FICO: Moat Deterioration or the Buying Opportunity of the Decade? 📈

The stock is down 48% from its all-time highs. The bear case is loud. Here’s what you need to know. 💎

Hi there investor 👋

Today we’re breaking down one of the most controversial quality compounders in the market right now.

FICO (Fair Isaac Corporation) is a company most people interact with every time they apply for a mortgage, a car loan, or a credit card. The three-digit number that determines whether you get approved, at what rate, is almost certainly a FICO score.

The company has averaged more than 30% annual returns since 2008, trouncing the Nasdaq 100. It runs one of the most capital-light, high-margin business models in American finance.

And right now, the stock is down 42% from its 2024 peak.

The bear case: regulators broke the monopoly and a $1 competitor is coming for its most lucrative product.

Here’s the full breakdown. Let’s figure out who’s right. 👇

How FICO Makes Money

FICO is best understood as a toll booth on the American credit system.

Every time a bank, mortgage company, or auto dealer pulls a credit score to make a lending decision, there is a very high probability they are paying FICO a royalty. FICO invented credit scoring in 1989. The score became the industry standard because it works. It has been validated against hundreds of millions of loans over 35 years. And 90% of top US lenders still use it today.

The business has two parts:

Scores (about 55% of revenue)

FICO licenses its algorithm to the three credit bureaus (Equifax, Experian, TransUnion), who pass it on to lenders. FICO charges a royalty per score. The Scores business runs an operating margin of roughly 89%. Almost every dollar of price increase falls straight to the bottom line.

Software (about 45% of revenue).

