💎 Quality at a Reasonable Premium

Build a Winning Quality Growth Portfolio

When to Pay Up for Great Assets (And When You Absolutely Shouldn’t)

If you’ve spent any time studying quality investing, you’ve likely heard Buffett’s timeless line:

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

But that quote leads to a natural (and often difficult) question:

How much is too much to pay for a great business or asset?

In this piece, I’ll walk through a framework I use to decide:

When to pay a premium for quality

When to walk away

And how to think about valuation in a world of compounding, durability, and opportunity cost

🧠 The Temptation & Trap of Investing

❌ The Temptation:

You find an exceptional company — amazing margins, durable moat, excellent capital allocation — but it’s trading at 35–50x earnings, or a 2.5% yield on cost, or a very tight cap rate if it’s a private asset.

You think: “It’s so good — it’s worth the premium.”

⚠️ The Trap:

If your starting valuation is too high, it becomes a headwind that:

Eats into future returns

Leaves no room for error

Turns even a great business into a mediocre investment

Just take a look at Microsoft (Great business, too high starting valuation):

So where’s the line?

Let’s build the framework.

🔍 1. Separate Price From Payback Period

I don’t just look at a P/E multiple or yield. I ask:

How long will it take me to earn my money back in free cash flow, dividends, or capital appreciation — and what assumptions am I making to get there?

Let’s say:

You buy a business at 40x earnings

Earnings are growing at 20% per year

It reinvests well and expands margins

In that case, your payback period shrinks fast — because growth and reinvestment are working in your favor.

But if:

You buy at 40x

Growth slows to 10%

Margins compress

Capital allocation falters

Now you’ve locked in mediocre returns at a high price — with no margin of safety.

🧰 2. My 3-Part Filter: When Paying a Premium Is Worth It

Here’s what I look for before I pay a premium valuation (public or private):

✅ 1. Durable Competitive Advantage

The business should have a moat I understand — brand, regulatory edge, distribution lock-in, or extreme cost leadership.

Example:

Novo Nordisk has a massive head start in GLP-1, along with regulatory credibility.

✅ 2. High and Consistent Return on Capital

ROC should be 15%+ and stable or rising, ideally with:

Low reinvestment friction

Proven capital allocation history

No need for massive dilution or leverage to grow

Example:

Kinsale Capital consistently earns 20–30% ROE, self-funds growth, and stays disciplined. Worth a premium.

✅ 3. Optionality or Pricing Power

I want businesses that either:

Can launch new products off their core platform

Or raise prices without customer churn

This creates hidden growth that traditional valuation misses.

Example:

Constellation Software reinvests into tuck-ins at 20–30% IRRs. You’re not just buying the core business — you’re buying a reinvestment machine.

🧮 3. What I Don’t Pay Premiums For

Just because a business is "good" doesn't mean it’s priced for success.

Here are red flags for me:

🚫 Crowded Trades With No Edge

If everyone’s buying it for the same reason, and the valuation assumes perfection, I pass.

Think: Consumer tech darlings with 60x multiples and no pricing power.

🚫 Decelerating Growth + Premium Multiple

If revenue and earnings are slowing, but the multiple is still priced for acceleration — that’s a recipe for underperformance.

Think: Aging SaaS businesses with 5–8% growth but still trading at 30–35x.

🚫 Unproven Management or Weak Capital Allocation

Even great products can’t overcome poor reinvestment discipline.

If the CEO is buying back stock at the top or overpaying for acquisitions, I won’t pay a premium — no matter how sexy the margins look.

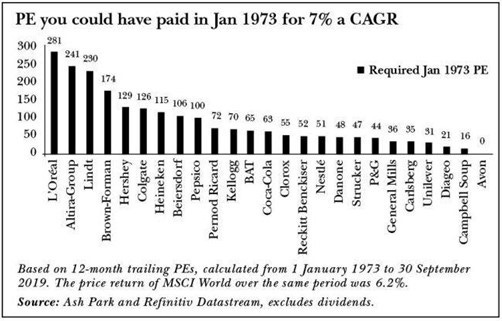

💸 4. When the Premium Becomes a Discount Over Time

Here’s the magic of quality compounding:

When you pay a fair premium for a truly elite business, time turns that premium into a discount.

Let’s say you bought:

LVMH at 25x earnings in 2015

Or Costco at 30x earnings in 2010

Or Blackstone at 5% yield in 2018

If those businesses continue to grow earnings at 12–20% for 10 years, you’ve made a massive gain — and your yield on cost looks incredible.

Over time, valuation matters less — as long as the business performs.

The hard part is separating the true elites from the rest:

📊 5. My Rule of Thumb: The 3% Rule

Here’s a simple rule I use:

Only pay a premium if you believe the business will grow intrinsic value by at least 3% more per year than your next-best option.

That’s your opportunity cost buffer.

If Kinsale is growing intrinsic value at 18%/year, and another stock or private deal is compounding at 12–13% — I’m fine paying up for Kinsale.

But if the gap is tighter than 3%?

I’ll wait for the price to come back to me.

🧭 Final Thought

Quality at a reasonable premium is the cornerstone of successful investing — but it only works when paired with:

A deep understanding of the business

High standards for capital discipline

Patience to let compounding do the heavy lifting

Valuation still matters — but in the long run, business quality dominates.

You don’t need to overpay.

You just need to know when a premium is actually a discount in disguise.

Here is a free “Valuation Sanity Check” template on Google Sheets for you:

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 15,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Great post!!!

I think, however, that we all look for the same things with the same criteria a little bit now. It is normal that then the ratings remain too high for too many years. There is an excess of narrative

This is great, any chance you would be ok with me sharing this article alone to family to see if they would like to subscribe?