5 Quality Businesses March 💎

High quality businesses pulling back -20% to -50%

Hi partner! 👋🏻

Welcome to the March edition of Top 5 Buys ✅

In this article, we will discuss our top stock picks for March 2026.

Let’s get into it 👇

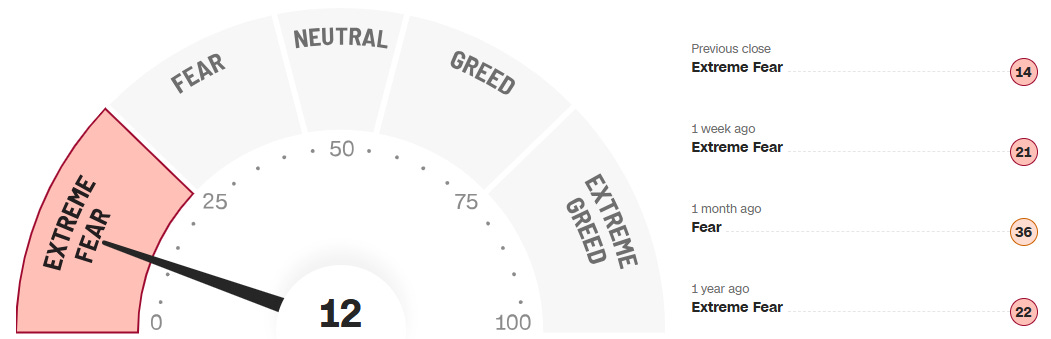

The Market Sentiment: Extreme Fear

March 2026 has been one of the most turbulent months in recent memory. The market is volatile as a result of:

A US-Israeli military strike on Iran → sending oil prices surging above $100

Trump’s 15% global tariff regime → with consumers and businesses absorbing most of the cost

Inflation refusing to cooperate → PCE at 2.9%, the Fed stuck between a rock and a hard place

A slowing economy → the weakest job growth outside of the pandemic since 2009

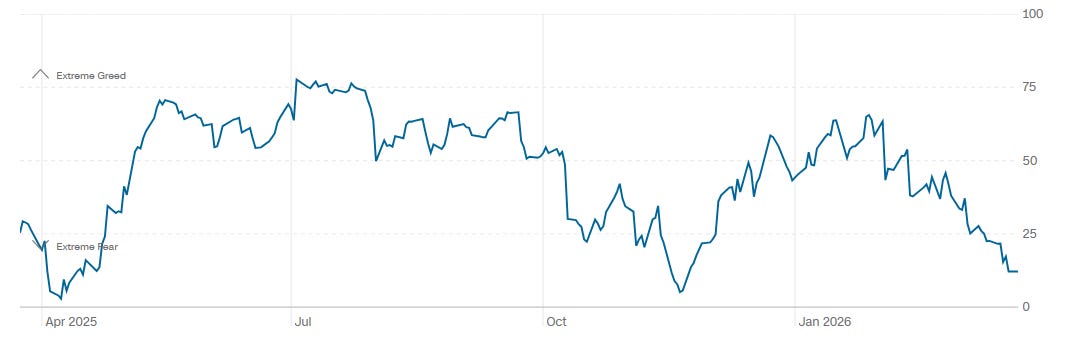

Investors are responding with extreme fear. The Fear & Greed Index currently sits at 21, deep in Extreme Fear territory.

The crazy part?

Despite elevated volatility drifting toward 19-20%, the S&P 500 year-to-date returns remain near flat, only down -1.63% YTD (Still close to all time high levels).

This is because the largest companies are holding up. Nvidia just unveiled its Vera Rubin platform at GTC 2026. Microsoft, Alphabet and the mega-caps are absorbing the uncertainty better than most.

Growth and SaaS stocks have not been so fortunate. The combination of tariff fears, geopolitical chaos and the agentic AI narrative continuing to pressure software multiples has hit many former darlings hard. The entire SaaS category is trading at its lowest forward EV/Sales in recent times:

Predicting the future is impossible. But we can point to 5 quality growth companies likely to keep compounding, regardless of tariffs, oil prices, or whatever headline drops next week.

Disclaimer:

The author may hold positions in securities mentioned. Readers should do their own research and consult a licensed financial advisor before making investment decisions.

