Top 5 Buys May 2026 🚀

Mr. Market is discounting high quality businesses 💎

Hi partner! 👋🏻

Welcome to the May edition of Top 5 Buys ✅

You can access our Top 25 Buys for 2026 list as a premium member here.

In this article, we will discuss our top stock picks for May 2026.

Let’s get into it 👇

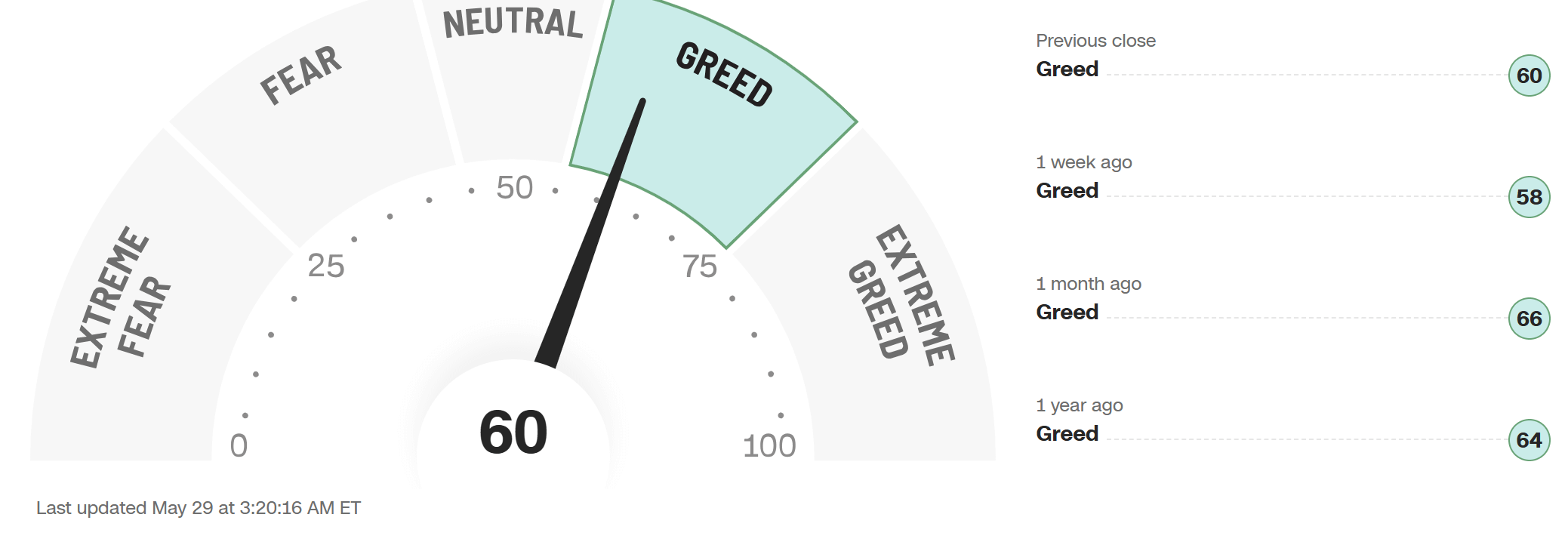

The Market Sentiment: Greed

After the chaos of April, tariff announcements, geopolitical noise, and a brief detour into Extreme Fear, the market has bounced back with surprising speed. Investor sentiment has settled around Greed, as the S&P 500 reclaims ground near all-time highs.

The investors who acted in April have already been rewarded. Now the question is whether this recovery holds, or whether the underlying uncertainty reasserts itself.

Honestly? It doesn’t matter that much. What matters is finding businesses that compound regardless of what the macro throws at them.

I can’t predict the future, but I can point to 5 quality growth businesses that continue to compound regardless of macro economics.

Here are this month’s Top 5 Buys 👇

This is not investment advice. Always conduct your own due diligence and make your own investment decisions.

Top 5 Quality Buys May 2026 🚀

#1 of 5🏛️ Kinsale Capital KNSL 0.00%↑

Technology-Driven Insurance Compounder · $KNSL · Richmond, Virginia

E&S Insurance

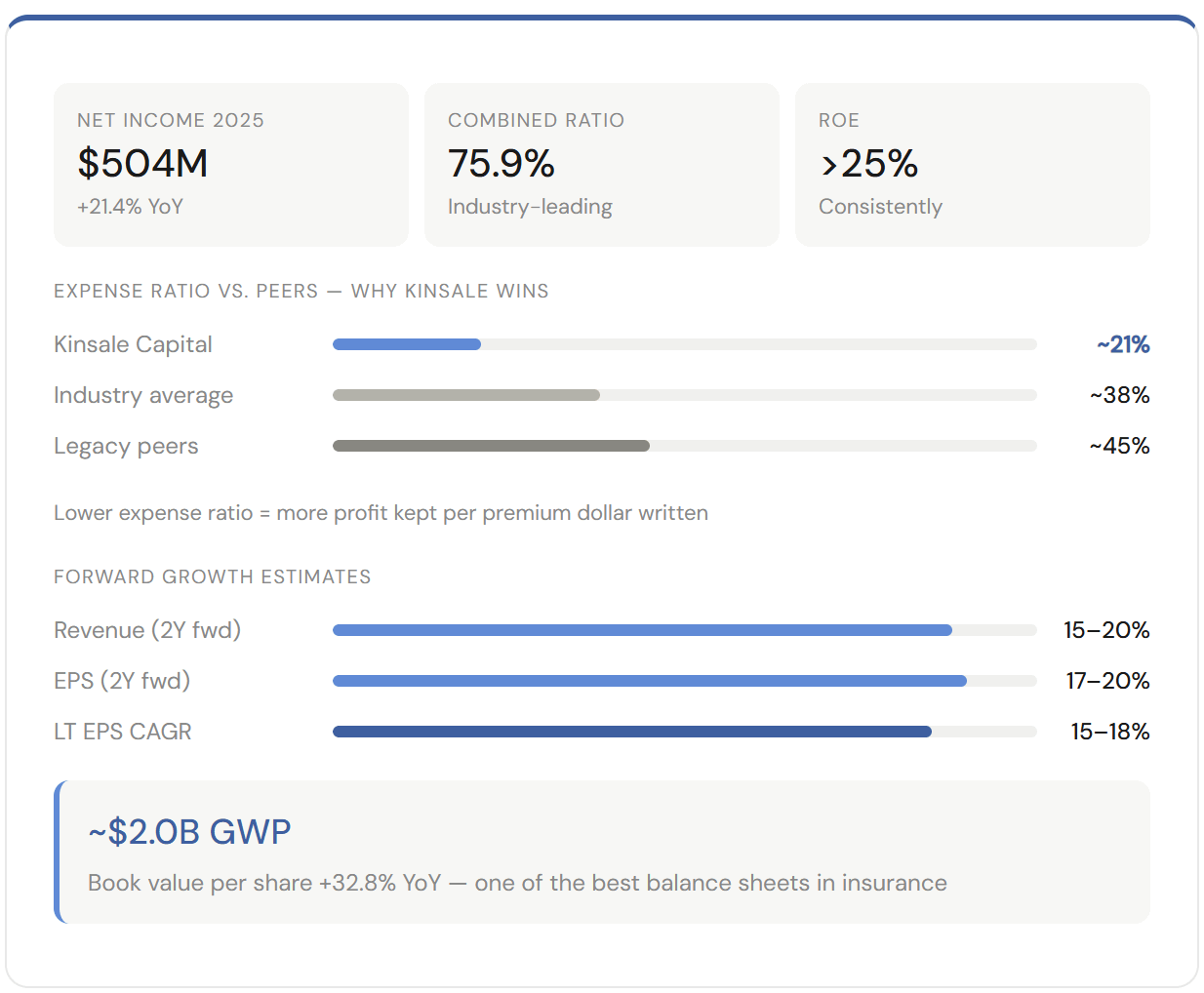

Kinsale Capital ($KNSL) is the best business model in insurance. A pure-play Excess & Surplus (E&S) lines specialist that has turned underwriting into a competitive advantage. Since IPO in 2016, Kinsale has compounded shareholder returns 33.6% annually by doing something deceptively simple: insuring risks that standard carriers won’t touch, faster and cheaper than anyone else.

The E&S market exists because some risks are too unusual, complex, or volatile for standard insurance markets. Think cannabis businesses, cyber liability, construction projects in difficult environments, and emerging industries. It’s a great business to be in, if you can underwrite like Kinsale Capital does.

The Model: Tech Advantage in a Legacy Industry

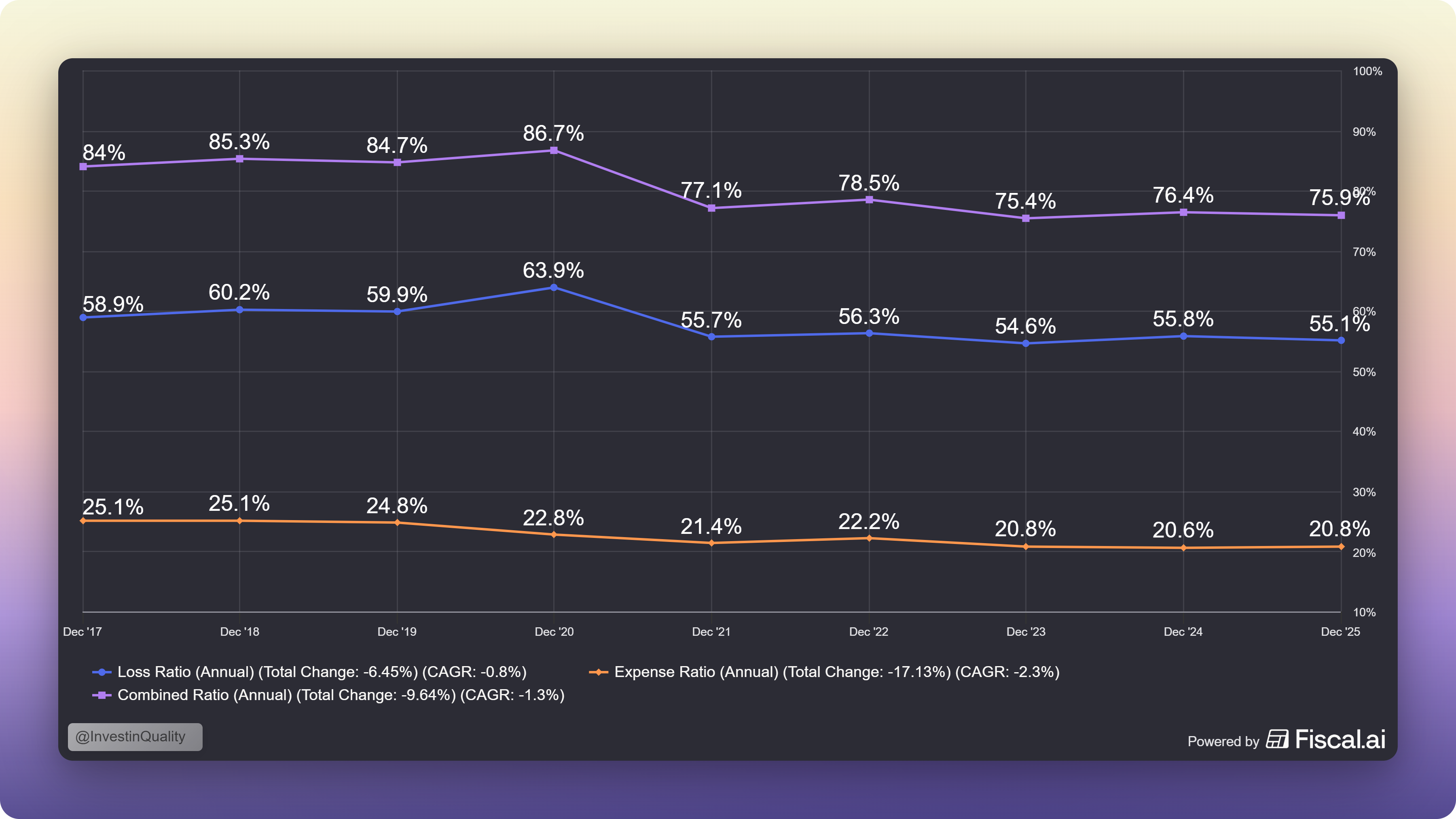

The insurance industry runs on legacy IT. Old systems, slow quoting, manual underwriting. Kinsale built its entire platform from scratch, proprietary technology enabling faster quoting, better data capture, and more granular risk selection than any competitor. The result is a structural cost advantage. Kinsale’s expense ratio sits around 20–21%, this is one of the lowest in the E&S market. Combined with disciplined underwriting producing a combined ratio in the mid-to-high 70s, Kinsale is generating ROE consistently above 25–30%. Legacy competitors can’t close this gap. Their infrastructure is too expensive to replace.

Growth Drivers

E&S market expansion: The E&S market has been taking share from standard lines for years as risk complexity grows. Kinsale is perfectly positioned as a pure-play operator.

Technology flywheel: As Kinsale writes more policies, its data advantage improves. Better data → better pricing → better loss ratios → more capital to grow.

Small-to-mid market focus: Kinsale targets smaller, more fragmented accounts where broker relationships are stickier and competition from large carriers is weaker.

Investment income: A growing float invested at improving rates adds a compounding tailwind to earnings.

The Numbers

Kinsale is trading at its lowest forward PE in over a decade, of 14.77x.

Despite the historical low levels, it still trades at a premium to other insurance businesses, as it should, with much higher combined ratio, return on equity and growth.

The unit economics for Kinsale Capital is one of the most durable in financial services.

Bottom line

Kinsale is a rare investment case, a financial company with a genuine technological moat. Insurance is typically a commodity. Kinsale has made it a compounding machine by building technology that incumbents can’t replicate without tearing down everything they have. The E&S market is growing, the advantage is durable, and management has been disciplined throughout. This is the kind of business you want to own for a decade.

#2 of 5 🌸 Interparfums IPAR 0.00%↑

Asset-Light Fragrance Compounder · $IPAR · New York, USA

Luxury Fragrance

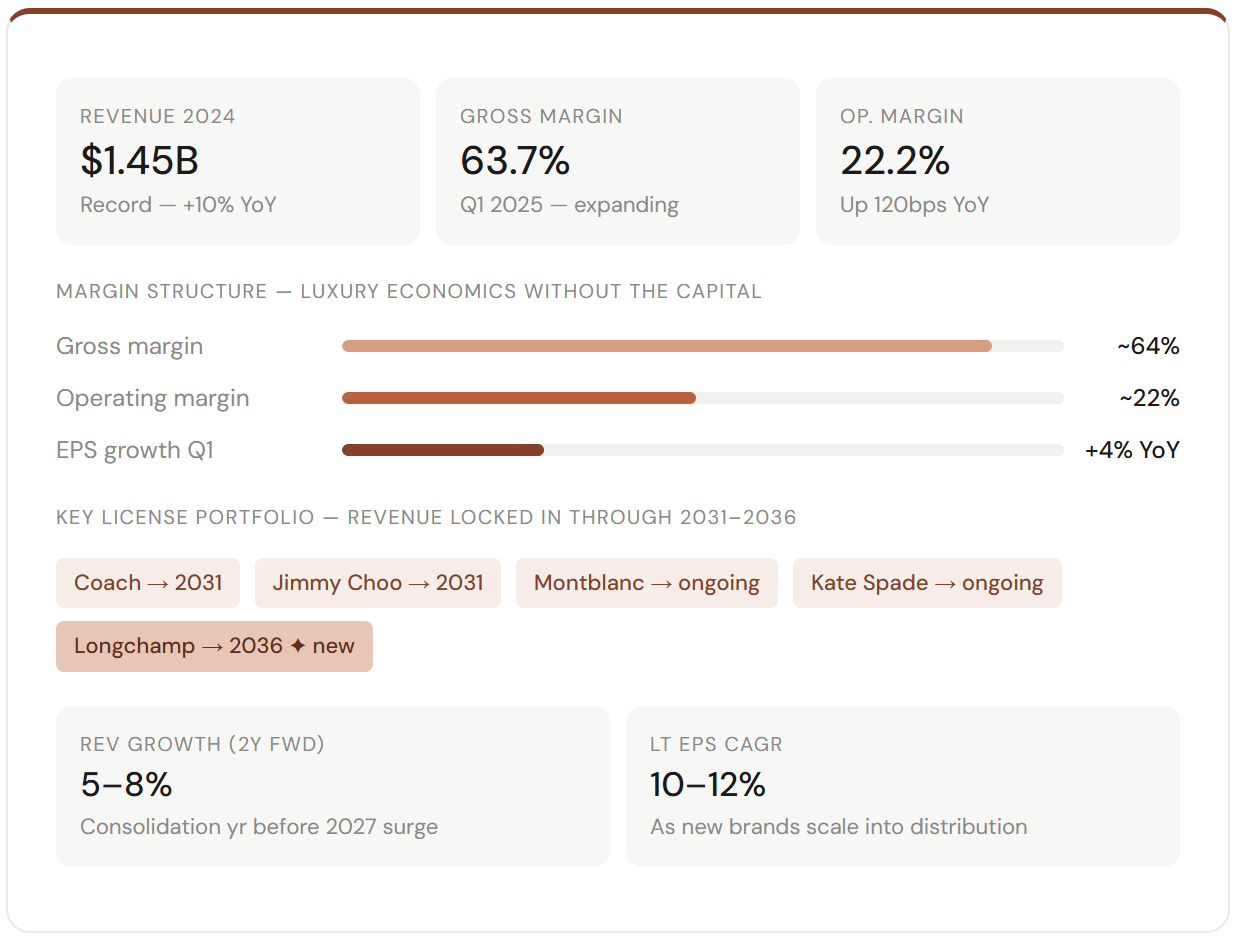

Interparfums ($IPAR) is one of the best-kept secrets in consumer goods. It’s not a luxury house. It doesn’t own the brands. It licenses them, and that distinction is crucial.

The model is elegant: Interparfums signs long-term exclusive licensing agreements with prestigious fashion brands (Coach, Jimmy Choo, Montblanc, Kate Spade, Karl Lagerfeld, and more), then handles the creation, manufacturing, and global distribution of fragrances under those brands. The brand owner gets royalties without operational headaches. Interparfums captures the economics of luxury fragrance with a fraction of the capital intensity.

The Model: Licensing as Leverage

The fragrance business is incredibly attractive. Gross margins are thick, products have long shelf lives, gifting occasions are recurring, and prestige brands command premium pricing. The Coach license was just renewed through June 2031. A new license with Longchamp (through 2036) was signed in July 2025. The portfolio is diversifying and lengthening.

Growth Drivers

Jimmy Choo franchise strength: The “I Want Choo” franchise is a genuine hit. Jimmy Choo is growing around 16% annually.

New license pipeline: Longchamp launches in 2027. New brands entering the portfolio add future growth optionality.

Global prestige fragrance tailwind: Consumer demand for prestige and luxury fragrance remains robust even as consumers become more selective elsewhere.

Geographic expansion: North America, Western Europe, and Asia/Pacific all strengthened in 2024–2025.

The Numbers

2026 is a consolidation year by management’s own guidance, they’re laying the groundwork for a strong 2027 as new brands ramp. For long-term investors, that creates a window.

Combine this with the drop in valuation over the past years. Interparfums is now trading at a 7.92% forward free cash flow yield, and a 18.7x fwd. PE ratio, it’s cheapest valuation in over a decade:

Bottom line

Interparfums is a textbook asset-light compounder. It has captured the economics of luxury fragrance without the capital intensity of building a luxury brand. The licensing model is misunderstood by investors who worry about renewal risk, but the track record of renewals and an expanding portfolio makes this business far more durable than it appears. Patient investors who look through the 2026 consolidation year will likely be rewarded in 2027 and beyond.