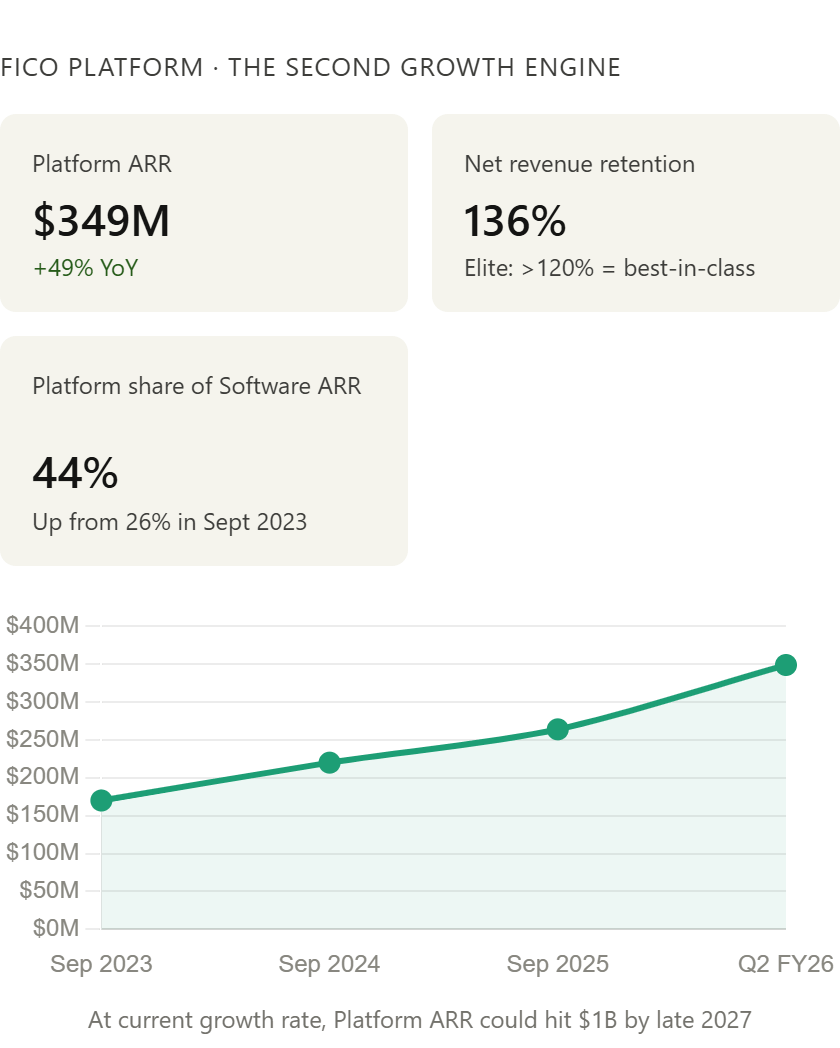

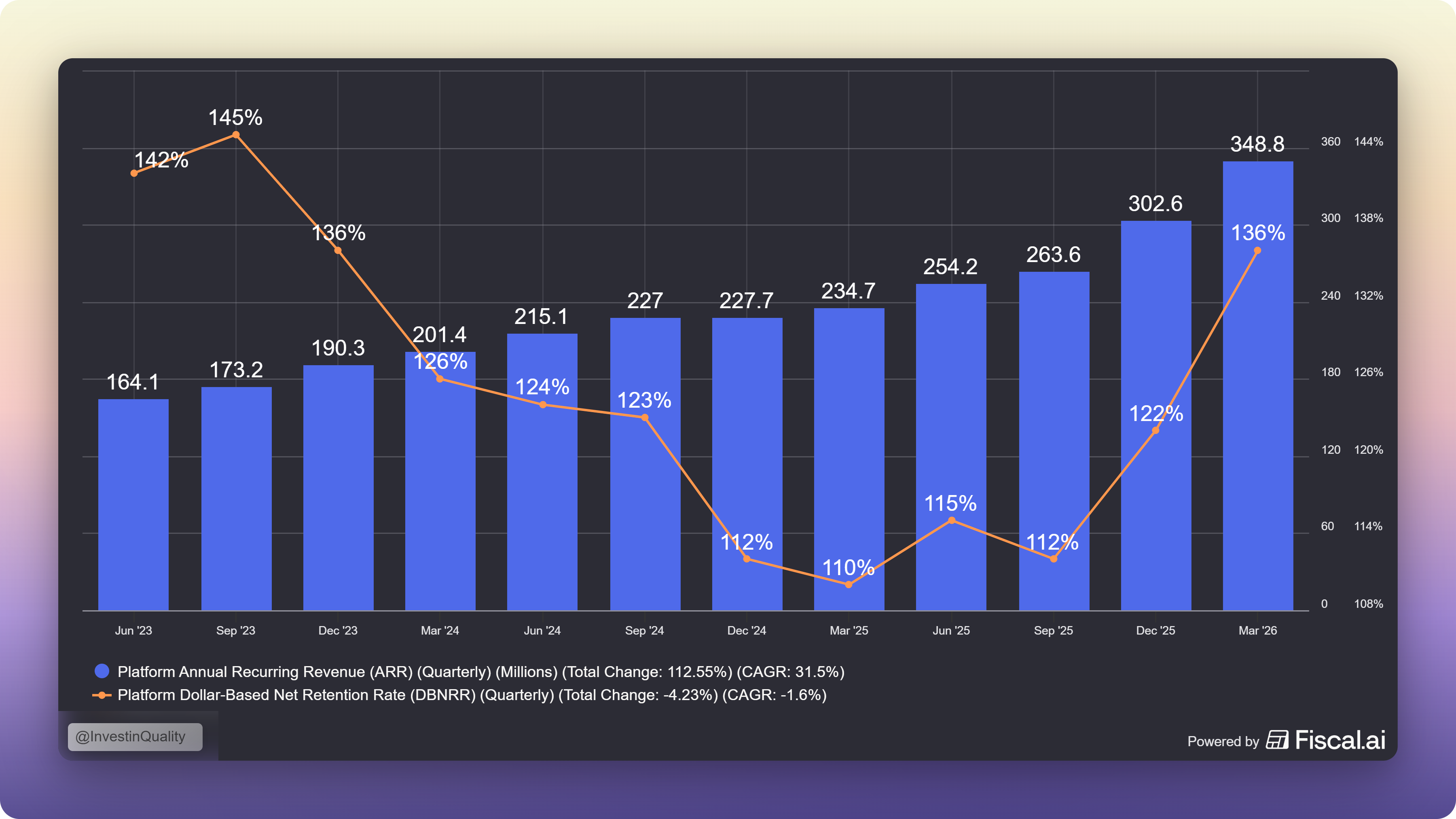

The FICO Platform is an AI-powered cloud system used by banks, insurers, and telecoms to automate lending decisions, fraud detection, and collections. Platform ARR is growing fast and is the company’s reinvestment engine.