Here are this month’s Top 5 👇

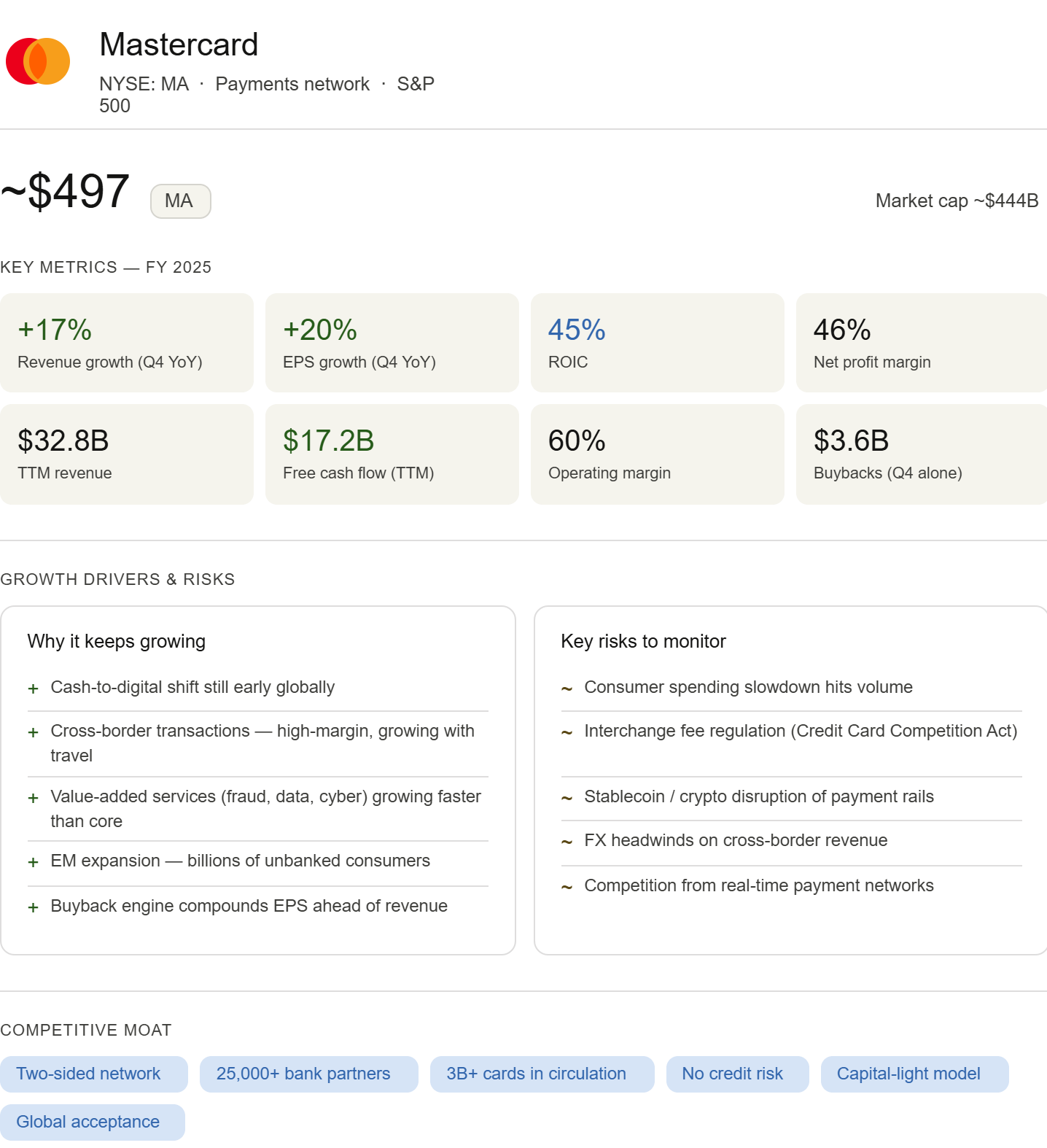

1. Mastercard MA 0.00%↑

The business model

Mastercard is a global payments network sitting between cardholders, banks, and merchants, processing transactions across more than 150 currencies in virtually every country on earth.

Critically, it takes on zero credit risk. It earns a small toll on every transaction that crosses its rails and moves on.

In the last twelve months, Mastercard generated $32.8 billion in revenue and nearly $15 billion in net profit, running a 60% operating margin and a 45% net margin.

The business model requires almost no capital to grow, with free cash flow of $17.2 billion against capex of just $489 million. With over 3 billion cards tied to a two-sided network connecting 25,000+ financial institutions, the competitive position is structural. The more issuers and merchants on the network, the more valuable it becomes for everyone else.

Growth drivers

The long-term thesis rests on one durable shift: the global migration of payments from cash to digital.

Most consumer transactions worldwide are still made in cash, particularly in emerging markets where Mastercard is actively expanding.

