5 Steps to Identify a Strong Moat 🏰

Moats matter for long-term compounding

Hi there, investor 👋

Warren Buffett has spent decades looking for one thing: businesses that can stay profitable for years, even when competitors try to steal their customers.

He calls this advantage a “moat.”

Think of medieval castles. The wider and deeper the moat around the castle, the harder it was for invaders to get in. Same with businesses. The stronger their competitive advantage, the harder it is for rivals to chip away at their profits.

Here’s the thing most investors miss: not every successful company has a moat. Some businesses are great today but vulnerable tomorrow. Others look boring but are practically impossible to displace.

The difference? Five questions.

Question 1: Can Competitors Easily Copy This?

This is where most companies fail the moat test.

If a rival can replicate your business model in six months, you don’t have a moat. You have a head start. And head starts evaporate fast.

Take restaurants. You can copy almost anything—the menu, the decor, the service style. That’s why most restaurants struggle to maintain high margins. There’s always another spot opening down the street.

")

Compare that to Visa. Good luck building a competing payment network. You’d need to convince millions of merchants and billions of consumers to switch. Even with unlimited money, it would take decades.

The pattern: Patents, proprietary technology, massive scale, or network effects create moats. Execution alone doesn’t.

Question 2: Would Customers Care if This Company Disappeared?

Brutal question. But it cuts right to the core.

If your business vanished overnight, would customers scramble to find you? Or would they shrug and buy from whoever’s convenient?

Survey")

Coca-Cola passes this test easily. People have emotional connections to the brand. They’ll pay more for Coke than generic cola, even when the taste difference is minimal. That’s pricing power—the ultimate sign of a moat.

Airlines? They fail hard. Nobody cares which airline they fly. They just want the cheapest ticket. That’s why airlines have such terrible economics despite moving millions of people every day.

The test: If customers view your product as interchangeable with competitors, you’re a commodity. Commodities don’t have moats.

Question 3: Does the Company Have Pricing Power?

Here’s the simplest moat test: If they raised prices 10% tomorrow, would customers keep buying?

Apple can do this. They’ve done it repeatedly with iPhones, and people keep lining up. That’s a moat.

Most retailers can’t. Raise prices and shoppers just go next door. That’s the absence of a moat.

")