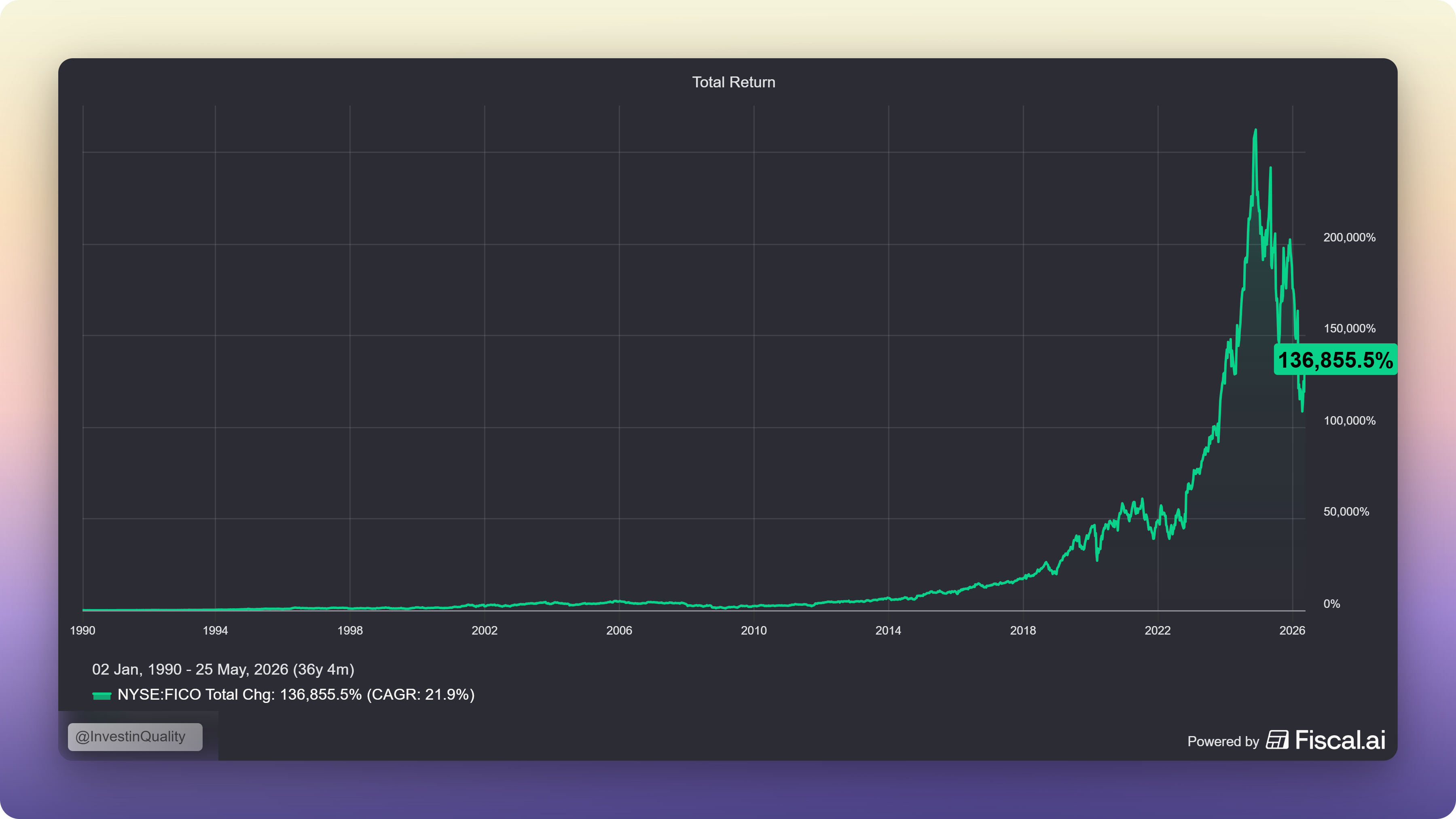

FICO has compounded by 21.9% annually since its inception in 1990, despite its recent -48% sell off:

The Moat: Toll Booth

The core of the FICO moat is what investors call standard-setting lock-in. When a product becomes so embedded in an industry’s processes, regulations, and infrastructure that switching becomes expensive, even when a cheaper alternative exists.

Layer 1: Woven into regulation

The FICO Score is not just widely used. It is built into federal lending guidelines, Fair Housing Act compliance frameworks, and the investor documentation behind the $10+ trillion US mortgage-backed securities market.

When a fund manager in Tokyo buys a US mortgage security, credit quality is expressed in FICO scores. When a bank’s compliance officer certifies lending standards, FICO is the measuring rod. Replacing it requires re-underwriting historical loan performance, retraining models, renegotiating investor documentation, and convincing regulators. None of this happens quickly.

Layer 2: 70 years of proprietary data

FICO has been in credit analytics since the 1950s. Its models have been trained and refined against more loan outcomes than any competitor can replicate. An independent study published in 2025 found FICO Score 10T is the most predictive score for first-time homebuyer mortgages. In finance, that edge matters. A slight improvement in default prediction saves large lenders hundreds of millions per year.

Layer 3: Extraordinary Pricing power

This is the clearest proof that the moat is real. FICO has raised its mortgage royalty repeatedly and aggressively, with lenders complaining the entire time. And yet the price keeps going up.

Why can FICO keep raising prices? Because the math is simple. On a $400,000 mortgage, a $15 credit fee is not the variable that drives the decision. As FICO’s own EVP put it: their royalty represents approximately two-tenths of one percent of total mortgage closing costs.

The lobbyists complain, but lenders pay.

The Risk You Cannot Ignore

Here is the real bear case, and it deserves a serious hearing.

On July 8, 2025, the FHFA officially allowed mortgage lenders to use VantageScore 4.0 alongside Classic FICO when originating loans for Fannie Mae and Freddie Mac. FICO stock fell nearly 19% in a single session. In March 2026, another 9% drop followed as the credit bureaus (who own VantageScore) began offering it at $1 per score versus FICO’s $4.95.

VantageScore is a joint venture of Equifax, Experian, and TransUnion. The same bureaus that distribute FICO scores own a direct competitor. Their economic incentive to steer lenders toward VantageScore is obvious.

This is a legitimate, structural risk. Not a temporary headwind.

What makes it more complicated:

The FHFA mandate allows VantageScore, but it does not require it. Re-tooling mortgage underwriting systems, retraining credit analysts, and updating compliance frameworks takes years. CEO Will Lansing has faced this question publicly for 15 years:

“We compete with VantageScore every day. We always win.”

The numbers still back him up. B2B Scores revenue grew 42% in Q3 FY2025 even after the VantageScore announcement.

The concern is trajectory, not today’s share. The bureaus pricing VantageScore at $1 is predatory. If lenders start accepting it for non-GSE lending first, and then GSE lending, the long-term price ceiling for FICO scores comes down. This is a multi-year risk to watch, not an immediate catastrophe, but a real challenge to the pricing power that has driven so much of FICO’s earnings growth.

The Software Business: What the Bears Miss

When people debate FICO, they focus almost entirely on Scores. The Software segment is becoming very interesting.

FICO Platform is an enterprise AI decisioning system. Banks use it to automate loan origination, fraud detection, and collections. Insurers use it for underwriting. Telecoms use it to manage credit exposure. T-Mobile recently deployed a FICO Platform solution it says transformed its onboarding capabilities for connected device financing.

Platform Dollar-Based Net Retention Rate is 136%. That means existing Platform customers spend 36% more each year, on average. Enterprise software companies with NRR above 120% are considered elite. FICO Platform is delivering at a level that suggests real product-market fit, not just price increases.

The migration story matters too. Non-platform software ARR is declining as legacy customers move to Platform. This creates a short-term ARR headwind but a long-term margin expansion story, as SaaS recurring revenue is more predictable and higher lifetime value than old-school licenses.

FICO’s financial profile is unusual. The company carries net debt, largely from aggressive share buybacks. But the Scores business generates so much free cash flow that this is manageable.

