Terry Smith on Quality Investing 💎

The importance of patience, the man in the arena, and the insanity of the current market

Hi there, investor!

In this article, we’ll discuss a recent interview with Terry Smith, the legendary investor behind Fundsmith.

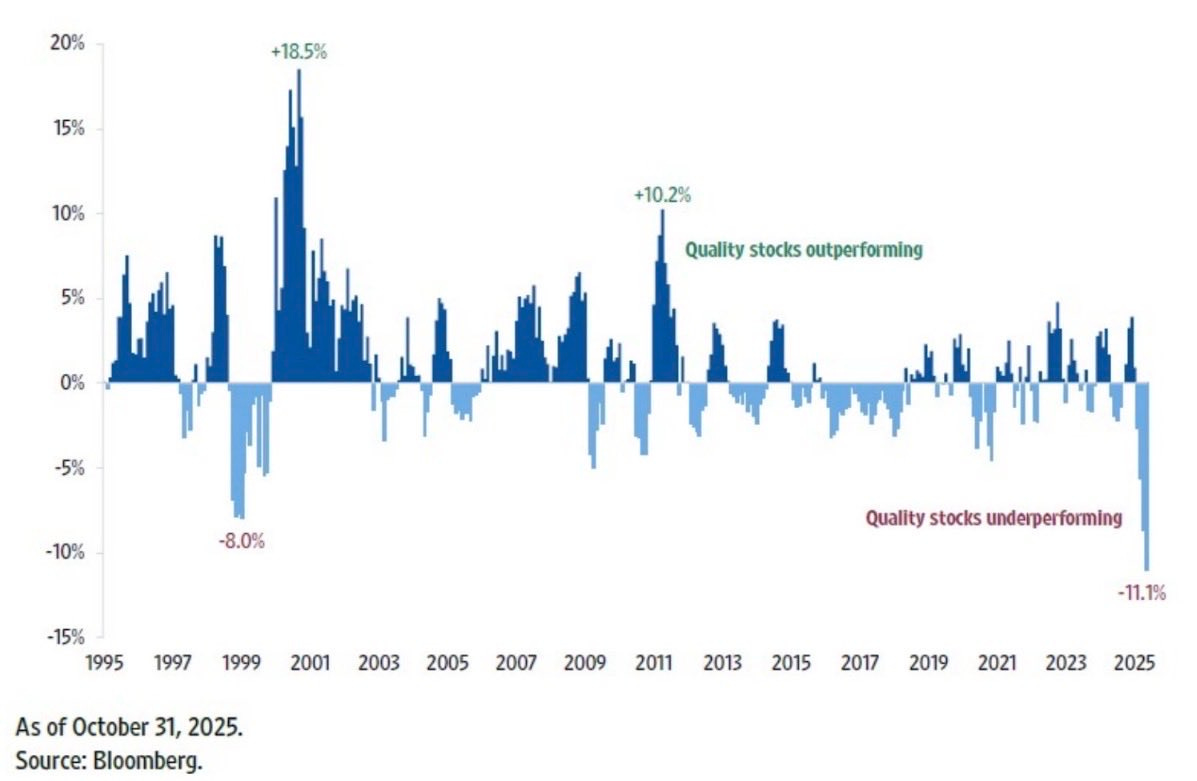

Smith has beaten the index for decades, but he has faced headwinds in recent years, as Quality investing is experiencing its worst period since the dot-com bubble.

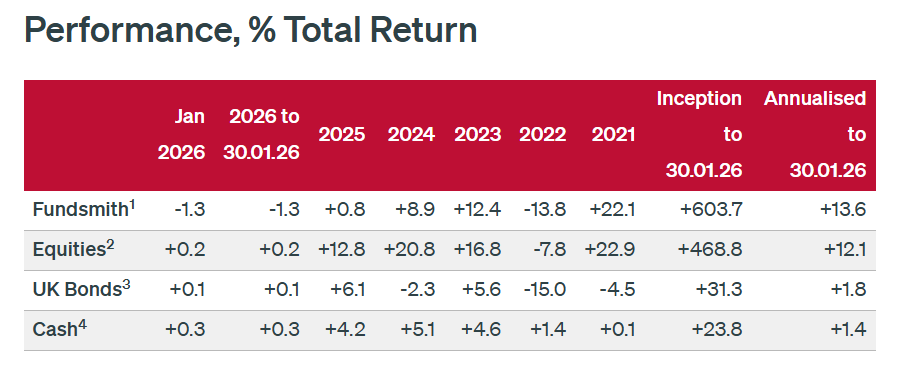

Fundsmith has delivered an annual return of 13.6% since its inception in 2010, compared to 12.1% for the MSCI World Index.

However, the fund has underperformed the index for several years now. In the interview, Smith emphasizes the importance of patience and long-term thinking.

If you’d like to watch the full interview, you can find it here:

Let’s go through the key points 👇

FCF Yield + Growth = Long-Term Compounding

Smith argues that one of the simplest ways to estimate a company’s future shareholder return is to take its free cash flow yield and add the expected growth rate.

For example, Visa has an FCF yield of around 4% and an estimated future EPS growth rate of 12.9%. Based on Smith’s framework, this would imply a potential long-term return of approximately 16.9%.

Smith doesn’t elaborate in detail on why he prefers free cash flow, but other investors often use earnings yield (the inverse of the P/E ratio) plus dividend yield and growth estimates. That approach can also work.

However, Smith always follows the cash.

He focuses on a company’s ability to convert accounting earnings into real cash, and he is mindful of the accounting techniques that can distort reported earnings.

Free cash flow is harder to manipulate. It is calculated as cash flow from operations (CFFO) minus capital expenditures (CapEx). The logic is simple: operating cash flow reflects the true cash generation of the business, while CapEx represents the capital required to sustain operations.

In many cases, CapEx can be divided into maintenance and growth investments. Some investors attempt to adjust for this by excluding “growth CapEx,” but Smith prefers to keep the calculation straightforward. Growth investments are typically already reflected in the company’s expected growth rate.

FCF yield plus expected future growth provides a practical and effective way to think about long-term returns.

The Man in the Arena

Terry Smith is clearly inspired by Theodore Roosevelt’s famous “Man in the Arena” speech.

He often references it when discussing his success.

Smith speaks about courage — about making decisions that may expose you to ridicule or public criticism. For example, Smith recently thought about buying a bank stock after being opposed to banks for decades.

He refuses to let fear of embarrassment prevent him from making what he believes is the right decision.

Like Roosevelt’s “man in the arena,” he would rather risk failure than stand among the timid souls who experience neither victory nor defeat.

The Insanity of the Current Market

Smith describes today’s market environment as unusual.

He argues that AI expectations are currently carrying the market. Strip away AI-related spending, and the broader economic picture looks far less impressive.

This concerns him. No one truly knows what AI will deliver in terms of profits and cash flows over the next five years. When the hype fades, will sustainable business models justify the enormous investments being made?

Smith does not give a definitive answer, but reading between the lines, he appears skeptical.

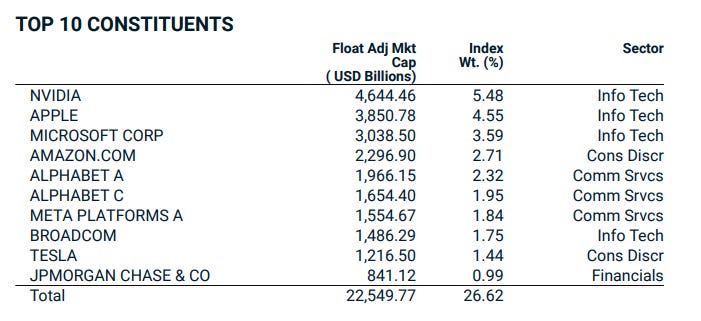

He also highlights a major structural shift over the past decade: the rise of index investing.

Today, if an investor allocates $100 to an S&P 500 fund, approximately $7–8 flows to Nvidia, and $4–6 goes to many of the other Magnificent Seven companies.

Smith argues that this creates a supply-demand distortion:

Stocks rise → index weight increases → more passive inflows → prices rise further → weights increase again.

This feedback loop reinforces momentum.

Almost every major index fund has significant exposure to these same large companies. In that sense, index investing can amplify concentration risk. Even the MSCI world index, which is supposed to be globally diversified, is highly concentrated in the top 10 US stocks:

According to Smith, the top 10 stocks have driven roughly two-thirds of recent market gains. This explains why buying the index has worked so well — it is heavily concentrated in these mega-cap leaders.

Smith does not claim to know when this dynamic will reverse. However, he notes that we have not experienced a true recession since Iraq invaded Kuwait in the early 1990s, and that the only major firm to collapse in 2008 was Lehman Brothers.

He believes we may be due for a significant correction, though he admits he has no insight into when that might occur.

Why Smith Believes His Portfolio Will Perform Well

Smith argues that his portfolio consists of companies with:

Predictable future cash flows (driven by moats and organic growth)

Returns on capital of approximately 30%

Strong conversion of earnings into free cash flow

He believes that owning businesses with these characteristics will ultimately produce strong results.

However, patience is essential — particularly during periods dominated by powerful market narratives.

Smith echoes a principle associated with Charlie Munger: over long time horizons, shareholder returns tend to approximate the company’s return on capital.

Charlie argues that it is hard for a business with a return on capital of 6% to earn any more than 6% for shareholders over the long term. Here is the full quote from Charlie:

Concluding Reflections

It is striking how quickly perception shifts.

Terry Smith has gone from being celebrated as a superstar investor to being dismissed by some as outdated — all within a few years.

Markets have short memories. Long-term track records are easily forgotten when recent performance disappoints.

Fundsmith has not abandoned its philosophy. It has adapted where necessary but remains committed to its core principles.

Meanwhile, many investors have shifted toward the Magnificent Seven — and that strategy has worked extremely well. So the temptation is understandable.

Still, there are risks in today’s index-driven market. When valuations are stretched, and optimism fuels unprecedented capital investment, it may be wise to step back and reassess.

Buffett faced similar criticism during the dot-com era.

The worst strategy an investor can adopt is constantly changing approaches to match current market leadership. Every year brings new narratives, sectors, and technologies.

The disciplined investor builds a portfolio of high-quality businesses they genuinely want to own — and remains patient enough to let compounding work.

It has been a challenging period for many quality-focused investors.

But disciplined investing, with a strong emphasis on risk-adjusted returns, will never go out of style.

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Thanks for sharing.