On top of that secular tailwind sit cross-border transactions, a high-margin segment that grows with international travel and e-commerce, and value-added services including fraud analytics, data insights, and cybersecurity.

All of these are growing faster than core and carry higher margins. Q4 2025 net revenue grew 15% to $8.8 billion, EPS grew 20%, and management guided for high-end low-double-digit currency-neutral growth in 2026.

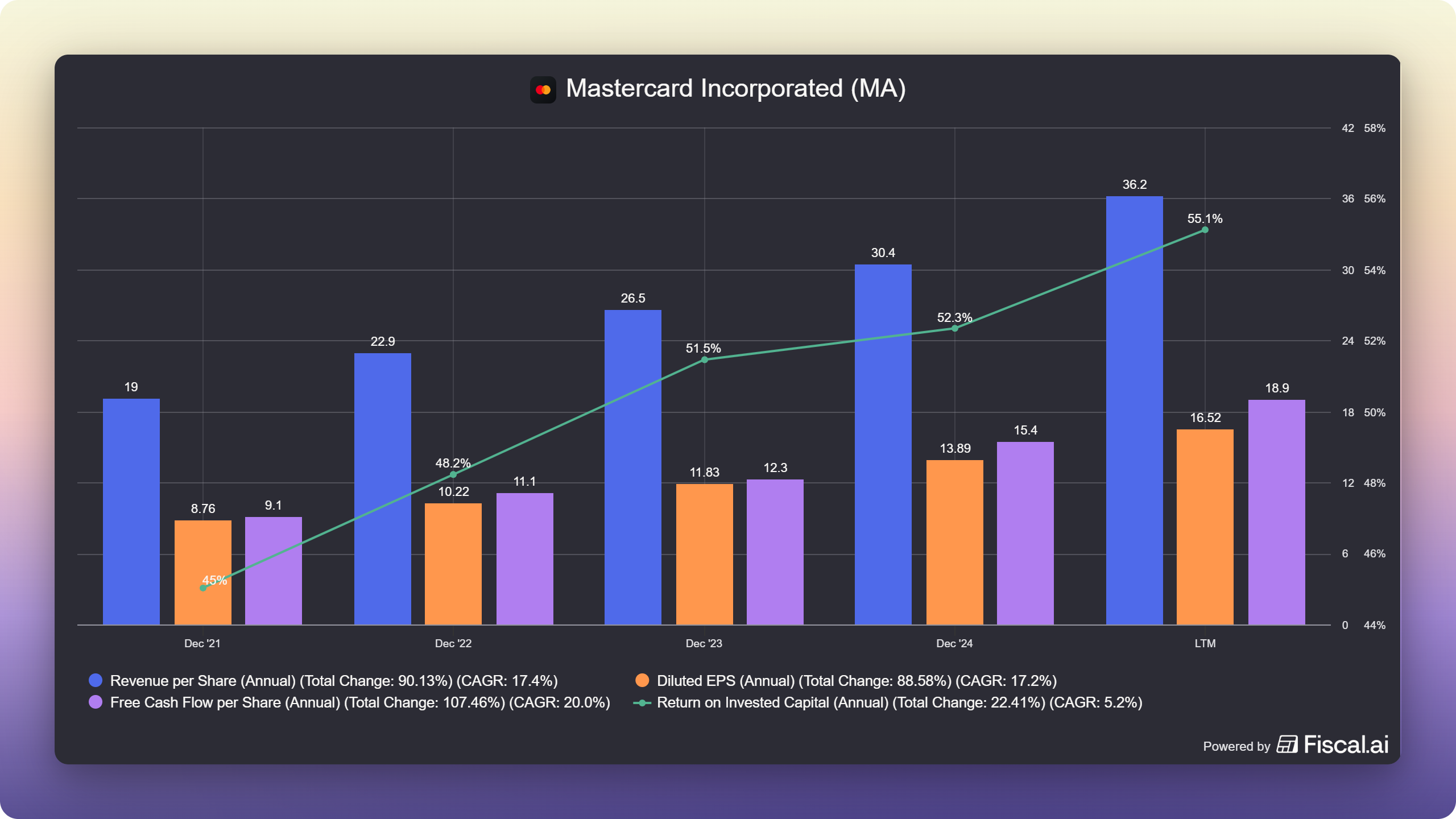

The last 5 years of growth for Mastercard have been significant, growing revenue per share by 17.4%, EPS by 17.2%, and FCF per share by 20% CAGR with expanding Return on Invested Capital:

The buyback engine adds a further mechanical tailwind: Mastercard repurchased $3.6 billion of stock in Q4 alone, consistently compounding EPS ahead of revenue growth.