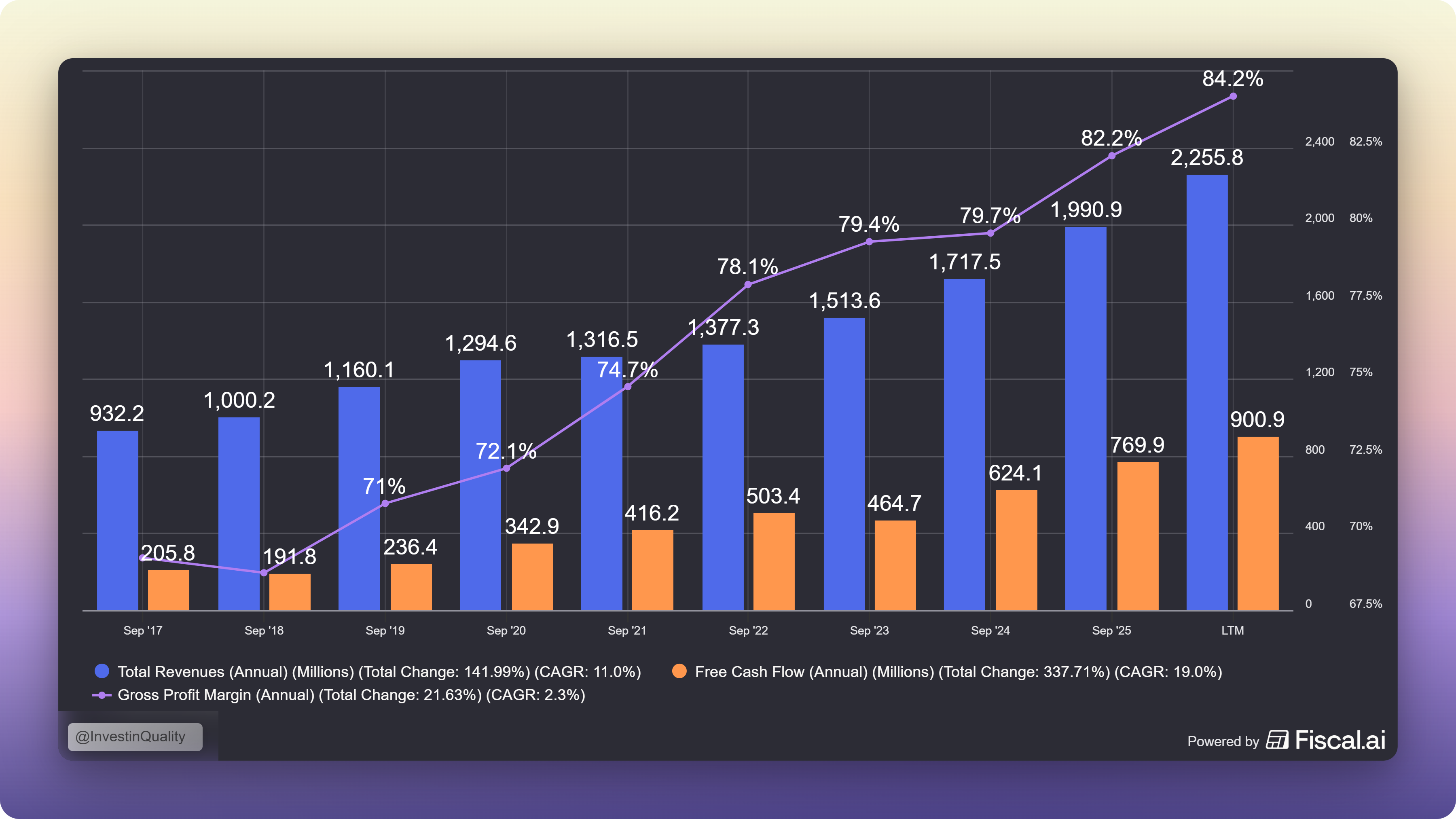

In fiscal year 2025:

Revenue: $1.99 billion, up 15.9%

Free cash flow: $769.9 million, up 23.4%

Diluted EPS: $26.54, up 29.78%

Shares bought back: $1.58 billion worth

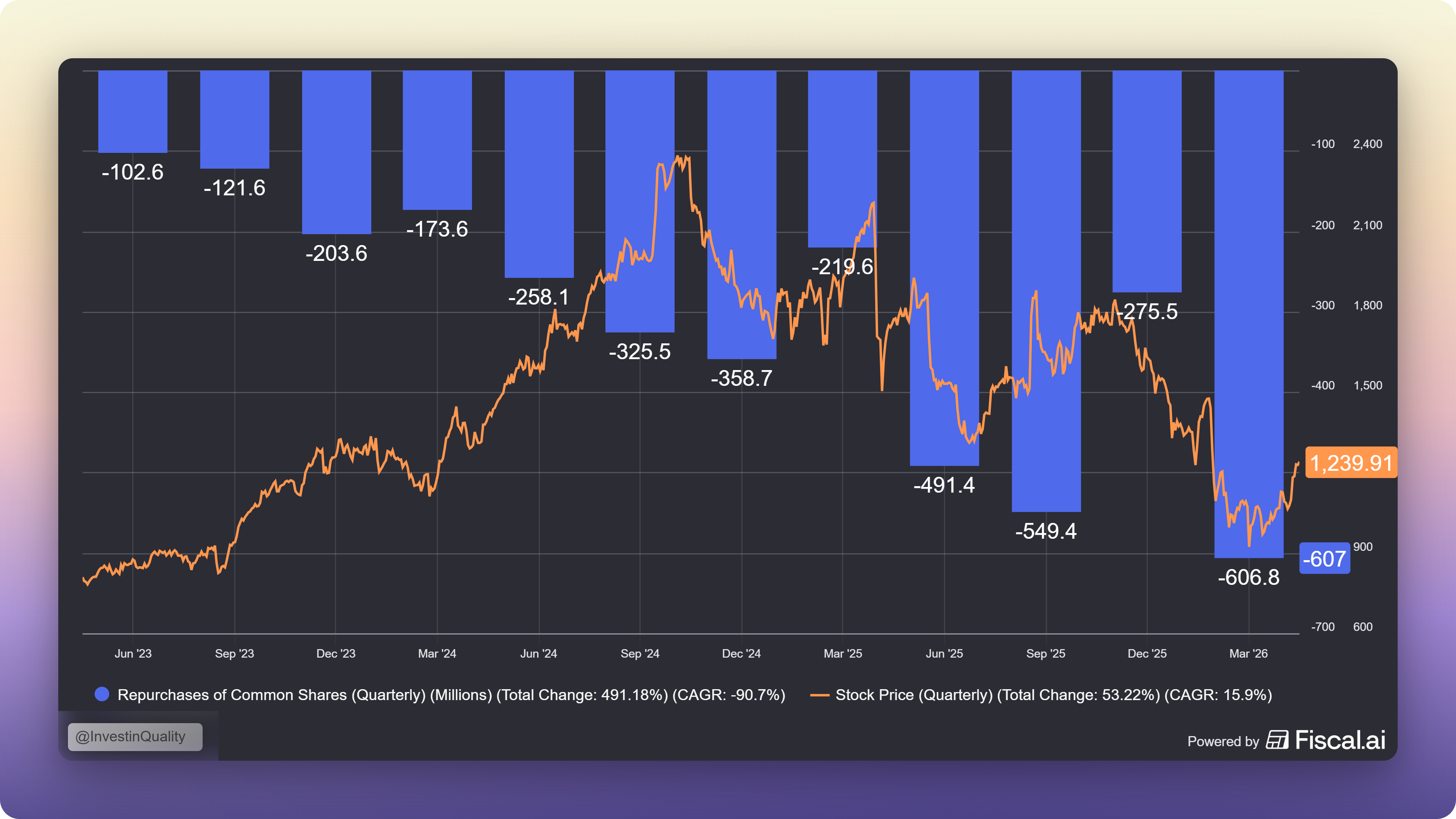

Note the share count. FICO has been buying back stock aggressively for years. The per-share economics compound faster than the headline revenue numbers suggest. Aggressive buybacks works out great when the stock price is fair, but when multiples get extreme (like in 2024-2025) the capital allocation is questionable.

In Q2 FY2026, FICO deployed $606 million in buybacks in a single quarter, the largest in company history, plus $170 million more after quarter-end. At a stock price around $1,100 at the time, that is a significant signal from management.

The Scores segment runs at roughly 89% operating margins. The non-GAAP operating margin for the company overall reached 58% in recent quarters. Trailing four-quarter free cash flow as of Q2 FY2026 was $867 million, up 28%.

Growth: Where Does It Come From Here?

FICO’s revenue growth has three drivers.

Volume

More credit pulls as the economy grows, housing activity recovers, and auto financing continues. This is modestly positive and relatively predictable.

Price

FICO has raised mortgage royalties four times in its history, three of them in the last three years. The VantageScore threat limits how aggressively this continues in mortgages, but there is real runway in auto, card, and personal loan markets, where pricing has been flat for years. B2C direct consumer pricing is also under monetized.

| Seeking Alpha")

Platform growth

With Platform ARR growing 49% and NRR at 136%, this segment is in the early stages of its potential. FICO’s installed base of enterprise clients is enormous. Attaching more Platform use cases to existing relationships is a multi-year growth driver that doesn’t depend on credit cycle dynamics at all.

Consensus estimates point to roughly 15 to 18% EPS growth over the next two years. Given the buyback program reducing the share count by about 2.5% annually, free cash flow per share growth will run above headline revenue growth.