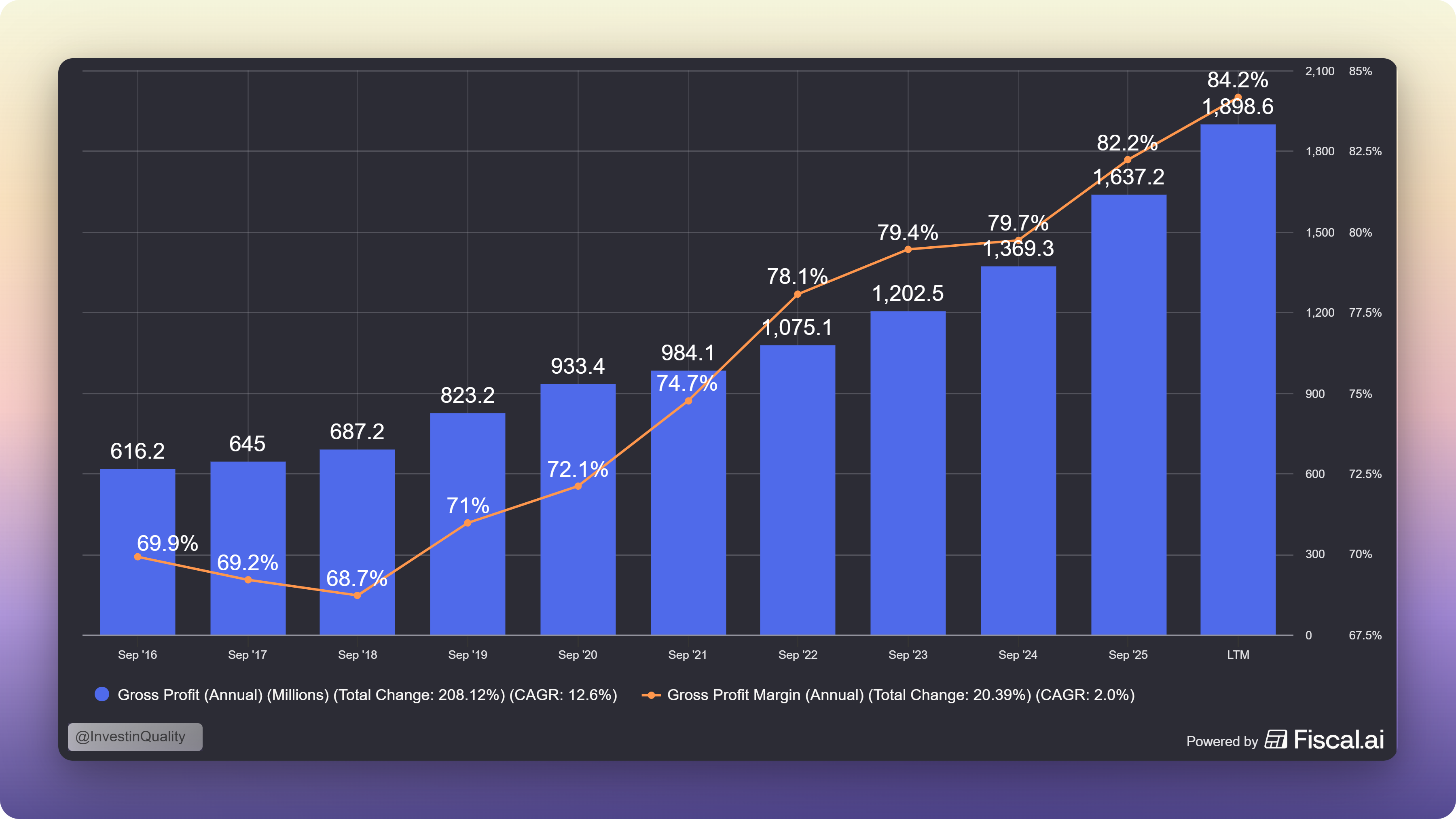

Pricing power shows up in the numbers. Look at gross margins over time. Companies with moats maintain or grow their margins. Companies without moats see margins slowly erode as competition forces prices down.

Fico is a great example of pricing power and increasing gross margins:

Costco is also interesting. They deliberately limit their pricing power—they cap markups at 14% on branded goods and 15% on their Kirkland private label. But this constraint is actually their moat. By committing to low prices, they’ve built customer loyalty so strong that their membership renewal rate exceeds 90%. Members know Costco won’t gouge them, so they keep coming back.

The insight: Real pricing power means you can raise prices without losing customers. If you can’t, your moat is weak or nonexistent.

Question 4: Are Returns on Capital High and Staying High?

This is where finance meets reality.

Return on Invested Capital (ROIC) measures how much profit a company generates from every dollar it invests in the business. High ROIC companies turn money into more money efficiently.

