Emerging Compounder 💎

Growing revenue +40%, 20x Forward PE, PEG of 1.2x

Sea Limited business breakdown SE 0.00%↑

Sea’s stock is 53.6% below its recent high. The bear case is that TikTok Shop is dismantling Shopee, gaming peaked, and margins are collapsing. The bull case is that three businesses running simultaneously at 40%+ revenue growth, for the first time in company history, suggests something very different is happening.

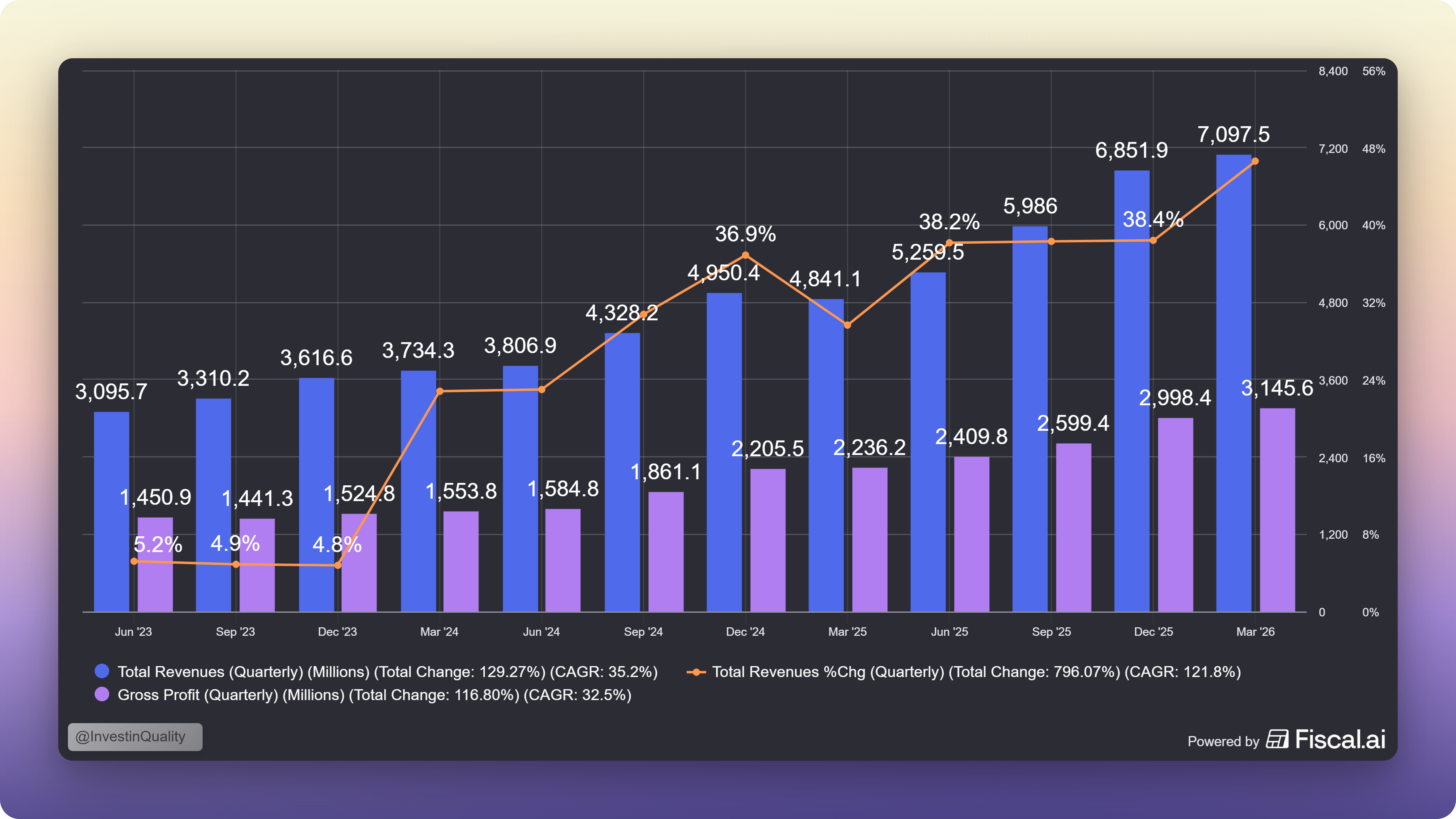

Revenue grew 46.6% in Q1 2026. Net income grew 6.7%. The market is looking at that gap and concluding the business model is broken. I think it’s doing something else entirely, confusing deliberate reinvestment with structural deterioration.