Valuation

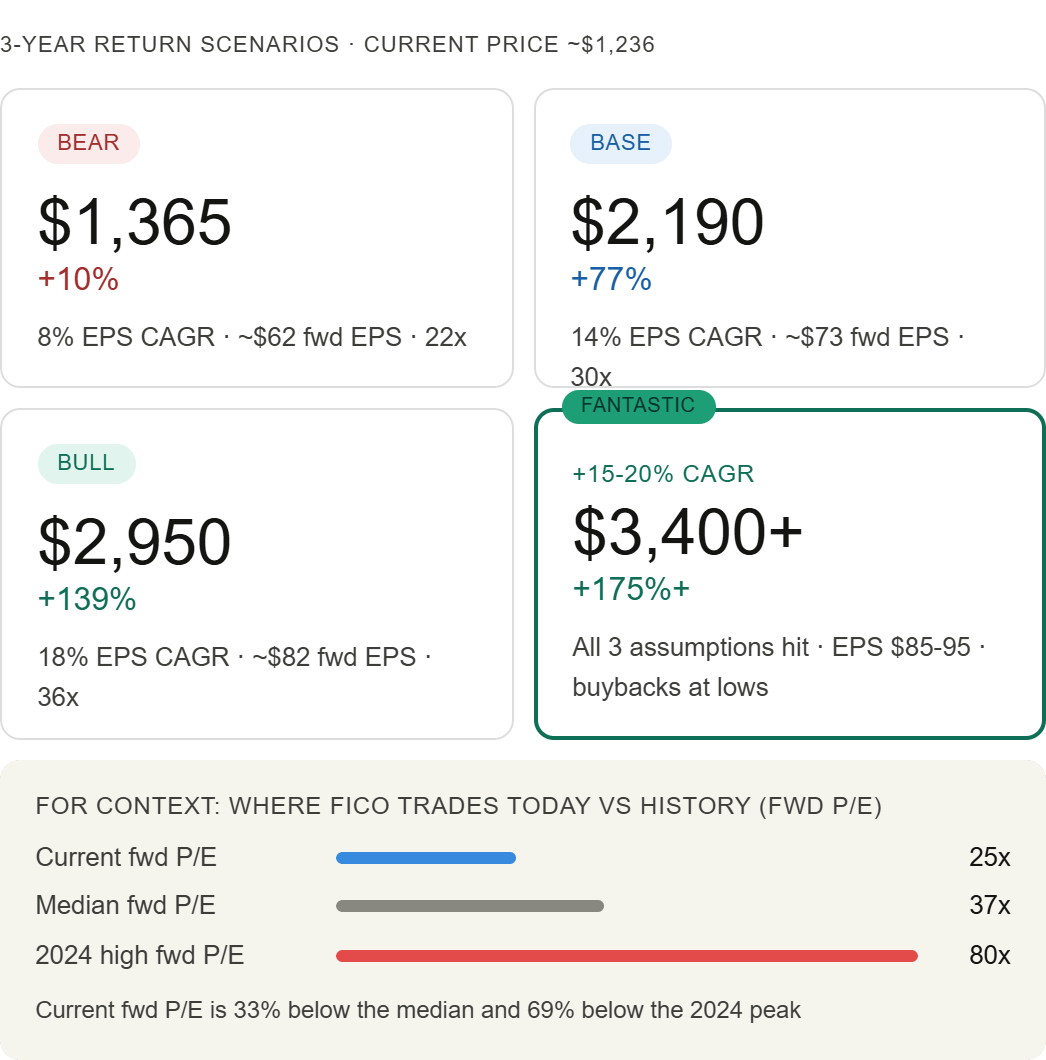

At roughly $1,236 per share (May 2026), FICO trades at:

25x forward earnings

32% below its 10-year average multiple of 37x

69% below the September 2024 peak

Here are my scenarios for FICO:

The base case: continued double-digit growth from scoring volume and Platform expansion, with a modest re-rating toward (but not back to) historical averages, generates attractive returns from today’s price.

The bear case requires a collapse in Scores pricing power AND the Software segment stalling AND the market assigning a sub-25x multiple to a still-cash-generative business. That’s a lot going wrong simultaneously.

Three Assumptions for a Fantastic Outcome (+15-20% CAGR) 🚀

For FICO to compound at 15 to 20% per year from here, three things need to go right.

Assumption 1: VantageScore adoption stays slow for 5+ years.

The regulatory door is open, but building a new standard takes decades. If mortgage lenders move slowly (which history strongly suggests), FICO’s B2B Scores revenue continues to grow even at flat pricing. Price increases in auto and card scoring (where VantageScore has no regulatory mandate) provide an additional tailwind. This alone could add 8 to 10 percentage points to annual EPS growth.

Assumption 2: FICO Platform becomes a $1B+ ARR business by 2028.

Platform ARR is $349 million today, growing at 49% with 136% net retention. If growth slows to a still-excellent 30% per year, Platform hits $1 billion ARR by late 2027 or early 2028. At Software margins that are expanding as the mix shifts to SaaS, this would add meaningful earnings power and justify a higher quality multiple across the whole business.