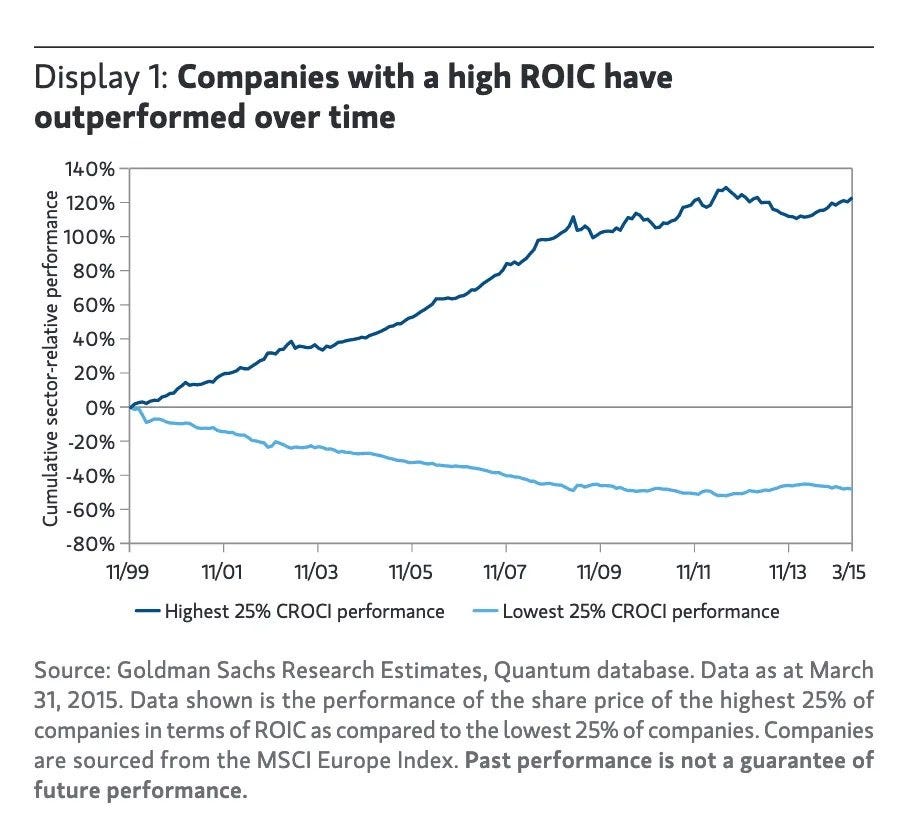

We know that high ROIC businesses perform much better than their low-ROIC counterparts:

But here’s what matters for moats: consistency.

Companies with real moats maintain high returns on capital year after year. Why? Because their competitive advantages protect them from the usual pattern where high returns attract competition and drive returns back down.

Look at Microsoft. For decades, they’ve generated returns on capital well above 20%. Competitors try to chip away at Office, Windows, and now Azure, but Microsoft’s ecosystem moat keeps the profits flowing.

Compare that to most retailers or manufacturers. They might have one great year with high returns, but then competition catches up and returns fall. That’s capitalism working—but it also signals no moat.

The data: According to research from Missouri State University, companies with wide economic moats consistently outperform companies with no moat. The difference isn’t subtle. It compounds over decades.