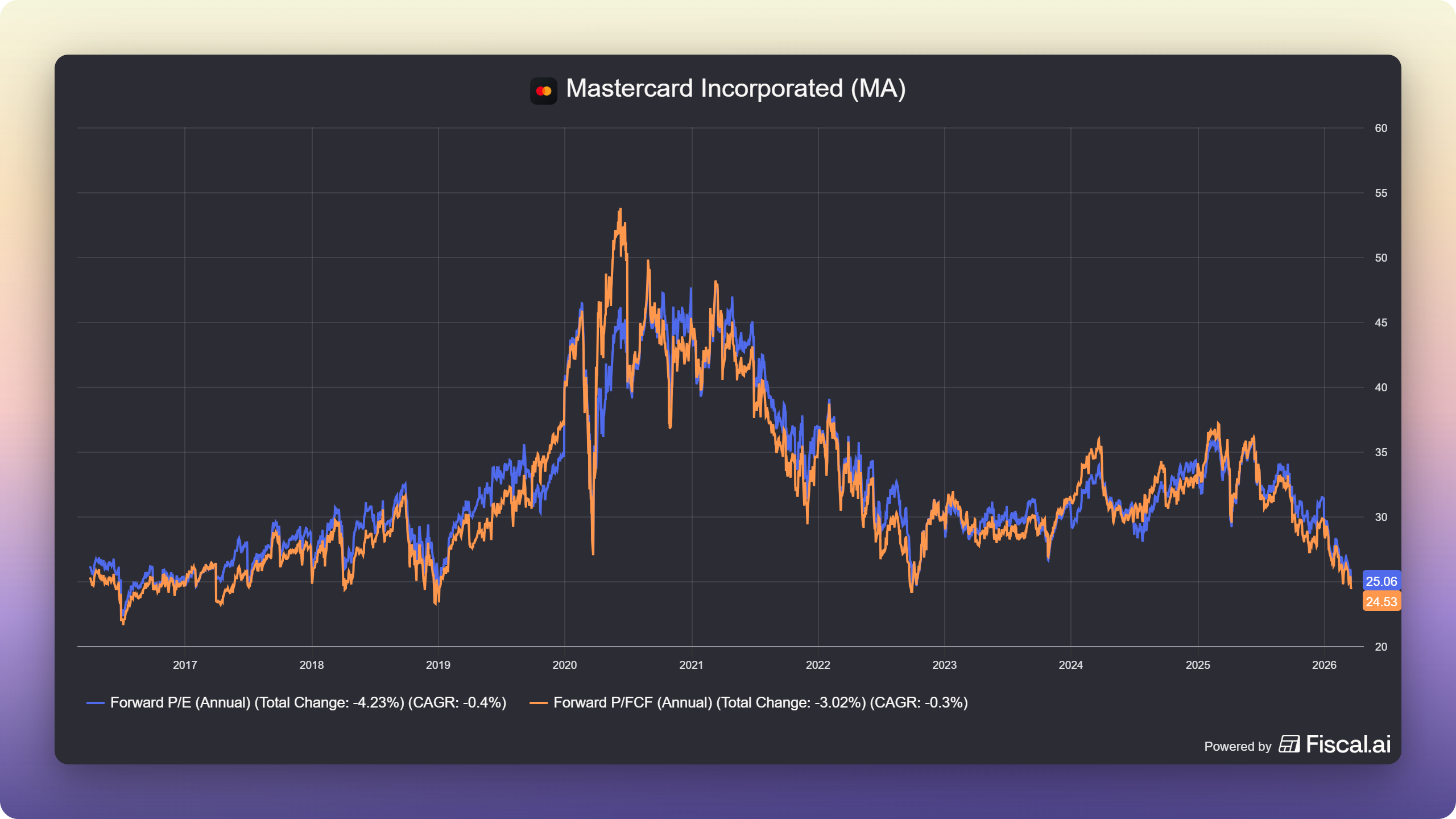

Valuation

Mastercard trades at a forward PE of around 25x, close to its 10 year low of 22.3x. The forward P/FCF is currently 24.5x, also well below its 10 year median multiple:

For a business compounding EPS in the high teens, a multiple of ~25x is arguably the most attractive entry point relative to its own history in years.

The analyst consensus target is $658, implying roughly 19% upside with a strong buy rating. The risk is macro, not structural. A slowdown in consumer spending or a regulatory intervention on interchange fees could temporarily compress volumes. For a long-duration compounder of this quality, the current price looks like a reasonable entry.

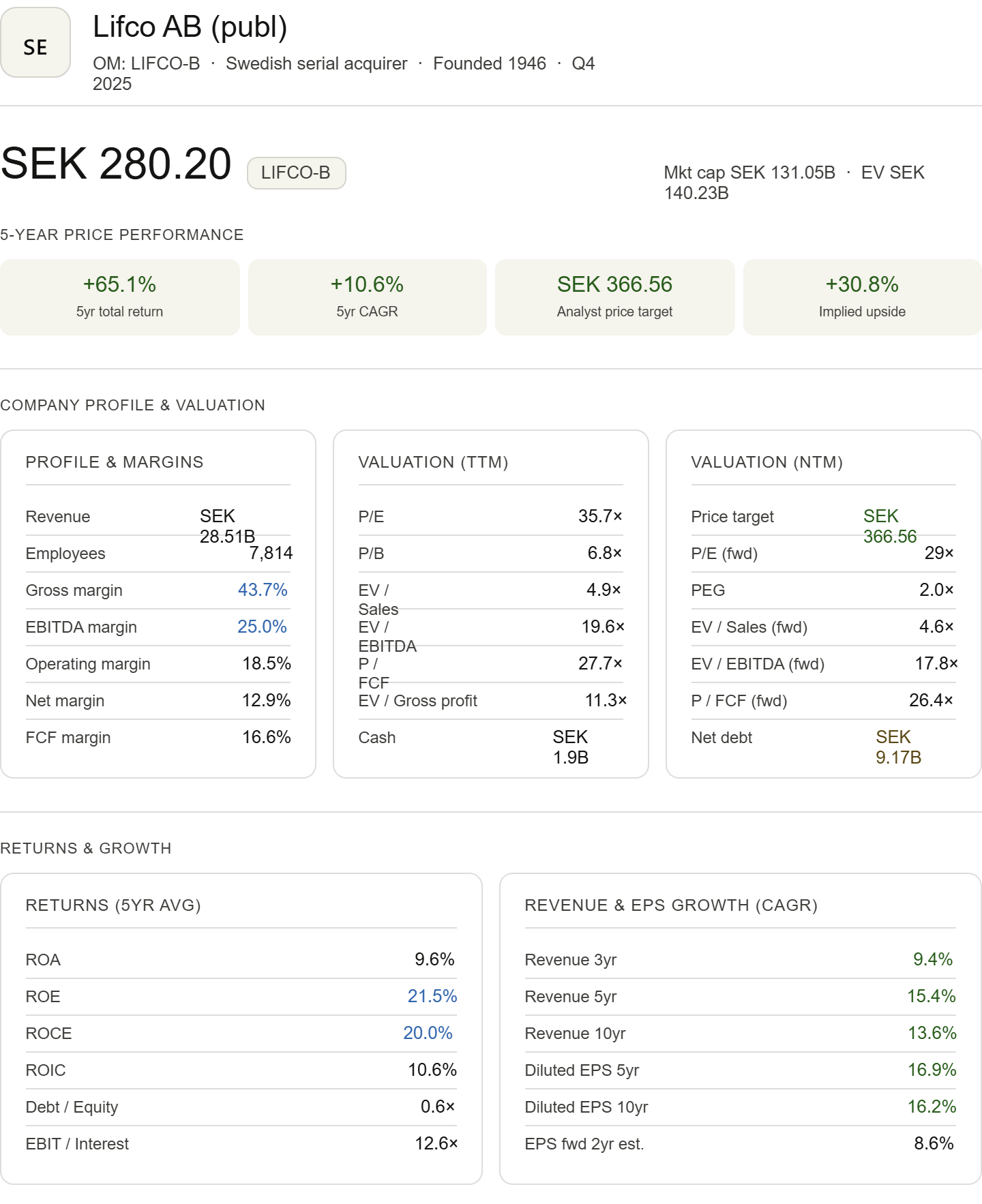

2. Lifco AB $LIFCO-B

The business model

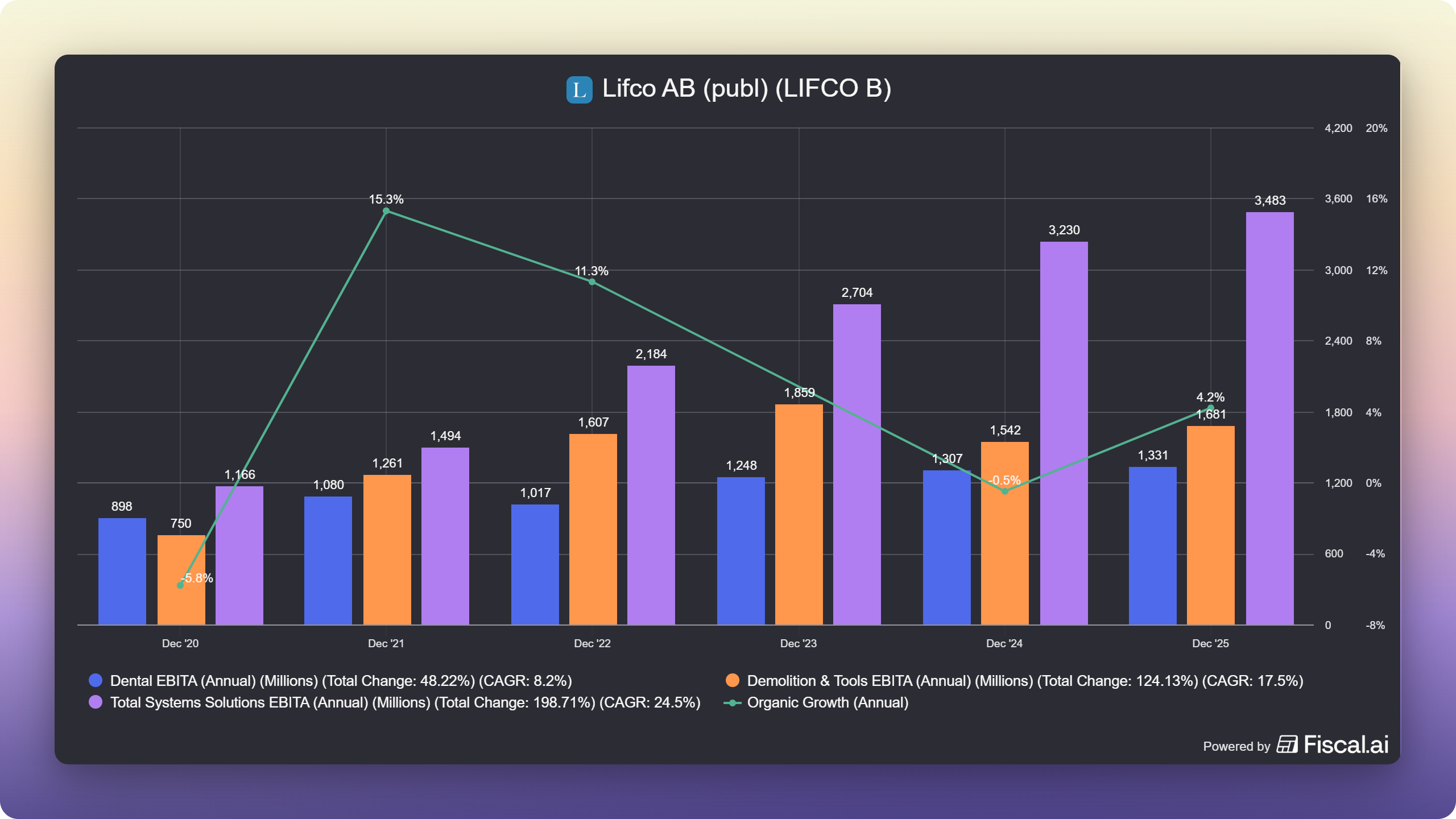

Lifco is Sweden’s best-kept secret in quality investing. Built on the same decentralised serial acquirer model that made Constellation Software legendary, it owns 275 operating companies across 37 countries, organised into three divisions: Dental, Demolition & Tools, and Systems Solutions.

The primary business segment has compounded EBITDA by 8.2%, 17.5%, and 24.5% respectively, with organic growth ranging from -5.8% to +15.3% in the period:

The businesses Lifco owns are deliberately unglamorous: dental consumables, hydraulic demolition attachments, contract manufacturing.

That is precisely the point. Boring businesses in niche markets carry pricing power, low capital intensity, and minimal disruption risk. From 2015 to 2025, Lifco delivered an EBITDA CAGR of 18% and an EPS CAGR of 16%.

What drives growth from here

Acquisitions are the engine.

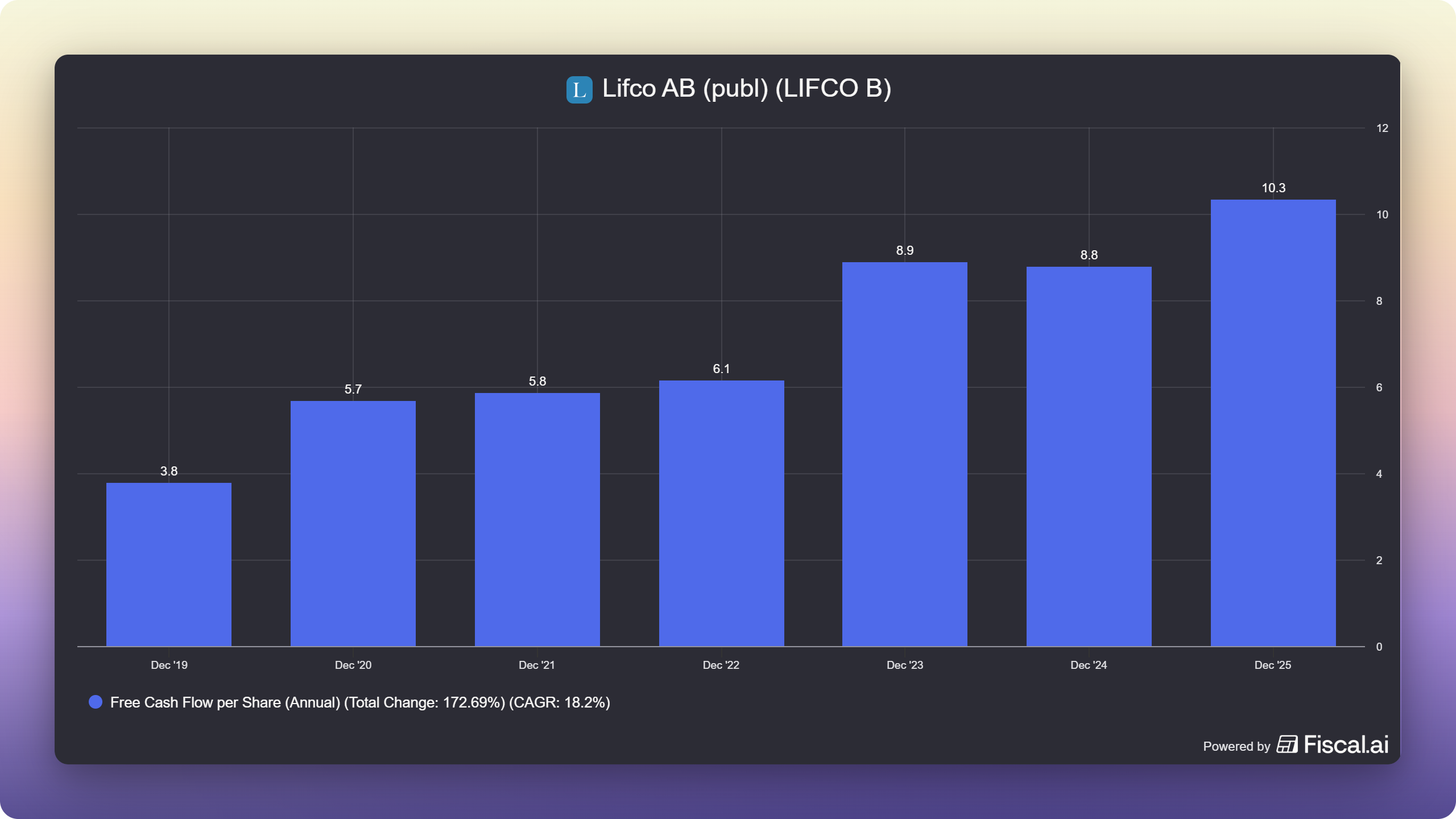

In 2025, Lifco completed 16 deals adding approximately SEK 2.2 billion in annualised net sales, while free cash flow per share has compounded at 18.2% annually since 2019.

The company targets founder-owned businesses in fragmented markets with few credible buyers, acquiring at sensible multiples and adding operational stability and efficiency.

The pipeline is structurally full. Thousands of private niche businesses across Europe and Globally will eventually need a buyer, and Lifco is patient, well-capitalised, and known as a permanent home.

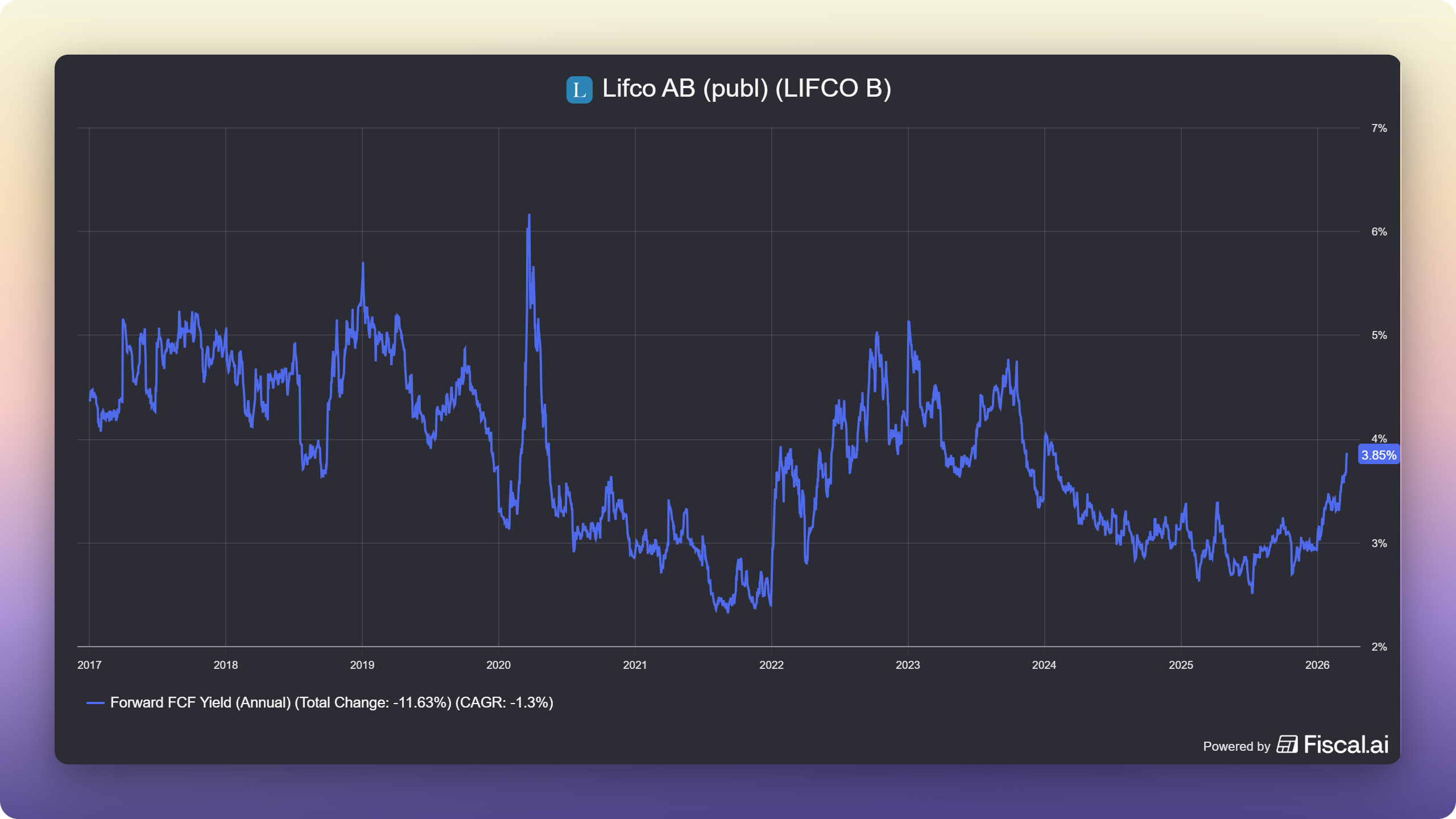

Valuation

At roughly SEK127 billion market cap, Lifco trades at a premium to European industrial peers, warranted given the consistency of its compounding and the capital-light nature of its portfolio.

The stock has contracted by -33.8% since its July 2025 highs, offering a rare chance to enter a proven compounder at a forward PE of 28.1x or a fwd. FCF yield of 3.85%.

Top 3 is for Premium subscribers only. Join us today:

Build a Market-Beating Portfolio of Quality Compounders, Now 30% Off

Many world-class compounders are currently trading at multi-year low levels. We do the work to identify the few that truly matter, businesses with durable moats, high returns on capital, and long reinvestment runways.

Inside the Premium service, you get:

💎 A focused portfolio of high-quality businesses

📈Clear buy & sell alerts

📚 Deep dives that actually explain why something works

📜 A repeatable framework you can use for life

Get 30% off before the price hike, and start building a portfolio designed to outperform over the next decade.

Don’t overcomplicate it. Own better businesses. Let time do the work.