Assumption 3: Management keeps returning capital aggressively at depressed prices.

The Q2 FY2026 buyback of $605 million in a single quarter (when the stock was near multi-year lows) is the kind of capital allocation that creates enormous per-share value. If management continues deploying $1+ billion per year in buybacks at depressed prices and the business keeps growing, the per-share earnings math becomes very compelling very fast. EPS in FY2028 in this scenario could reach $55 to $60, versus ~$32 today.

None of these assumptions require anything extraordinary. They require the business to keep doing what it has done for 30 years, while management continues to be disciplined with the cash it generates.

What Must Be True for the Base Case

Even for the base case to work, you need to believe:

FICO’s VantageScore headwind plays out slowly, not suddenly. The operating evidence today: 42% B2B Scores growth in Q3 FY2025, strong Q1 FY2026 results, supports the slow-transition view.

Pricing power survives in non-mortgage markets. Auto, card, and personal loan scoring have seen almost no price increases. These are large markets where FICO’s position is equally dominant.

The FICO Platform compounds. With 136% NRR and 49% ARR growth, this is the kind of business that can grow for years inside an existing customer base.

Management keeps allocating capital well. Will Lansing has run this company since 2007. The buyback program has been consistent and value-accretive for years.

The Bear Case Simply Put

The bureaus own VantageScore. They will subsidize it at $1 per score because every FICO score they displace is economics that stays inside their ecosystem. Over 5 to 10 years, lenders adopt VantageScore for more and more use cases. FICO’s pricing power erodes. Revenue growth slows from mid-teens to mid-single digits. The stock, previously priced as a quality compounder at 40 to 50x earnings, re-rates to 20 to 25x. You get a decade of flat returns.

This scenario is what the stock is partially pricing today. It is not crazy. It requires close monitoring.

Concluding Thoughts

FICO invented credit scoring, became the universal language of creditworthiness in the world’s largest economy, and spent three decades building a pricing moat so strong it can charge $4.95 for something that costs almost nothing to produce.

The VantageScore threat is real. The regulatory environment is hostile. The stock got expensive at the peak.

But at 25x forward PE, 48% below its peak in 2024, with an $867 million free cash flow machine, management buying back stock at the fastest pace in the company’s history, and a Platform business growing at nearly 50% per year, the risk-reward looks more interesting than the narrative suggests.

This is not a set-and-forget holding. The VantageScore situation requires active monitoring. If adoption accelerates and Scores pricing starts to compress meaningfully, the thesis weakens. But the bears are pricing in a level of structural decline that the current operating numbers do not support.

FICO is not a broken business, yet. Currently it is discounted. Whether that discount is temporary or permanent is a question that will take 3 to 5 years to answer fully.

Whether I decide to start a position in FICO remains to be decided, you can follow the Quality Growth portfolio and get premium content by becoming a member today:

Ready to take the next step? Here’s how I can help you grow your investing journey:

Go Premium — Unlock exclusive content and follow our market-beating Quality Growth portfolio. Learn more here.

Essentials of Quality Growth — Join over 300 investors who have built winning portfolios with this step-by-step guide to identifying top-quality compounders. Get the guide.

Free Valuation Cheat Sheet — Discover a simple, reliable way to value businesses and set your margin of safety. Download now.

Free Guide: How to Identify a Compounder — Learn the key traits of companies worth holding for the long term. Access it here.

Free Guide: How to Analyze Financial Statements — Master reading balance sheets, income statements, and cash flows. Start learning.

Get Featured — Promote yourself to over 24,000 active stock market investors with a 42% open rate. Reach out: investinassets20@gmail.com

Disclaimer:

This newsletter is for informational purposes only and does not constitute financial, investment, or other professional advice. The views expressed are solely the author’s opinions and may change without notice.

Investing in securities involves risk, including the potential loss of capital. Past performance is not indicative of future results.

The author may hold positions in securities mentioned. Readers should do their own research and consult a licensed financial advisor before making investment decisions.

FICO is a toll booth on every mortgage, and each per score price hike drops almost fully to the bottom line. At 25x forward with those margins, the market is pricing moat erosion the filings have not confirmed yet.

It all comes down to how much the government will flex here. They could simply cap further price increases to the rate of inflation. Or they could treat them like a Utility and make them file a rate case to prove that their costs have increased and need to raise their price to earn a return on capital