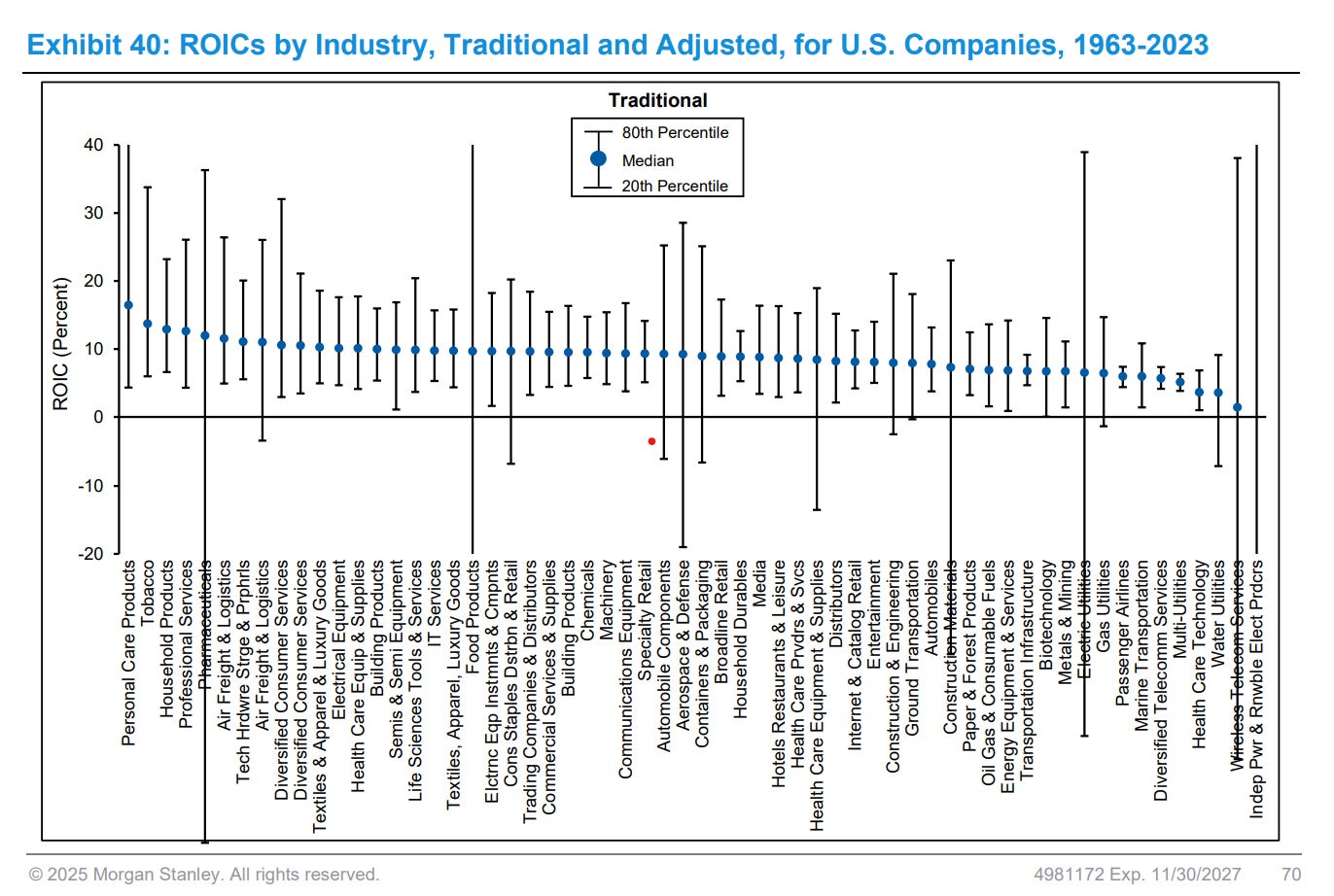

Here are the highest ROIC industries for US companies:

Question 5: Is the Moat Getting Wider or Narrower?

Moats aren’t static. They’re always changing.

Buffett himself says moats are either widening or shrinking, even when the changes aren’t obvious in the short run.

