Top 5 Buys March 2024 🏰

5 Undervalued Quality Companies 🧠

The Greed to Fear index is pointing towards Greed

The market has been in Greed & Extreme Greed territory for a while now. If we look at 1 year ago, the market was in “fear” - usually this provides better entries for stocks as the overall market tends to fall, dragging quality investments with it.

The S&P 500

The S&P 500 keeps pushing all-time highs - driven mostly by 7 companies in the index, “The Magnificent 7”: Microsoft, Apple, Amazon, Meta Platforms, Nvidia, Alphabet and Tesla. These 7 companies make up 29% of the S&P and were responsible for 61.5% of the performance in 2023. This means that the remaining 38.5% of performance was spread among the 493 other companies in the S&P 500. This makes you think twice about the diversification you are getting from index funds currently. It also tells us that it is not the US stock market that has performed very well, it is mostly the Mag 7 that has.

Mr. Market

Mr Market always offers us deals. When some stocks rise quickly, others lag or decline due to temporary issues or a range of different factors. The month of March is no different. A few high-quality companies have sold off due to short-term headwinds.

This provides possible entry points for us as investors.

What is a good buy?

I have outlined in my book and my valuation cheat sheet how I value businesses. There are several methods one can use, but I like to keep it simple. First I want to understand the business, how it makes money, the different business segments, and the growth potential for each segment or product/service and market. Then I look at historical multiples to get an idea of what the company has traded at, as well as the development of margins and capital efficiencies over time. I then use a discounted cash flow analysis and a reverse DCF analysis to determine what I believe the company will return.

Here are the top 5 buys for February from the Quality Growth universe:

Check out the top 5 buys for February 2024 here:

Disclaimer: This is not investment advice, always do your own due diligence and make your own investing decisions.

Top 5 Buys March 2024

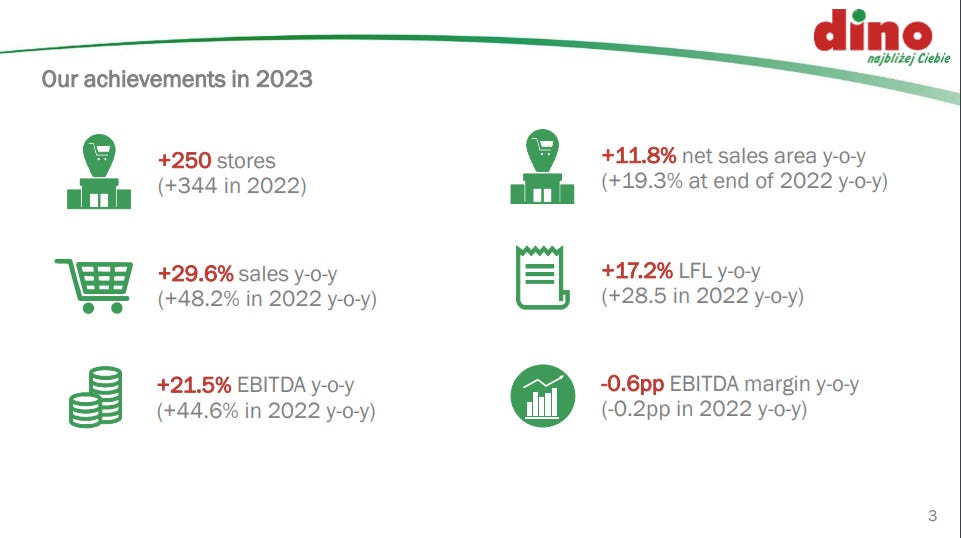

Dino Polska DNP 0.00%↑ 🛒

Dino Polska is a Polish retailer that sells food, beverages, and tobacco. Dino Polska has quickly expanded all over Poland and is set to continue to expand its network of stores. The founder still owns ~50% of the business.

Key Fundamentals:

OCF 5-Year CAGR: 18.13%

Gross Margin 23%

Interest coverage 13.7x

Operating Margin 7.33%

ROCE 5-Year 25.8%

EPS 5-Year CAGR 35.5%

CAGR since inception 39.1%

Valuation and buy area

Dino Polska is an amazing growth story from Poland. The business owns the real estate where it builds its retail stores, and has been aggressively expanding in Poland. A key thing to follow would be whether or not Dino can expand beyond Poland, as their stores now cover the entire country. At some point, they would need to expand to other nations to continue to grow.

The current price of Dino Polska is PLN 370 per share. Given my estimates in dark blue below, I’m expecting a ~12.5% annual return from the current valuation. These are conservative estimates to mitigate risk and due to the “emerging market”-discount we often see on these kinds of companies. Dino is currently attractively priced, and one could argue that now is a decent time to enter the stock.

High growth expectations

Dino is expected to grow fast — 27% EPS growth for the next 2 years, and 23% long-term EPS growth. This is amazing, and looking at the historical growth, they have delivered in the past. But we don’t invest in the past, we have to look ahead.

