Top 5 Buys April 🏰

Fairly priced quality businesses 🧠

We are building a video course on quality growth investing. 👨🏫

It will teach you:

How to find quality ideas 💡

How to analyze a business 🏰

How to value a business 📊

How to build your portfolio 🧠

Sign up for an early release offer when the course releases:

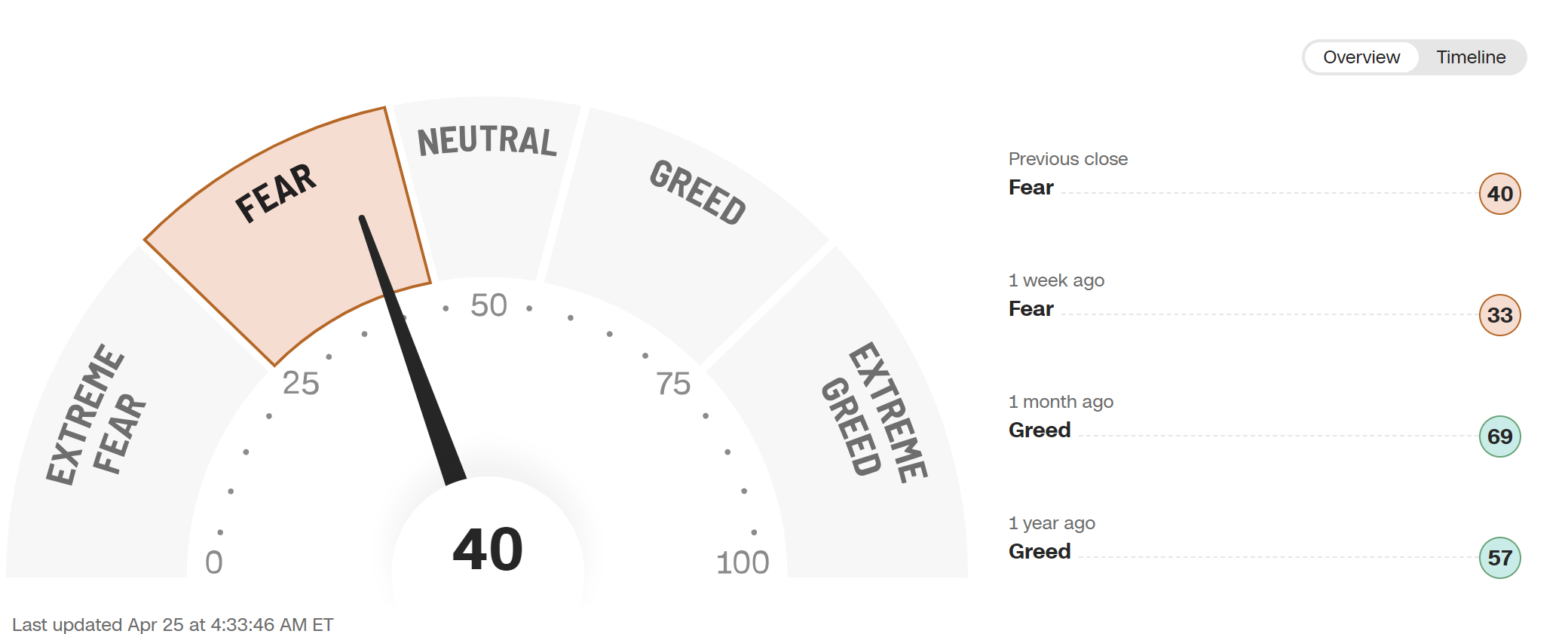

The Greed to Fear index is pointing toward Fear 😱

The market is cooling off after a massive run-up. This is completely normal. What usually happens, is that prices get ahead of the fundamentals and the market needs to pull back a bit, and trade sideways for some time before continuing to increase. After the price starts to fall, the financial media will dictate different narratives that fit - like sticky inflation, war in the Middle East, and so on.

The S&P 500

The S&P 500 is still close to its all-time highs, it has pulled back -3.5% since its top levels. We might see the downtrend continue for a few more months. As a long-term investor, this is what you want. Lower prices for equities, mean that the expected long-term returns are much higher. Purchasing stocks at stretched valuations can be a good way of losing your capital.

Earnings Season

As of this writing, we see some of the large companies sell off after their earnings. Meta Platforms traded as low as -22% in the aftermarkets, while Adyen lost ~12% on its earnings, Evolution -5%, and so on. In my experience, when the market is in a negative narrative spiral, even good earning reports can send a business down after the report. I don’t pay too much attention to one quarter’s earnings. I look for red flags for the long-term prospects of the business.

10 Cheap businesses from the Quality Growth Investable Universe:

What is a good buy?

I have outlined in my book and my valuation cheat sheet how I value businesses. There are several methods one can use, but I like to keep it simple. First I want to understand the business, how it makes money, the different business segments, and the growth potential for each segment or product/service and market. Then I look at historical multiples to get an idea of what the company has traded at, as well as the development of margins and capital efficiencies over time. I then use a discounted cash flow analysis and a reverse DCF analysis to determine what I believe the company will return.

Top 10 Buys 2024

Keep in mind, last week we released a top 10 buys that will be updated monthly for premium subscribers. To not be repetitive, I will not mention any of the 10 buys—The top 10 represent our current best buys as we see it.

Read it here: Top 10 Buys 2024 👑

Check out the top 5 buys for March 2024 here:

Disclaimer: This is not investment advice, always do your own due diligence and make your own investing decisions.

Top 5 Buys April 2024 🏆

Fortinet FTNT 0.00%↑ 👾

Fortinet is a prominent global cybersecurity company. It provides broad, integrated, and automated security solutions designed to secure and simplify IT infrastructure.

Fortinet is best known for its FortiGate firewall, alongside a wide array of products including FortiManager, FortiAnalyzer, and FortiSIEM, catering to enterprises, service providers, and government entities.

Key Fundamentals:

Revenue 5-Year CAGR: 24%

EPS 5-Year CAGR 30.6%

ROCE 5-Year 23.8%

Gross Margin 77%

Operating Margin 23%

Interest coverage 59x

CAGR since inception 28.8%

Valuation

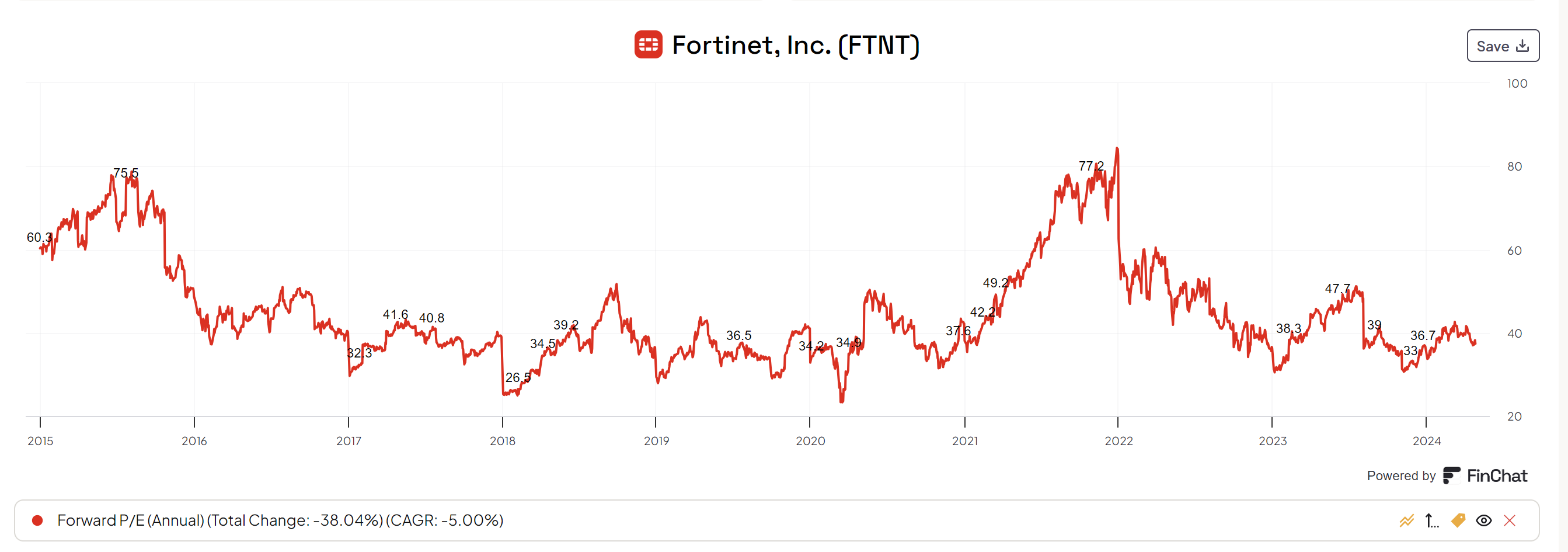

Fortinet is a high-quality business expected to grow its long-term earnings by more than 15% annually. The stock has sold off a few times since 2021 due to growth concerns. We don’t have the same concerns.

Fortinet saw the business boom in 2021 in a post-pandemic market where businesses worldwide were investing heavily in IT infrastructure and digitalization. Cyber security was one of them.

In 2021 revenues grew 28.8% YoY, and in 2022 it grew 32.2% YoY. The deceleration in 2023 was to be expected of “only” 20.1%.

We believe the business is well-positioned to benefit from the secular trend of cyber security. This trend is only getting stronger as criminals utilize new technologies such as AI to make their attacks on corporations & businesses more sophisticated.

Fortinet is currently trading at ~36x NTM earnings. Historically, this is a decent multiple to pay for a high-quality cybersecurity business.

Xpel XPEL 0.00%↑ 🚗

Xpel is a global leader in the manufacture and distribution of protective films and coatings for automotive and architectural applications.

Xpel's flagship products include paint protection films, automotive window films, and ceramic coatings. These products are designed to protect vehicles from scratches, chips, and environmental damage.

The company serves a diverse clientele ranging from individual car owners to professional installers, offering training and certification programs to ensure high standards of application and customer satisfaction.

Key Fundamentals:

Revenue 5-Year CAGR: 29%

EPS 5-Year CAGR 43%

ROCE 5-Year 45%

Gross Margin 41%

Operating Margin 17%

Interest coverage 54x

CAGR since inception 21.2%

Valuation

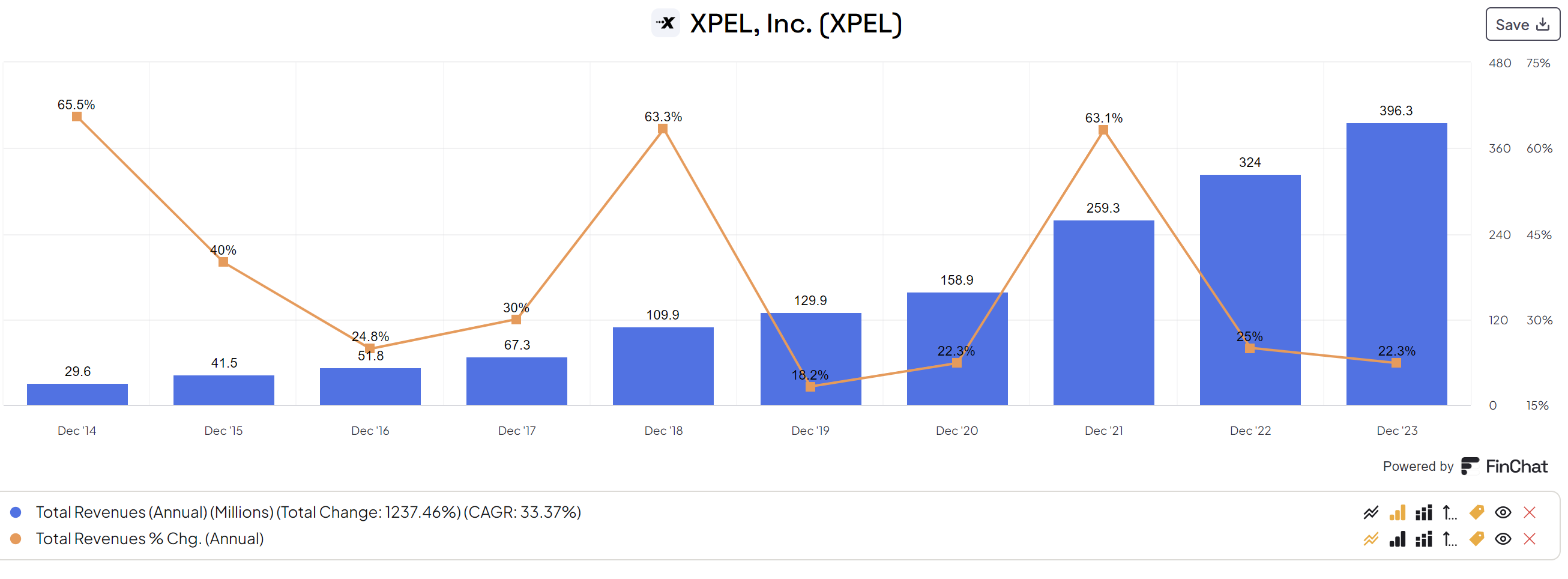

Xpel is a fast-growing small-cap that was a huge winner after the pandemic. The multiples for the business got excessively high at +70x NTM earnings, and the stock has not been able to catch up to its all-time highs after this. Xpel is now trading at 25x NTM earnings. A much more reasonable price for a fast-growing business.

As we can see below, Xpel has only had one year of below 20% annual revenue growth (in 2019 18.2%). The product Xpel is delivering is great, and there is sustained demand for it, even at a larger scale.

The rest of the article is for Premium subscribers, consider going Premium: