Top 5 Buys June 2026 💎🏰

Quality is finally getting cheaper...

Hi partner! 👋🏻

Welcome to the June edition of Top 5 Buys ✅

You can access our Top 25 Buys for 2026 list as a premium member here.

In this article, we will discuss our top stock picks for June 2026.

Let’s get into it 👇

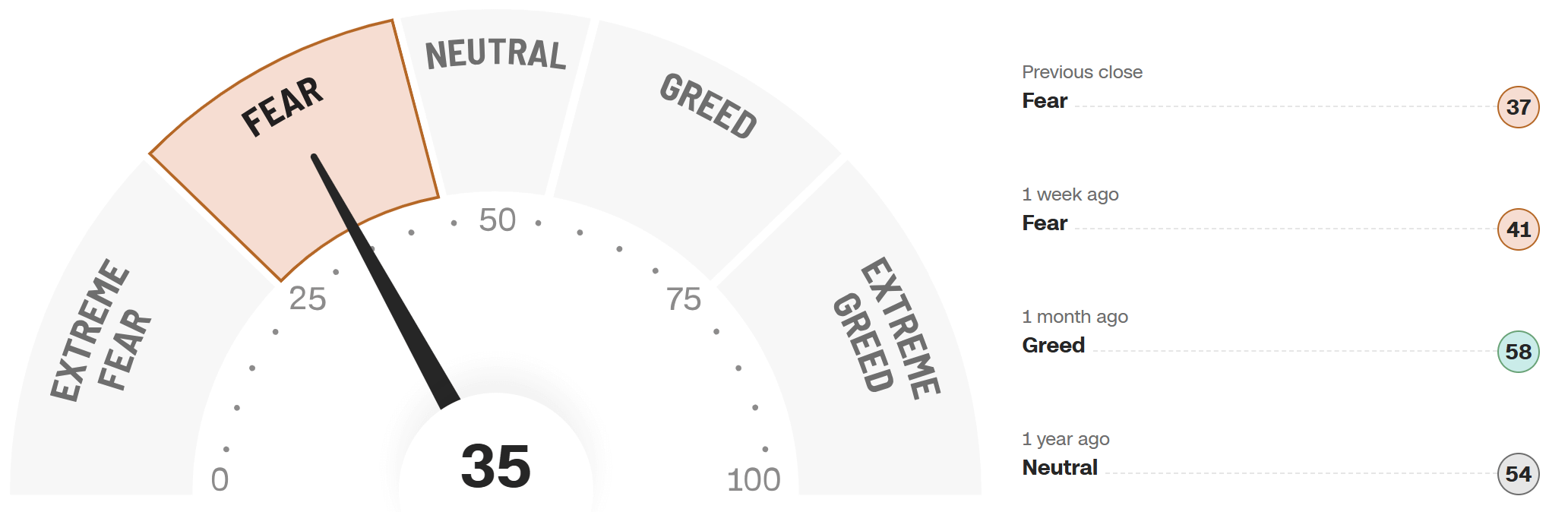

The Market Sentiment: Fear

A month ago, the market was flirting with Greed, then the Strait of Hormuz situation escalated, the oil price spiked, and the Fear & Greed Index dropped to Fear territory at 35:

This is the overarching trend of 2026 so far. The fear and greed cycle on steroids. Tariff scares in April, recovery in May, geopolitical shock in June, and whats next?

Every few weeks the market finds a new reason to panic, sells off, then mostly forgets about it a few weeks later.

I don’t trade the index. But I do pay attention to what it tells me: when fear shows up, prices move before fundamentals do. That gap is where buying opportunities exist.

This month’s five picks all share something in common. Each one reported strong fundamental momentum recently, and each one has seen its share price disconnect from that momentum, for reasons that have little to do with the actual business.

Here are this month’s Top 5 Buys 👇

This is not investment advice. Always conduct your own due diligence and make your own investment decisions.

Top 5 Quality Buys June 2026 🚀

Meta Platforms META 0.00%↑ 📱

The preferred digital advertisements platform is building its own AI infrastrucutre.

Social Media & AI Infrastructure

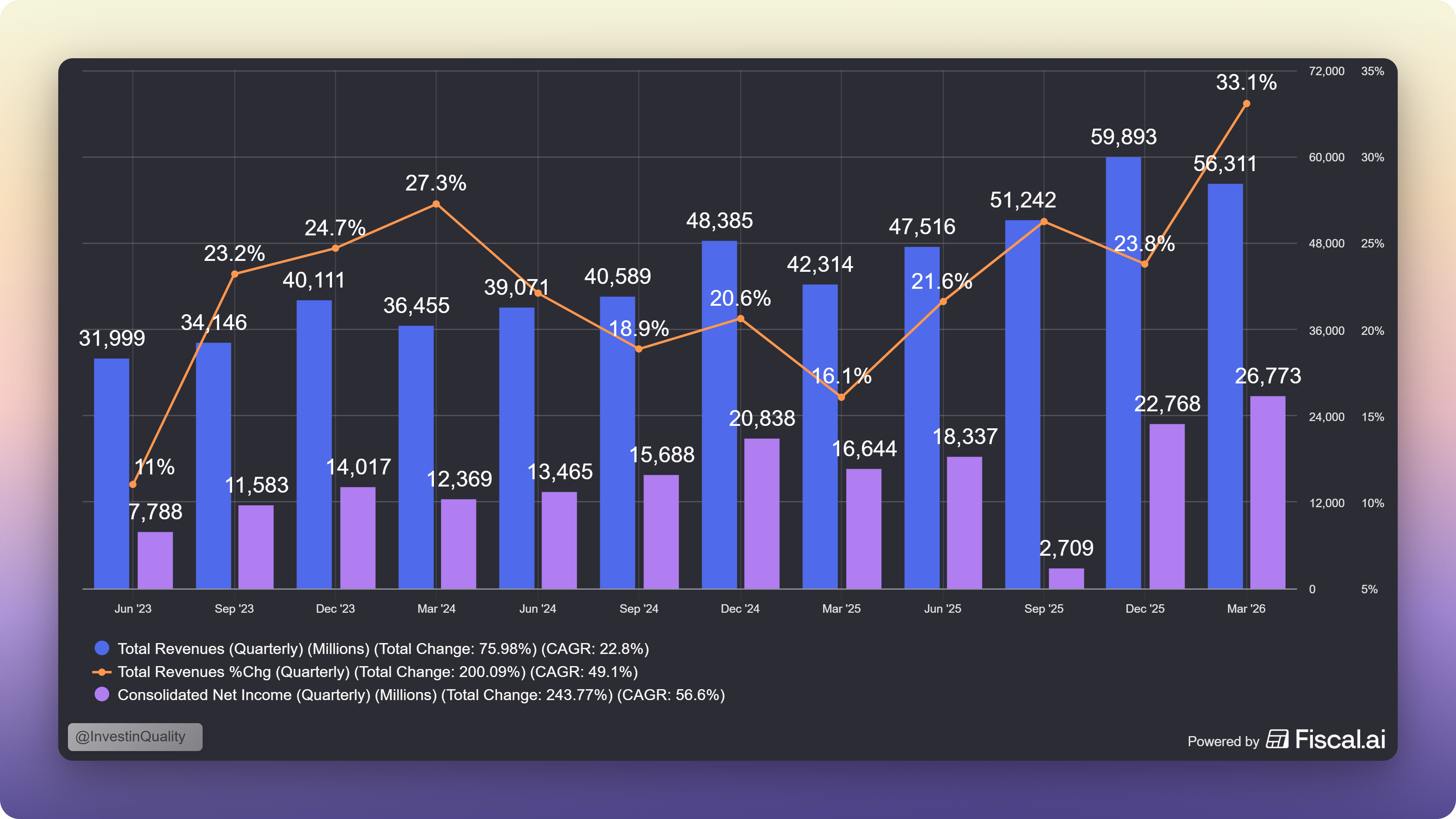

Meta just delivered one of its strongest quarters in years, and the stock is still down roughly 17% over the past 52 weeks. Q1 2026 revenue grew 33% year-over-year to $56.3 billion, beating estimates. Net income reached $26.7 billion. And the market’s response has been to focus almost entirely on the capex number.

Meta guided 2026 capital expenditure up to a range of $125 billion to $145 billion to fund AI infrastructure and data centers. That’s a lot of money.

But despite the result from the AI investment, the fundamental business of Meta is throwing off enormous free cash flow from an advertising engine that is getting more efficient (And more effective with the use of AI).

The market is pricing Meta like an AI cost center. The Q1 numbers say it’s still primarily an advertising compounder that happens to be investing heavily in its next potential leg of growth.

The Model: Distribution First, Monetization Second

Meta’s core business has always followed the same playbook: build the platform people spend the most time on, then monetize that attention better than anyone else.

Facebook, Instagram, WhatsApp, and Threads collectively reach close to half the world’s population. That distribution is the moat, and it creates a lot of optionality and new potential revenue streams for Meta.

AI is simply the newest lever for squeezing more value out of it; better ad targeting, better ranking algorithms, and now entirely new product surfaces like AI-powered Business Agents inside WhatsApp, Instagram, and Messenger.

Growth Drivers

Ad efficiency from AI: Better targeting and creative generation tools are lifting advertiser ROI, which supports continued pricing power even as impression growth moderates.

According to Meta, “For every $1 advertisers spent using Advantage+ shopping campaigns, they saw 17% more purchases compared to advertisers who used manual shopping campaigns.” (Source: Meta for Business)

Business Agents: A global AI-powered agent now operates across WhatsApp, Instagram, and Messenger, aimed at small and medium businesses that previously couldn’t afford a dedicated marketing or customer service function. This is a new revenue stream for Meta.

Instagram Plus and AI subscriptions: Meta is testing premium, ad-light tiers, an early step toward diversifying revenue beyond pure advertising. Meta expects a 1-2% conversion rate on Instagram and Facebook plus. The two platforms have 2.35 billion and 3.07 billion monthly active users.

Let’s do the math at $3.99 per month:

1% conversion = 5.42 x 0.01 x 3.99 = $216 million monthly recurring revenue

2% conversion = 5.42 x 0.02 x 3.99 = $432 million monthly recurring revenue

This growth comes at very low additional operational costs, as Meta already has the infrastructure in place, they just monetize the distribution they’ve already built.

The Numbers

Meta trades at a forward P/E of 16.76x, a meaningful discount to where it traded for most of the past two years, despite revenue growth accelerating.

Return on invested capital sits at 24.3%, exceptional for a company spending this aggressively on infrastructure.

The PEG ratio is 0.8, which tells you the market isn’t pricing in much credit for growth at all right now. That’s unusual for a business compounding earnings the way Meta currently is.

Bottom line: Why now?

Meta is a high-quality compounder trading at a discount because the market can’t decide whether to treat the AI buildout as an opportunity or a threat to margins. The Q1 numbers already answered that question: revenue accelerated, margins held up, and entirely new monetization surfaces are opening up. Patient investors who can tolerate capex headlines are being offered a re-rating opportunity here.

I’m not sure about the AI investment for Meta, I believe it’s the wrong strategic bet for the business. But, as we’ve seen in the past, even poor capital allocation decisions (Like the Metaverse, buybacks at aggressive all time highs and so on) the digital advertisement engine of Meta can’t be held down. It is a pristine business, and all marketers I know always go back to spending more on Meta ads as opposed to other digital ad services.

S&P Global SPGI SPGI 0.00%↑ 🏛️

S&P Global finally trading at a reasonable price.

Financial Data, Ratings & Indices

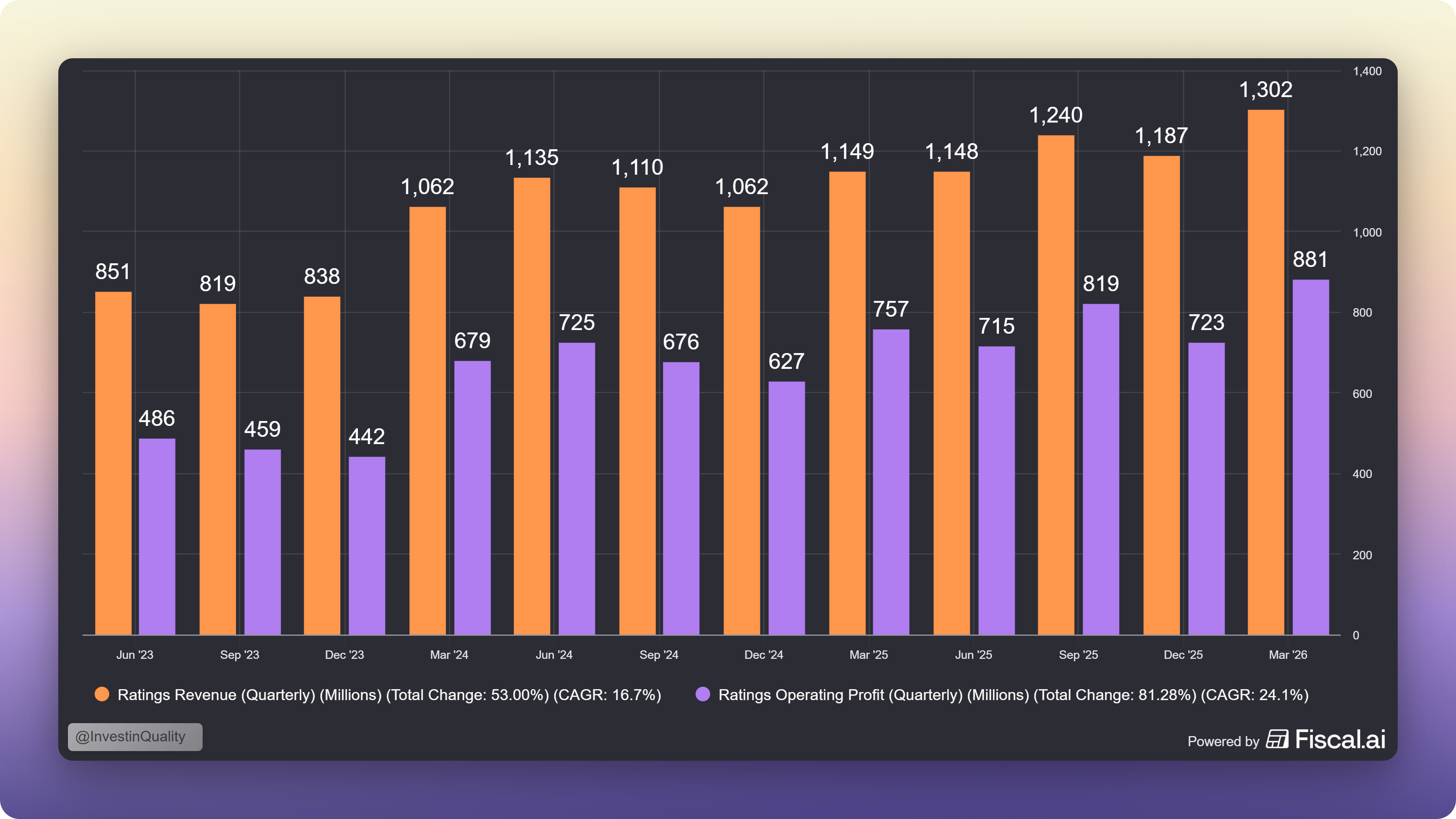

S&P Global just posted a 10.4% revenue increase and a 28% jump in net income, and the stock is trading at one of its lowest valuations in over a decade. If you’ve ever wondered what a wide-moat business mispriced by macro noise looks like, this is a prime example.

The Model: Three Toll Booths

S&P Global sells judgment, data, and benchmarks that the entire financial system relies on to function.

The Ratings division prices the creditworthiness of nearly every major bond issued globally; you cannot easily route around a credit rating that institutional investors require.

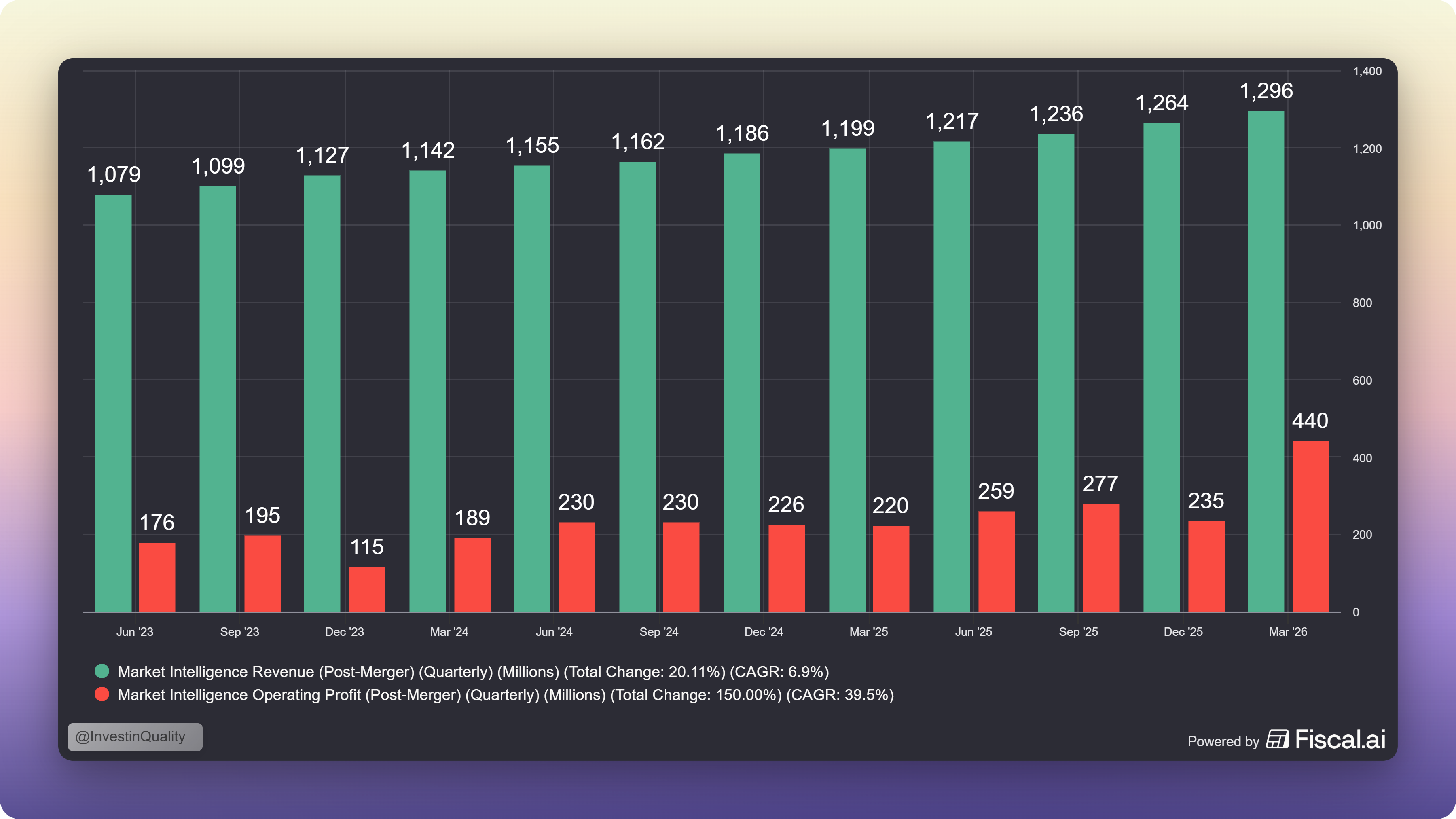

Market Intelligence sells data, analytics, and workflow tools on subscription, recurring revenue that barely notices fluctuations in the market.

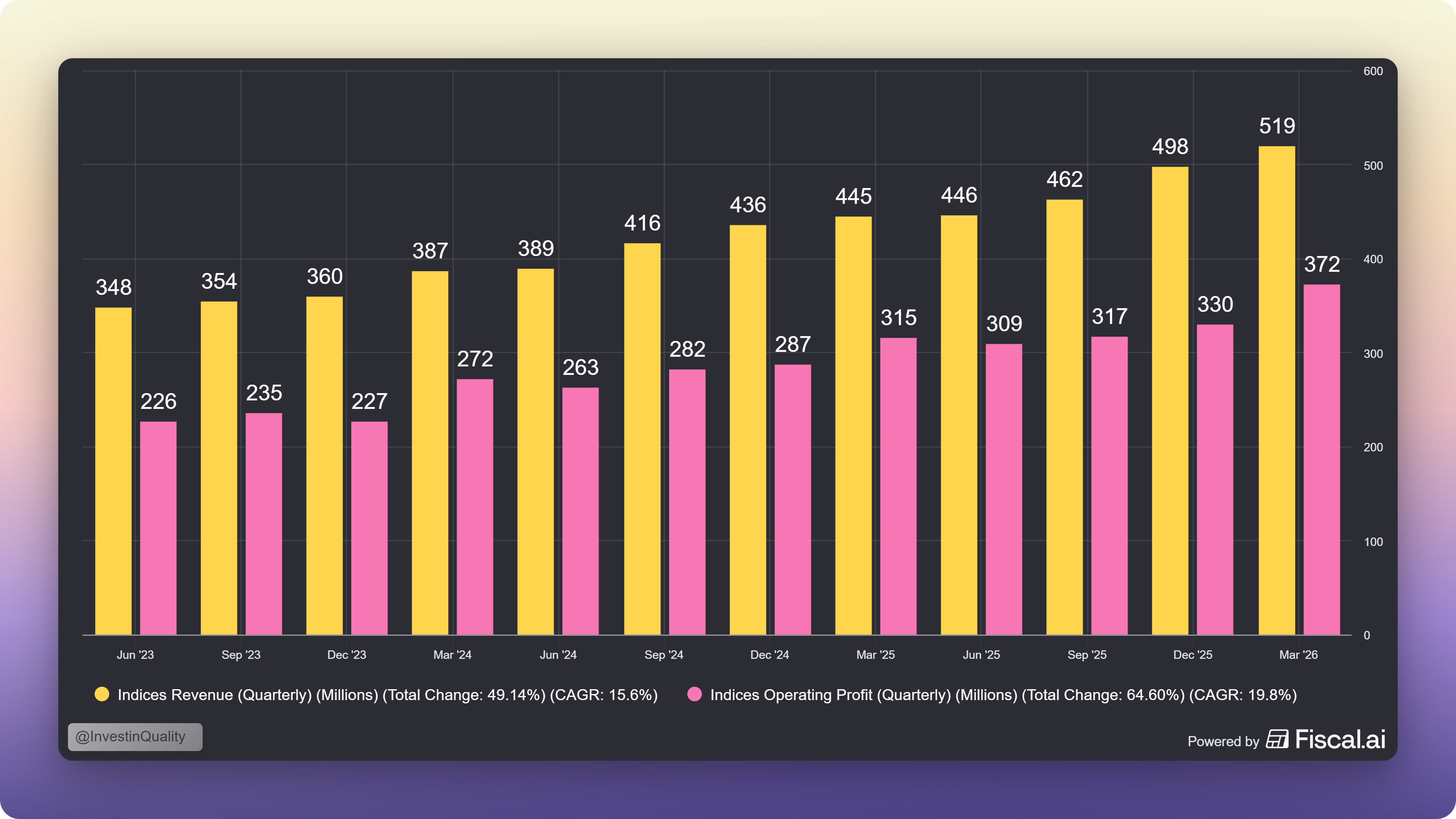

Indices earns asset-linked fees on trillions of dollars sitting in S&P-benchmarked ETFs and mutual funds, growing automatically as markets rise over time.

This is a duopoly business (alongside Moody’s) operating in a market with almost no real substitutes.

Growth Drivers

Bond issuance reacceleration: Billed issuance jumped 28% in the most recent quarter, driving double-digit Ratings revenue growth. Corporate borrowers refinancing into a more stable rate environment is a direct tailwind for SPGI.

Indices growing fastest of all five segments: Indices revenue grew 17% last quarter, the fastest of any division, powered by rising ETF and mutual fund AUM. This segment scales almost for free.

Capital return acceleration: Management now expects to return 100% or more of adjusted free cash flow to shareholders in 2026 through dividends and buybacks, up from prior guidance.

Mobility spin-off: S&P Global is on track to separate its Mobility division in 2026, a move that should sharpen the remaining business’s growth and margin profile and may unlock value the market isn’t currently crediting.