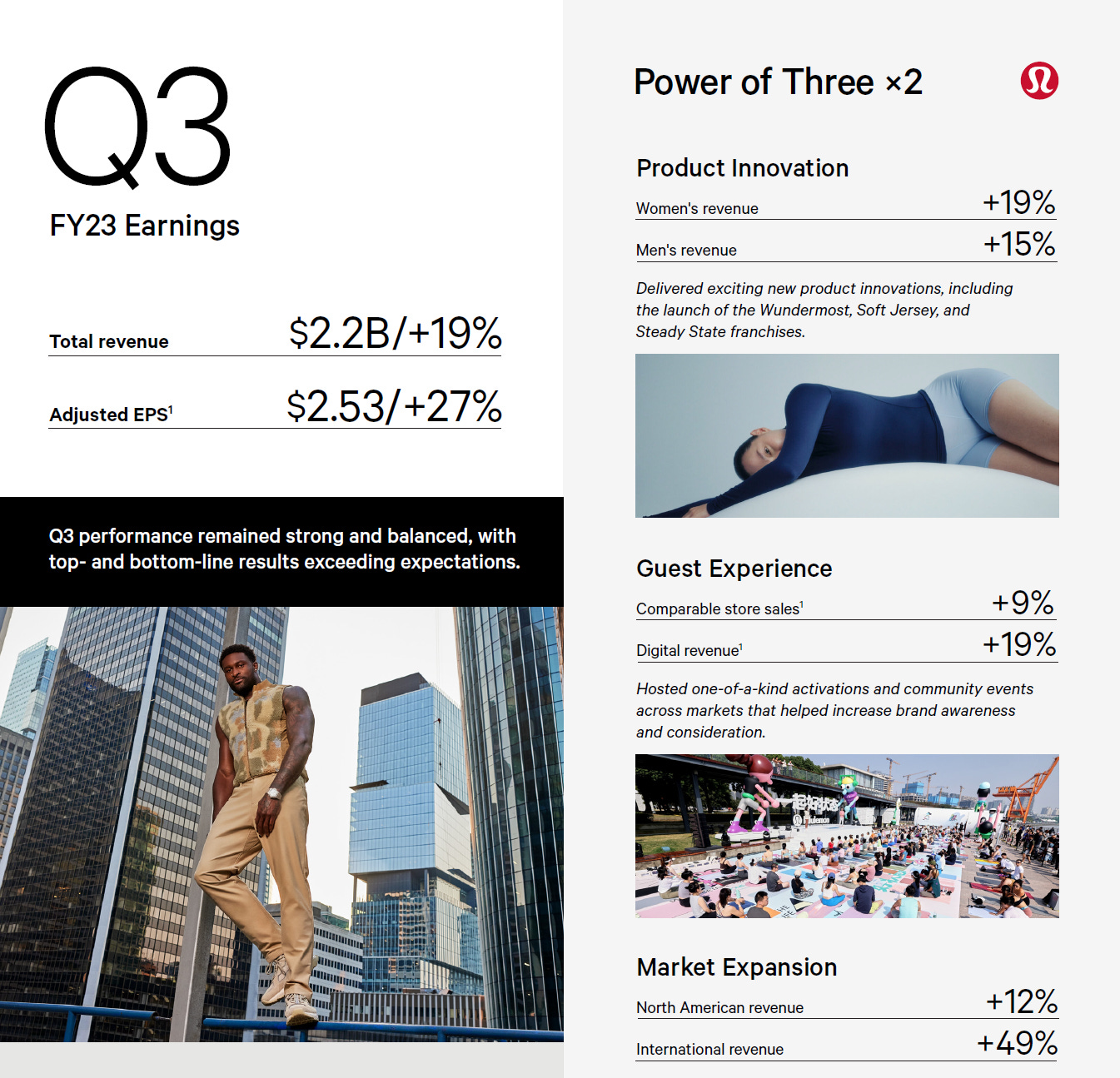

Lululemon LULU 0.00%↑ 💎

Lululemon Athletica designs, distributes, and markets athletic apparel, footwear, and accessories for women, men, and girls.

FCF 5-Year CAGR: 27.5%

Gross Margin 58.3%

Operating Margin 22.2%

ROCE 5-Year 33.4%

EPS 5-Year CAGR 27.6%

CAGR since inception 22.1%

Valuation & Buy Area

Lululemon recently released its annual report, which was not well received by the market. It is not on a ~20% fallback from its top levels. Considering the quality and growth potential for Lululemon, we believe it is fairly priced at current levels. Lulu has grown quite a bit in the past, and the projections for future growth are between 15-17% annually. Lulu could very well hit these estimates, but there is a risk in the short term that sales will be softer than expected, and hence, short-term stock prices could drop further.

Our model suggests that Lulu is trading below intrinsic value, and is fairly priced currently, given the normal growth scenario (Scenario 3).

The rest of the article is for Premium Subscribers only, consider subscribing: