve as the network becomes denser. In large cities with many riders and drivers, the system becomes significantly more efficient because the distance between supply and demand decreases. This reduces pickup times for riders and increases utilization rates for drivers.

Marketplace density also improves Uber’s margins. When drivers spend less time waiting for rides or deliveries, they can complete more trips per hour. That increases driver earnings without necessarily raising prices for consumers, which makes the platform more attractive to both sides of the marketplace.

This dynamic creates a powerful feedback loop. Faster pickup times attract more riders, which increases demand for drivers. More drivers then reduce wait times further, reinforcing the cycle. Over time, this type of network density advantage can become a meaningful competitive moat, and this effect is often referred to as “Uber’s Virtuous Cycle”:

The Transition to Profitability

For most of its early history, Uber prioritized growth over profitability. The company spent aggressively on driver incentives and rider discounts in order to build scale and outcompete regional rivals. While this strategy succeeded in establishing a global presence, it also resulted in significant financial losses.

The turning point came after Dara Khosrowshahi became CEO in 2017. Under his leadership, Uber shifted its focus toward operational discipline and sustainable profitability. The company exited several unprofitable markets, sold stakes in regional competitors like Didi and Grab, and began improving its unit economics across both mobility and delivery.

These changes gradually transformed the company’s financial profile. By 2023 and 2024, Uber had reached a point where operating leverage began to show clearly in the numbers. Revenue continued to grow, but costs grew more slowly, allowing free cash flow to expand meaningfully.

Advertising: A High-Margin Opportunity

One of the most interesting developments within Uber is the emergence of its advertising platform. Because millions of users open the Uber or Uber Eats app when they are ready to make a purchase, the platform captures extremely valuable commercial intent data. Restaurants and brands are increasingly willing to pay for placement within the app to capture that demand.

Uber’s advertising platform has grown remarkably quickly in just a few years. By May 2025, the business reached an annual revenue of $1.5 billion, growing roughly 60% YoY, making it one of the fastest-growing advertisement businesses globally. The rapid scaling reflects how valuable Uber’s ecosystem has become for brands looking to reach consumers at moments of real purchase intent.

Why Uber’s Data Is So Valuable

Uber’s biggest advantage in advertising comes from the data generated by its platform. The company facilitates more than 13.2 billion trips every year and serves over 180 million monthly users, creating a massive dataset about real-world consumer behavior.

“What is so appealing about Uber being in [40-plus countries] and serving over 180 million users is that this data set gives you the soul of the consumer,”

— Edwin Wong, Uber’s head of measurement sciences

Unlike many digital advertising platforms, Uber’s data reflects what people are actually doing in the physical world. The platform knows where users are traveling, what they are ordering, and when they are most likely to make purchases. That makes it possible for brands to place ads in highly relevant moments. For example promoting food offers during a commute home or travel products after a long flight.

New Ad Formats and What Comes Next

Uber is now expanding beyond simple sponsored listings into new ad formats. The company has installed around 50,000 tablets in vehicles, allowing brands to run video ads and content during rides.

Edwin Wong says these ads perform 11% than online video, in attention and post-checkout ad formats score 40%.

A study from Lumen found that Uber ads generate 6.6 times higher attention than online video, social, and mobile display.

Uber continues to expand these formats and build partnerships with platforms like OpenAI and OpenTable. Advertising could become one of the high-margin business segments inside the Uber ecosystem.

The Autonomous Vehicle Debate

Can you really write about Uber without mentioning autonomous driving?

Some investors believe that self-driving vehicles could eventually eliminate Uber’s role by replacing human drivers with robotaxi fleets. However, this view may underestimate the value of Uber’s marketplace and consumer habits.

Even in a world with autonomous vehicles, someone must coordinate the system. Riders still need a platform that handles pricing, routing, payments, and demand across cities. Uber already performs these functions at a massive scale, making it a natural coordination layer for autonomous fleets.

Autonomous technology is maturing, and Uber will likly transition from managing human drivers to managing fleets of self-driving vehicles.