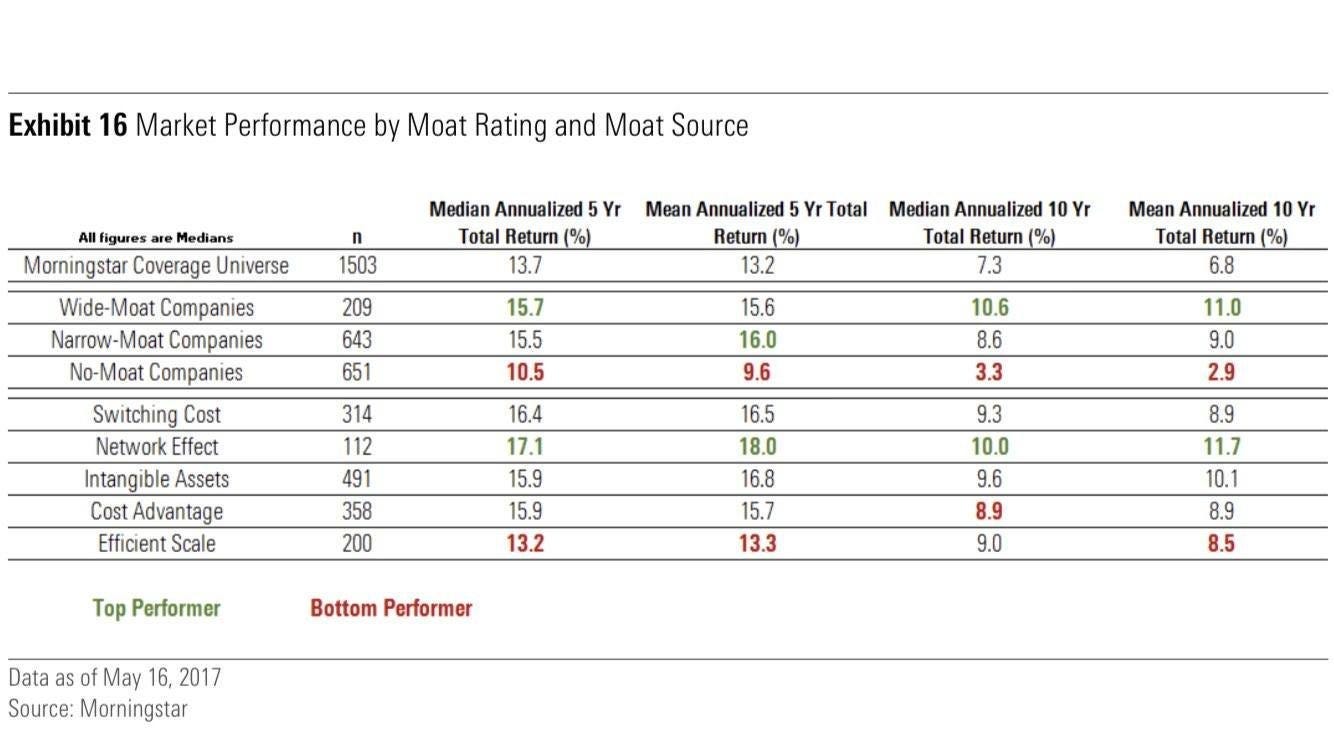

Here’s a breakdown from Morningstar on different moat types:

From the data, wide and narrow moat businesses outperform the no-moat companies significantly.

Amazon’s moat has widened dramatically. Every new Prime member makes the service more valuable. Every third-party seller on the platform gives customers more options. Every AWS customer makes Amazon’s cloud business harder to displace. The feedback loops compound.

Traditional retail banks? Their moats are shrinking. Fintech companies can now do most of what banks do—and they’re doing it cheaper and faster. The regulatory moat banks once enjoyed is eroding.

The question: When you look at a company, ask yourself: will their competitive advantage be stronger or weaker in five years?

If you want to get deeper into this subject, I highly recommend Measuring the moat by Mauboussin.

Real World Examples

Let’s apply this framework:

Costco - Wide Moat:

Can’t copy the scale advantages and buying power (Question 1)

Customers love the treasure hunt experience and low prices (Question 2)

Membership model locks in recurring revenue, 90%+ renewal rates (Question 3)

Consistent returns year after year (Question 4)

Global expansion and e-commerce growth widening the moat (Question 5)

Apple - Wide Moat:

Brand built over decades, impossible to replicate (Question 1)

Emotional connection drives customer loyalty worldwide (Question 2)

Can charge premium prices vs. competitors (Question 3)

Maintains high margins despite intense competition (Question 4)

Brand strength endures across generations (Question 5)

Most Airlines - No Moat:

Easy to replicate business model (Question 1)

Customers just want cheap tickets (Question 2)

Zero pricing power, constant fare wars (Question 3)

Returns on capital barely cover cost of capital (Question 4)

Competition keeps intensifying, any advantage is short lived (Question 5)

Why This Matters For Your Money

Companies with wide moats compound returns over decades.

Think about it: if a company can maintain high returns on capital while reinvesting profits back into the business, shareholders win. The returns compound.

Research from Morgan Stanley shows that companies sustaining ROIC above their cost of capital for longer than the market expects generate significantly higher returns for shareholders. These are the “compounders” that create generational wealth.

But companies without moats are traps. They might look cheap on a P/E ratio, but cheap isn’t enough if profits are about to get competed away.

This is why we’re very careful about buying bargain stocks. The price often reflects the quality (But not always).

Conclusion

Five questions. That’s all you need.

Can competitors copy this? Would customers care if it disappeared? Can they raise prices? Are returns staying high? Is the moat widening or shrinking?

Get these right, and you’ll avoid most bad investments.

Because in the end, capitalism is brutal. High profits attract competition like blood attracts sharks. The only defense is a moat wide enough to keep the sharks out.

Most companies don’t have one. The ones that do are worth finding—and holding onto.

Whenever you are ready, this is how I can help you:

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Essentials of Quality Growth — Join more than 300 investors who have bought the guide. Essentials of Quality Growth Investing is a multi-step guide for building a stock market portfolio of 10-20 high-performing quality compounders.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

(Free) How to analyze the financial statements — Learn how you read & analyze the balance sheet, income statement, and cash flow statement.

Promote yourself to +25.000 stock market investors (42% open rate) — Contact us via: investinassets20@gmail.com

This is such a clear breakdown of something that actually matters for long-term investing. I especially liked how you made "moat" concrete—it's easy to throw that word around, but your framework helps people see what to actually look for in a business.