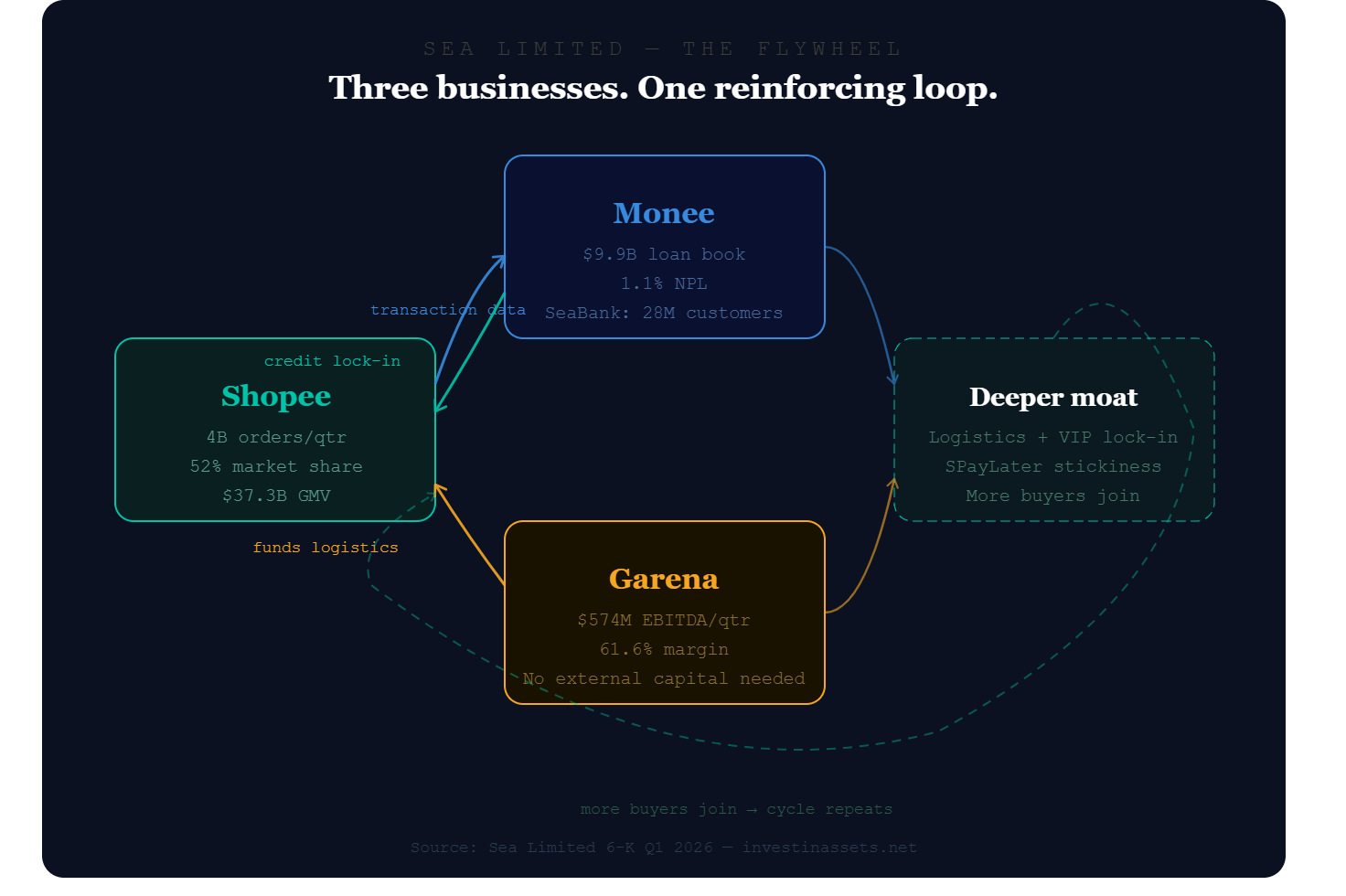

Sea Limited is made up of 3 primary businesses:

Business 1: Shopee

Southeast Asia’s Amazon (+Brazil)

Shopee is the dominant e-commerce marketplace across Southeast Asia and the #2 platform in Brazil. In Q1 2026 it generated $37.3 billion in GMV (up 30.2%), $5.1 billion in revenue (up 45.1%), and processed 4 billion orders. The most important number: revenue is growing faster than GMV. Shopee is taking a larger cut of every transaction, not just doing more transactions.

Shopee Q1 2026 key metrics vs prior year:

How is the take rate rising?

Advertising. Shopee’s ad revenue grew 80% year-over-year in Q1 2026, sellers paying to appear first in search results. This is structurally identical to how Google monetises search: high-margin, defensible, and nearly pure profit at the margin.

The VIP program is the detail most analysts skip. Launched in Indonesia in early 2025, it now has 3.5 million subscribers across Indonesia, Thailand, and Vietnam. Those members are 2.5% of all buyers but generate roughly 20% of all GMV. In Indonesia, VIP members spend 40% more after subscribing than they did before. That is not a loyalty program. That is a flywheel lock-in.

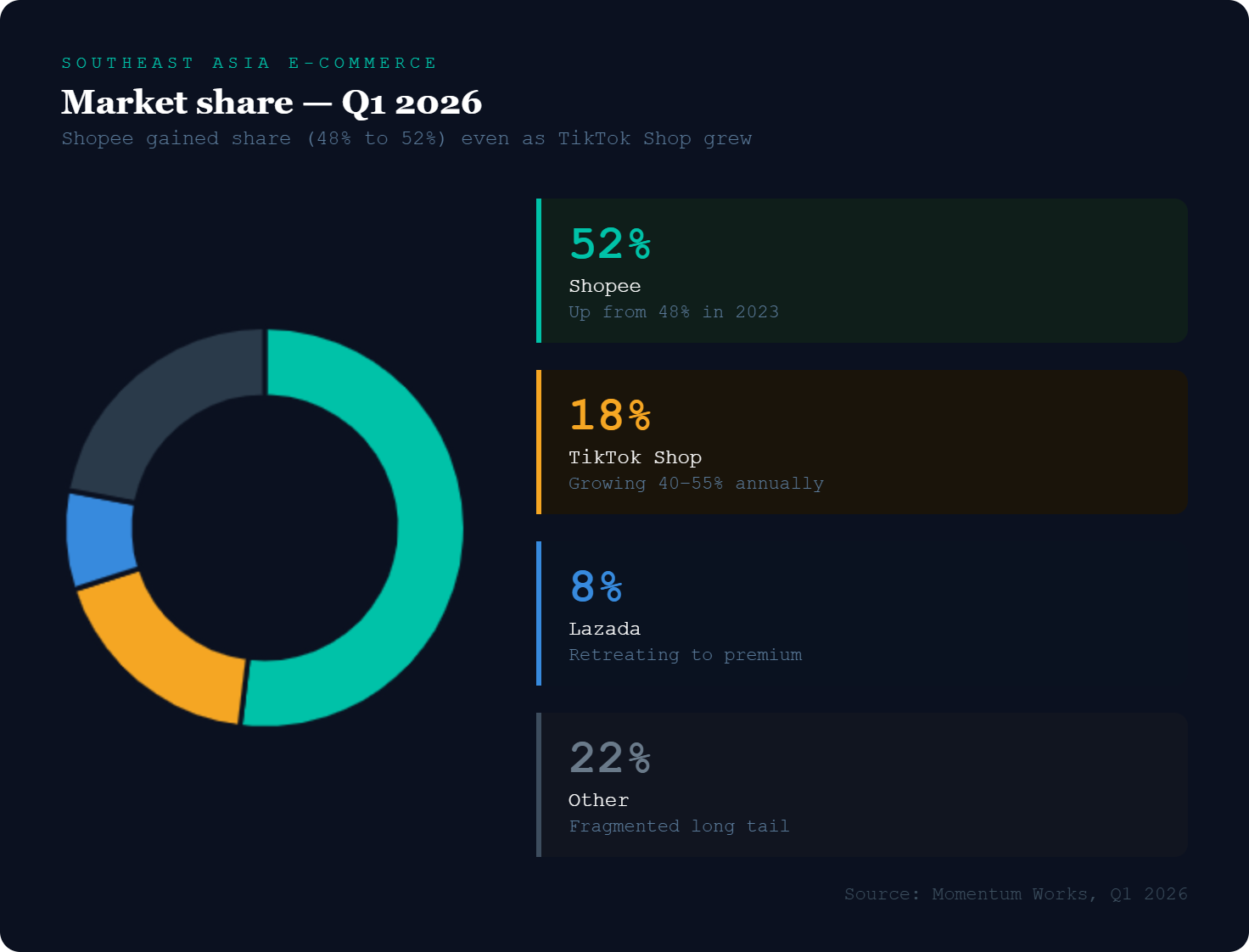

The TikTok Threat

Southeast Asia e-commerce market share Q1 2026:

TikTok Shop is a real competitor. It holds 18% of Southeast Asian e-commerce GMV, is growing at 40–55% annually, and its Tokopedia partnership gives it serious infrastructure in Indonesia, the region’s largest market. By 2027–2028, it could reach 25%+. This is a real threat for SE.

What TikTok Shop wins: impulse purchases, fashion, beauty, discovery-driven, low-ticket categories. What Shopee dominates: electronics, home goods, FMCG. These are categories where customers care about delivery guarantees, returns, and warranties. These are meaningfully different shopping occasions.

The scenario that should concern investors is not TikTok Shop at 18%, but TikTok Shop at 28% with a fintech stack that competes with SPayLater. That is the product Shopee’s moat actually depends on preventing.

Lazada, Alibaba’s bet on Southeast Asia, has essentially conceded. After spending over $7.4 billion, it has repositioned as a premium brand platform. One less serious competitor for mass-market GMV.

Business 2: Garena

The cash engine nobody models correctly

Garena operates Free Fire, one of the most downloaded mobile games in history, plus licensed titles including EA Sports FC and Call of Duty: Mobile. It exists inside a company known for e-commerce and fintech, which means most analysts look at it wrong.

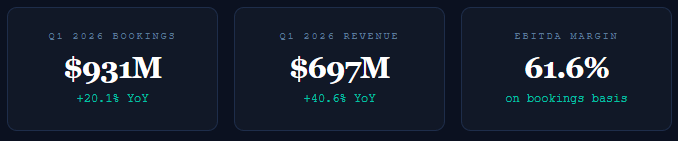

A 61.6% EBITDA margin. On $931 million in quarterly bookings. Garena generated over $500 million in operating profit in a single quarter, and that cash is flowing directly into Shopee’s logistics build-out and Monee’s loan book. This is the engine that makes Sea’s reinvestment cycle possible without raising external capital or diluting shareholders.

The user base has been roughly flat for two years (620–670 million quarterly). What’s changing is how those users spend. The paying user ratio has climbed from 8% to 10.9%. Average spend per paying user has risen from $0.83 to $1.40. This is a fundamentally healthier growth trajectory than buying cheap installs.

However, the concentration risk is real. If Free Fire faded sharply, it would hurt badly. The evidence so far points toward an evergreen franchise, IP collaborations with Jujutsu Kaisen, Naruto, and Squid Game have kept the game current, and Arena of Valor just hit record quarterly bookings in its tenth year of operation. But this risk is on the table.

Business 3: Monee

The fintech stack that makes Shopee defensible

Formerly SeaMoney, Monee is Sea’s financial services arm. It lends to Shopee shoppers via SPayLater and to small businesses on the platform, and operates digital banks: SeaBank in Indonesia, Philippines, and Brazil, plus MariBank in Singapore.

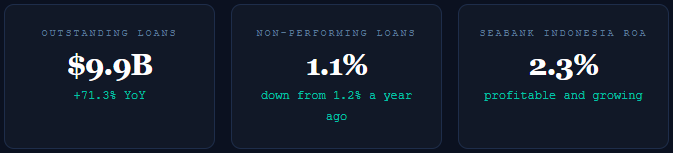

Growing a loan book at 71% annually while improving credit quality is not something you see often. The NPL of 1.1% declining year-on-year tells you the underwriting model works at scale.

The competitive advantage for Monee is data. Every Shopee purchase, every payment, every return generates a transaction trail. Monee uses that to assess creditworthiness with far more precision than a bank that only sees salary and credit score. A regional bank cannot replicate this without first building a marketplace with hundreds of millions of buyers. A fintech startup cannot replicate it either, they don’t have the data.

SeaBank Indonesia ended 2025 with 28 million customers. It is the only Indonesian digital bank generating returns on assets comparable to conventional retail banks. Most digital banks are still burning cash acquiring customers.

Brazil is the next major growth vector. Monee obtained a new financial licence in Brazil in Q1 2026. The Brazilian loan book crossed $1 billion, up 250% year-over-year. SPayLater penetration in Brazil is roughly 10% of GMV versus significantly higher in mature Southeast Asian markets.

Monee is not just a fintech business. It is the moat that makes Shopee harder to leave. The moment a customer starts using SPayLater, switching to TikTok Shop means giving up their credit line. That is a strong lock-in.

The Flywheel

Each business makes the others stronger. Shopee generates buyers and transaction data. Monee uses that data to lend profitably, and its credit products, SPayLater, digital banking, make Shopee harder to leave. Garena generates cash that funds Shopee’s logistics build and Monee’s loan book growth. No external capital required, resulting in no dilution.

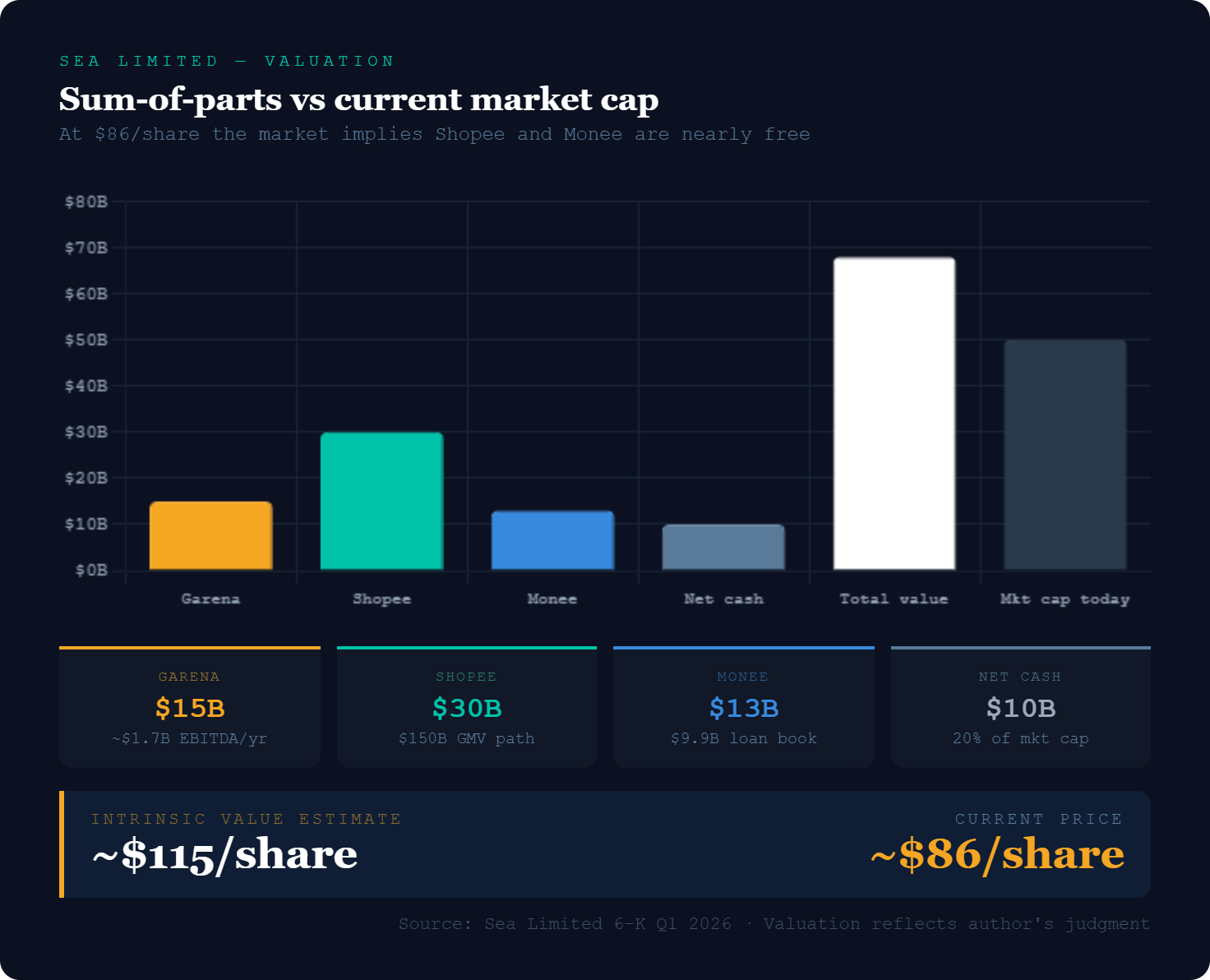

What Is Sea Worth?

Sum-of-the-parts

Sea’s balance sheet holds $11.1 billion in cash and investments against less than $800 million in debt, roughly $10.3 billion in net cash, nearly 20% of the entire market cap. In November 2025, the company announced its first-ever $1 billion share buyback, a signal that management believes the stock is undervalued.

Sum-of-parts valuation bridge vs current market cap.

At $86/share, the market implies Shopee and Monee are almost free. That is the opportunity, or the warning sign, depending on your view of TikTok Shop.

I love to look at the sum of all parts, but we almost never see a business being fully valued from this perspective, there is always a ‘conglomorate discount’. Look at Mercadolibre and Amazon as an example.

Despite this, Sea Limited is in a strong position in a very interesting market. If SE can continue to prove its profitability while keeping their Shopee market share, the result for investors can be lucrative.

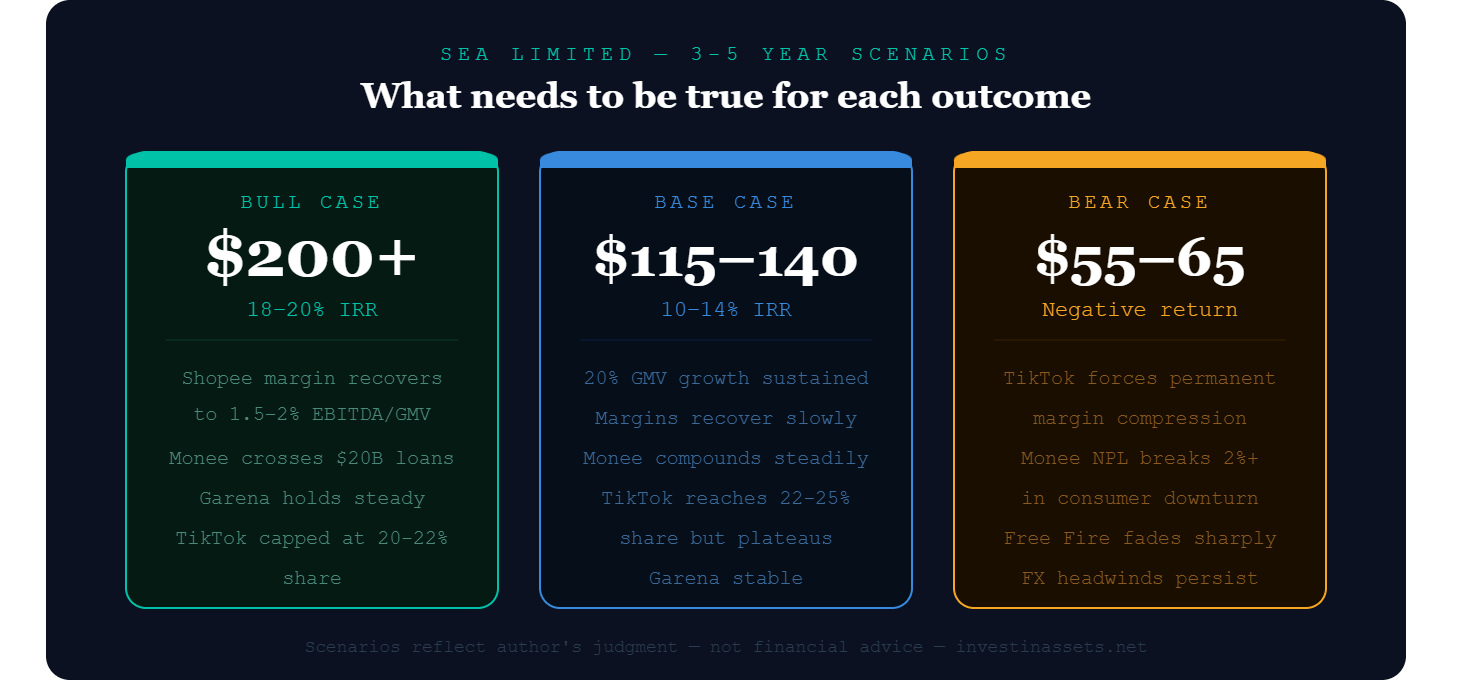

Here is what needs to be true for our bear, base, and bull case to play out:

The Risks You Need to Own

Shopee margin compression

Management guided Shopee’s profit margin at ~0.6% of GMV for all of 2026, versus a long-term target of 2–3%. This is deliberate investment, but patience is required. The re-rating catalyst is the first quarter where this metric inflects upward year-over-year.

Garena concentration

Free Fire is extraordinary. It is also a single game. A better replacement could erode it faster than IP collaborations can offset. The franchise looks evergreen, but that assessment has to be revisited every quarter.

Untested credit cycle

Monee’s 1.1% NPL looks pristine today. The loan book has only existed at scale during a period of relative economic stability. A sharp consumer downturn in Southeast Asia or Brazil is the real test, and that test has not yet arrived.

Governance concentration

Forrest Li holds ~59% of voting rights. Minority shareholders have limited ability to influence governance. You are backing the founder, and the founder alone. That is a feature for some investors and a dealbreaker for others.

Currency risk is also real and underappreciated. Sea earns in Indonesian Rupiah, Brazilian Reals, Thai Baht, and Vietnamese Dong, and reports in USD. FX moves add volatility that has nothing to do with operational performance and can distort quarter-to-quarter comparisons significantly.

Concluding Thoughts

Sea is a company where three distinct businesses compound each other, all running at 40%+ revenue growth simultaneously, on a balance sheet with $10+ billion in net cash, at a valuation that implies the flywheel stops spinning.

The market’s central fear, that TikTok Shop structurally impairs Shopee’s profitability, is a legitimate risk, not a dismissible one. TikTok Shop at 25%+ with a fintech layer would be a materially different competitive environment. What the market is getting wrong in my opinion is treating that as the current reality rather than a tail risk to monitor.

The single metric to watch: Shopee EBITDA as a percentage of GMV. The moment that starts inflecting upward year-over-year, the re-rating begins. Until then, you are being paid in growth while you wait, in a business where the underlying flywheel is turning faster than the stock price reflects.

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Disclaimer:

This newsletter is for informational purposes only and does not constitute financial, investment, or other professional advice. The views expressed are solely the author’s opinions and may change without notice.

Investing in securities involves risk, including the potential loss of capital. Past performance is not indicative of future results.

The author may hold positions in securities mentioned. Readers should do their own research and consult a licensed financial advisor before making investment decisions.

A lot of investors screen for low P/E.

Far fewer screen for the combination of growth, valuation, and capital allocation.

The interesting question isn't whether Sea is cheap.

It's whether the market is still underestimating the durability of the ecosystem.