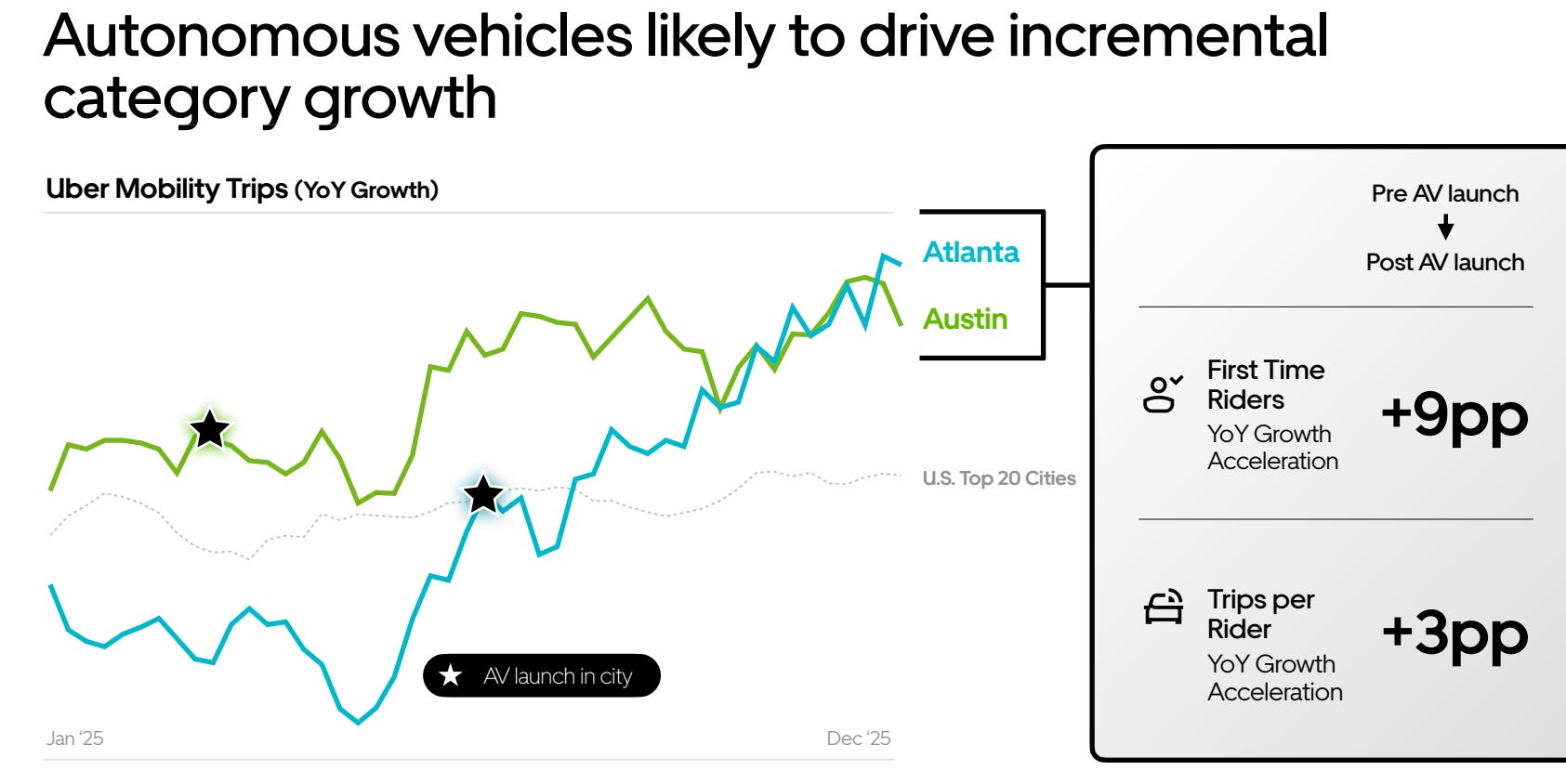

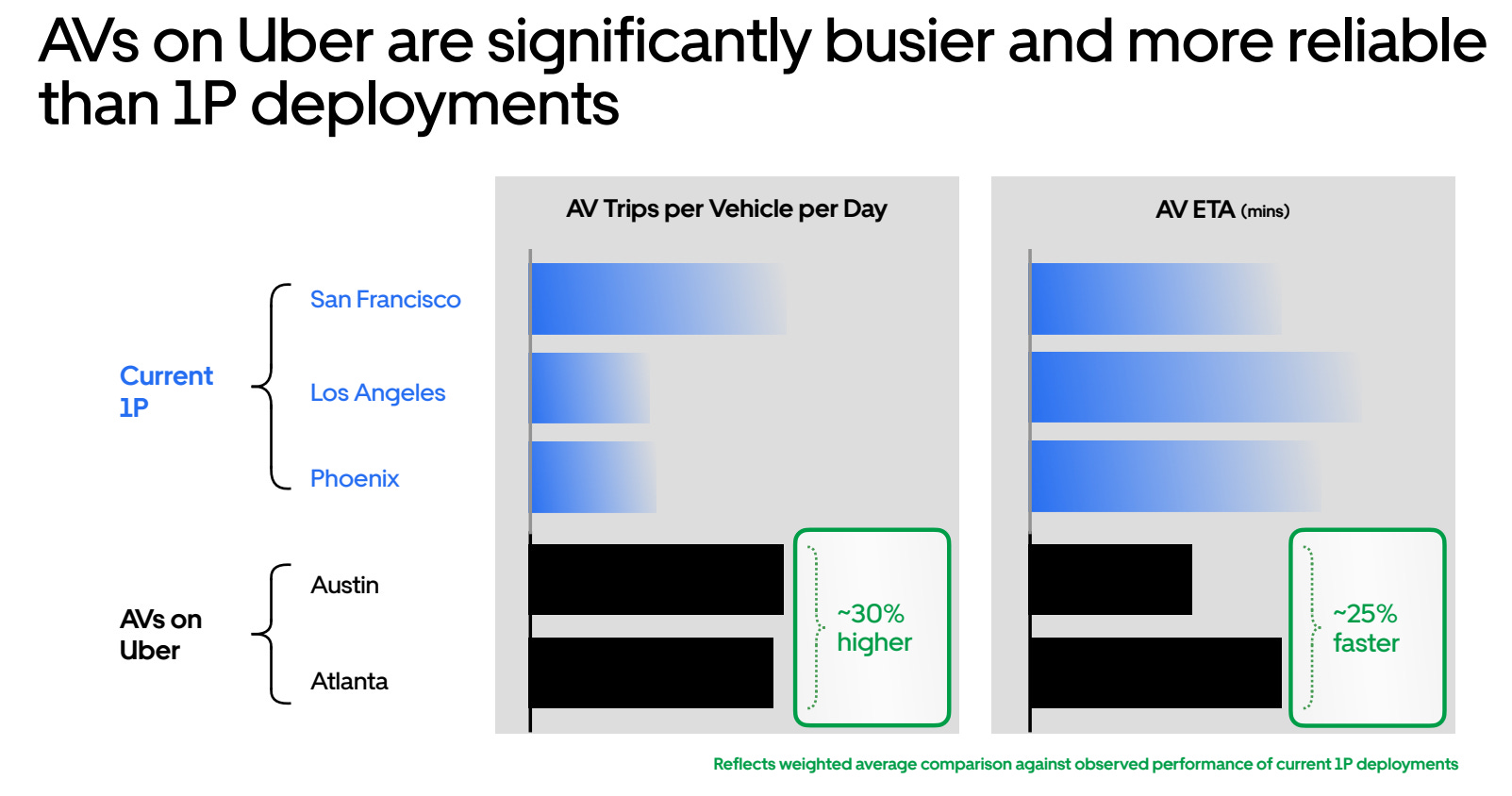

Uber is already testing AV in Atlanta and Austin, and are seeing significant results compared to the top 20 cities in the US (Gray line).

The data Uber has collects suggest that AVs are getting ~30% more trips in per day (Huge utilization boost), and are ~25% faster (Happier customers).

Many are viewing AV as a threat to Uber’s business model, but the data suggests that AV advancements will make Uber I) grow faster, II) get better utilization from their drivers, and III) get happier customers due to more efficient rides.

Uber does not need AV to be a profitable business, but it can take it to the next level, making the already capital-light company drop it’s operational expenses even lower.

The AV market is set to grow at a CAGR of 34.5% to +$3 trillion in 2033. Uber is well-positioned to take a piece of that market.

Valuation: Is Uber undervalued?

Uber’s long-term valuation depends on two things:

How fast the platform continues to grow

How profitable the marketplace becomes as it scales

In a bear case, growth slows as ride-hailing and delivery mature and competition limits pricing power. Revenue grow ~5% annually, EBITDA margins stabilize around 15%, and free cash flow grows roughly 5% per year, which could justify a 12x FCF multiple in ten years.

In a base case, Uber keeps executing well across Mobility and Delivery while advertising becomes a meaningful profit driver. Revenue grows around 10–12% annually, EBITDA margins expand toward 25%, and free cash flow compounds at roughly 15–18% per year as operating leverage improves. In that scenario, a scaled but still growing platform could trade around 18–20x free cash flow.

The bull case assumes Uber fully leverages its global marketplace. Advertising becomes a large high-margin business, the network becomes more efficient, and new opportunities such as autonomous fleets or logistics expand the platform. Revenue could grow 15%+ annually, EBITDA margins approach 30%, and free cash flow compounds +20%+ per year, potentially supporting a 25x+ multiple for a highly cash-generative global platform.

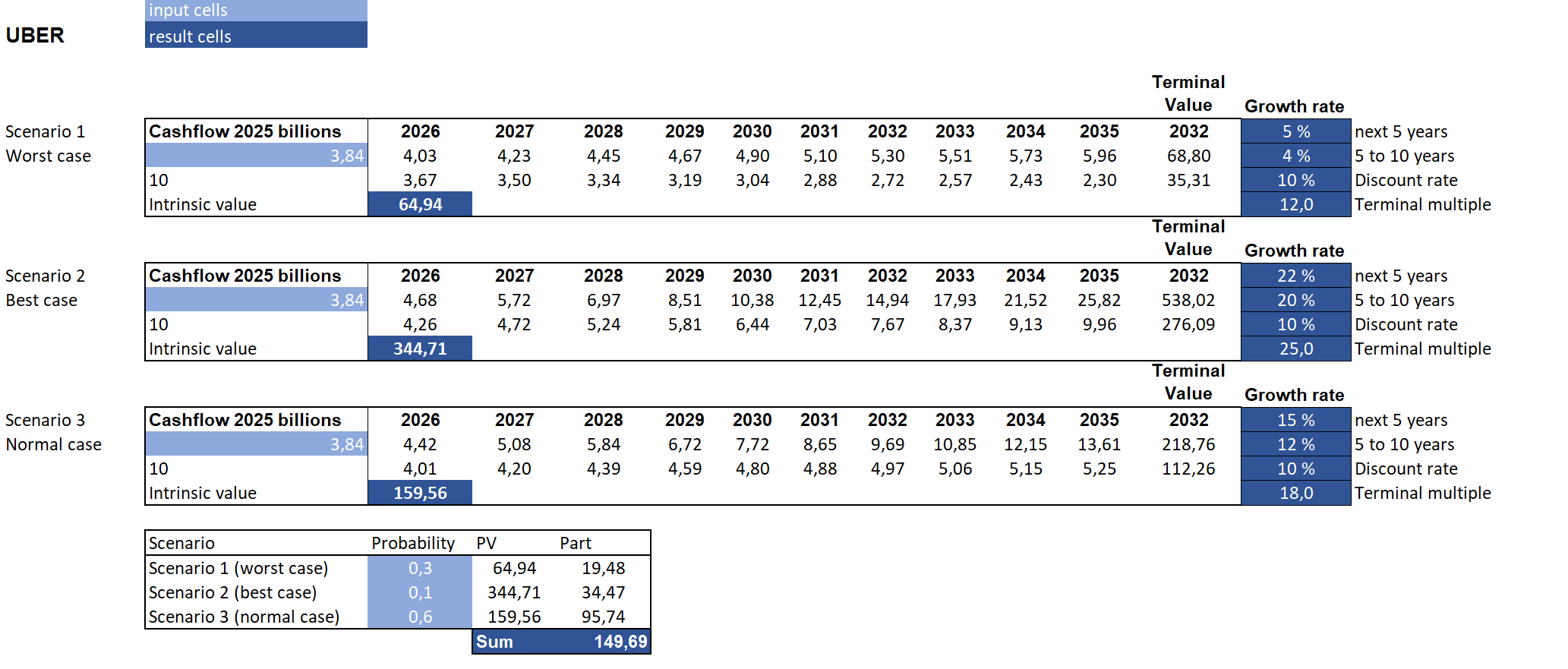

The TTM free cash flow per share is $4.6, but if we exclude stock based compensation, we arrive at $3.84. I like to exclude SBC because it is a real cost for investors, as you get diluted over time.

The discounted cash flow analysis:

Fair value estimate: $149,69

Current share price: $73.35

Upside: +104%

Expected CAGR from base case: +20%

The large difference between our fair value estimate and the current share price tells us that the market is pricing in a lot of pessimism and risks.

Competition is one factor, AI is another, and many are looking at AVs as the bear case and risk factor for Uber.

For Uber to not provide a solid return over the next 5 to 10 years, the business must really fall apart, only growing its free cash flows at 4-6% annually, and trading at a 12x multiple.

In other words, the market is pricing in that Uber will get distrupted, most likely from automonous vehicles.

If you believe in the base or bull case for Uber, the valuation looks very attractive at its current levels.

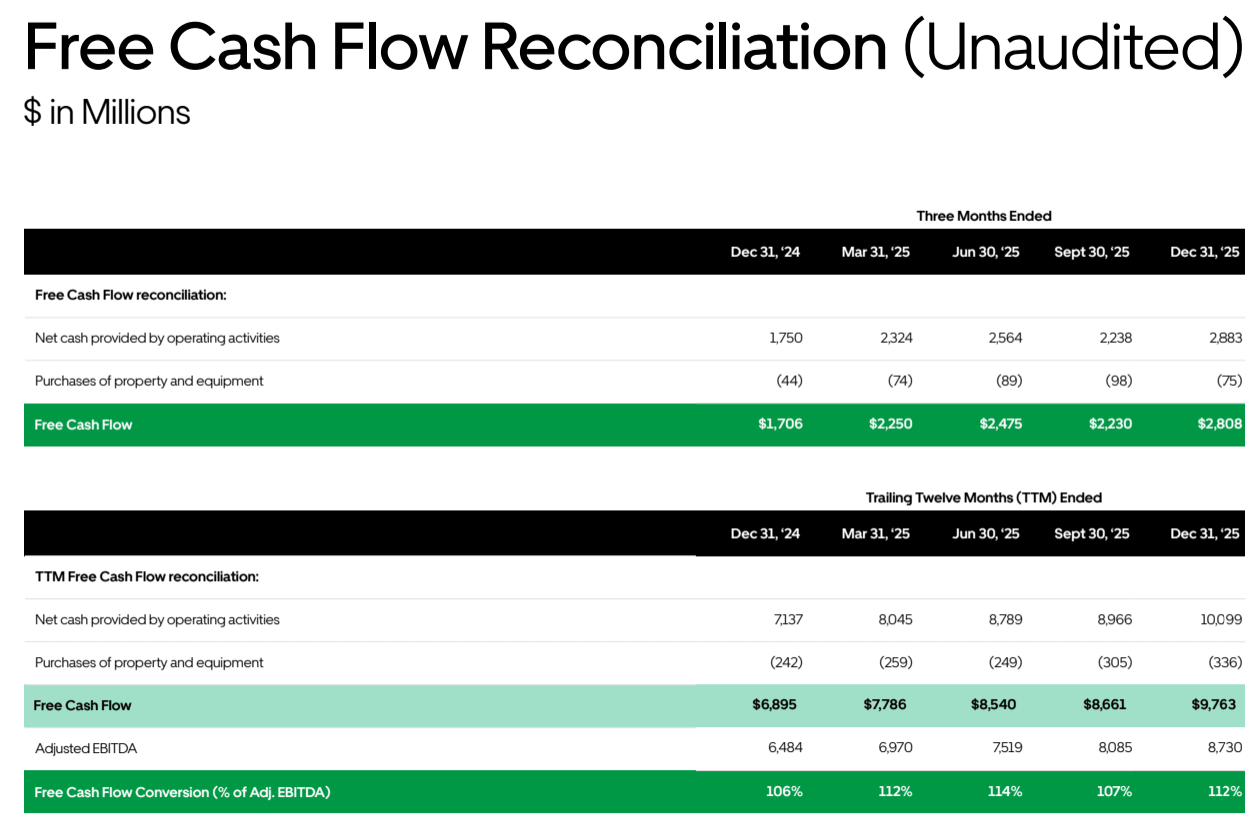

The last few months of free cash flow growth has been stunning, and is coming from a significant increase in the net cash from operating activities, with a free cash flow conversion rate of >100%:

Risks Investors Should Consider

Despite its progress, Uber still faces several risks. Regulatory scrutiny remains one of the most important factors, particularly regarding the classification of drivers as independent contractors rather than employees. Changes in labor laws could increase operating costs in some markets.

Competition is another factor to watch, particularly in the food delivery segment. Companies such as DoorDash continue to compete aggressively for market share in the United States, while regional competitors remain strong in some international markets. These dynamics can pressure margins and limit pricing power.

Finally, the company’s demand is somewhat cyclical. Economic downturns can reduce discretionary spending on rides and restaurant delivery, which could temporarily slow growth. However, Uber’s global scale and diversified services help mitigate some of these risks.

The Long-Term Investment Question

Uber today is a fundamentally different company than it was five years ago. The platform has reached global scale, the marketplace economics are improving, and the business is generating significant free cash flow. This suggests that the company is maturing and settling in as a quality market leader.

At the same time, the long-term opportunity may still be larger than many investors realize. Urban mobility, food delivery, local commerce, and logistics represent enormous markets that continue to shift toward digital platforms. Uber’s position at the center of these ecosystems gives it a strong foundation for long-term growth.

The proven effectiveness of Uber’s advertisement business and its distribution and data makes it appealing as a possible growth driver in the coming years. Additionally, advancements in autonomous vehicles is more likely to be a growth driver and profit enhancer for Uber, than an existential threat.

Uber has done a fantastic job of expanding its network, improving its unit economics, and building new monetization layers like advertisiting. If the business continue to hold its position as a market leader, with the best distribution, data, and infrasctructure in mobility, the business may have far more compounding potential than the market once believed.

Join the Premium Research

Free subscribers get occasional articles.

Premium Members get the full investing framework.

Including:

💎 Full Portfolio Access (80% of my net worth invested alongside members)

📢 Real-Time Buy & Sell Alerts

📊 Monthly Portfolio Factsheets

🏰 Quality Deep Dives

📘 Complete Research Archive

Everything is built around one goal:

Identifying businesses capable of compounding capital for decades.

Become a Premium Member👇

Note: The price will increase 50% on April 1st.

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 45% open rate. Reach out: investinassets20@gmail.com

The largest component in expenses of Uber is Driver commission. Autonomous vehicles will reduce that expense component by a significant margin. So much so that Uber may also try to lease their own AVs and generate long term profits. People are not factoring this into the Uber's valuation.

AV is not a competition, it will be a feature.

Waymo and Tesla may work on producing AV systems, but Uber's gloabal reach may compel them to ultimately supply their vehicles to Uber's platform.

I see that you haven't talked about net profits but EBITDA only. At the end the price of stock depends on real profits. What is your view on that?

6.3% FCF yield on a business where Waymo is actively eating into their core market in every city they expand to. Uber became FCF positive in 2023 after burning $14B over a decade. That 20% growth assumption prices in platform dominance, not a world where the car itself becomes the competitor. The moat looked obvious at Amazon too, right before AWS competitors emerged.