The Numbers

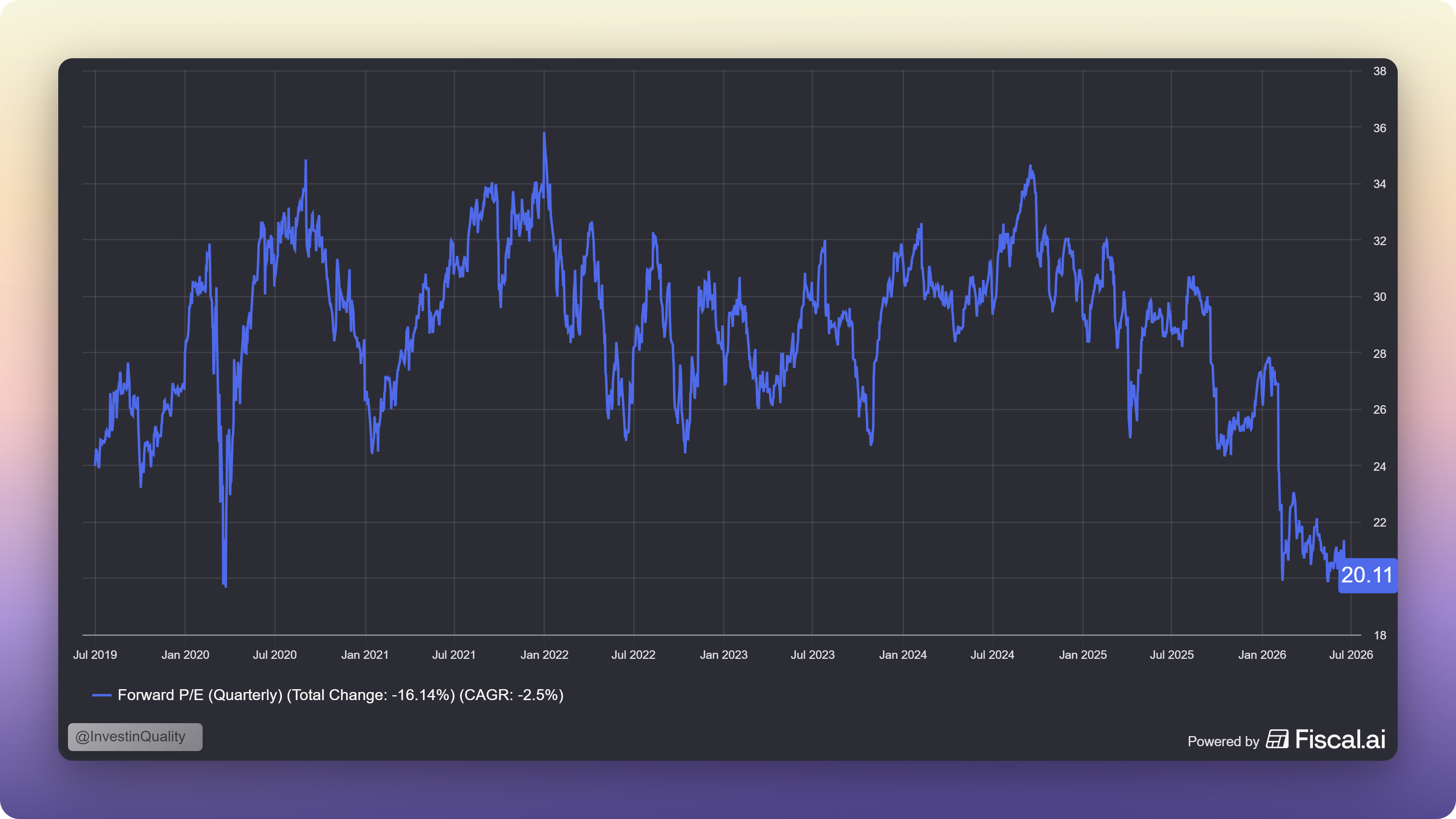

S&P Global trades at a forward P/E of 20.11x, well below its 3-year and 5-year average multiples, which have run closer to 30-35x.

The free cash flow yield is also at its highest level only seen a few brief times over the past decade:

Full-year guidance calls for 6-8% organic revenue growth, with adjusted EPS guided to $19.40-$19.65.

Bottom line

In my opinion, S&P Global isn’t cheap because the business got worse, but because the stock had a difficult year on sector rotation and general financial-sector pressure. Looking at the numbers, the underlying engine kept compounding. A toll-booth business with this kind of pricing power rarely trades at a meaningful discount to its own history. Right now, it does.

SPGI is set to return all free cash flows to investors. This is a double edged sword - on one hand it is great to get a dividend and buyback yield, but I ideally want to invest in businesses that can reinvest the proceeds at a high return.

Despite this, SPGI is a great defensive quality compounder to bring stability to ones portfolio.

The rest of this article, including our next three picks is for Premium subscribers only.