💎10 Lessons from Seth Klarman

<5 min read

10 Lessons from Seth Klarman 💡

Klarman has achieved an annual return of almost 20% since 1983. He is one of the most successful value investors in history. Klarman diligently focuses on fundamentals and is constantly looking for the best value investments. This has served him well as he has accumulated a net worth of +$1.3 billion.

Klarman's portfolio consists of value investments. His biggest holding, Liberty Global, is a telco holding company that seems very cheap on all valuation metrics. He also has notable positions in VSAT 0.00%↑ , GOOG 0.00%↑ , and FIS 0.00%↑ .

10 Lessons from Seth Klarman 👑

Lesson 1:

“In a rising market, everyone makes money and a value philosophy is unnecessary. But because there is no certain way to predict what the market will do, one must follow a value philosophy at all times.”

Klarman focuses on value investing. He is looking for companies that are trading below their intrinsic value. This does not necessarily mean that it must have a very low PE ratio. A cheap business can come in many forms and sizes. The bottom line is that valuation work is very important in investing, and Klarman emphasizes this above all else.

Lesson 2:

"Patience and discipline can make you look foolishly out of touch until they make you look prudent and even prescient."

Buffett was ridiculed in the dot com bubble, as he refused to partake in the internet stock boom. He was later proven right as the bubble popped, and Berkshire was invested in reasonably priced quality businesses.

Lesson 3:

"Never stop reading. History doesn’t repeat, but it does rhyme."

Knowing the financial history, and how markets tend to move over time, is a major advantage for investors. We see time and time again that investors get rallied up for different trends that will take over the world. In the early 2000s, it was the internet, in 2018, it was crypto/blockchain, now it is AI.

Like this article?

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Lesson 4:

"A simple rule applies: if you don’t quickly comprehend what a company is doing, then management probably doesn’t either."

Similar to Buffett's approach of jumping 1-foot bars, instead of 7-foot bars. Complicated business models are usually hard to understand and explain. This is often a sign that the model is not so great. A great business is simple to explain. It should be simple to explain why the business is able to make more money than its peers for example.

Lesson 5:

"The prevailing view has been that the market will earn a high rate of return if the holding period is long enough, but the entry point is what really matters."

It took the Nasdaq 15 years to regain its dot com levels. Don't ever be fooled into believing that price doesn't matter.

Lesson 6:

"In investing it is never wrong to change your mind. It is only wrong to change your mind and do nothing about it."

As investors, we should change our minds when the facts change, and not be too attached to our "darlings". Human beings easily fall into the trap of defending their previous decisions. It is far easier to selectively look at data that supports your decision, compared to objectively looking at all the data, and making a decision based on that. We fall into what is called a “confirmation bias” where we want to confirm our beliefs, and neglect information that is contradictory.

Lesson 7:

"When all feels calm and prices surge, the markets may feel safe; but, in fact, they are dangerous because few investors are focusing on risk."

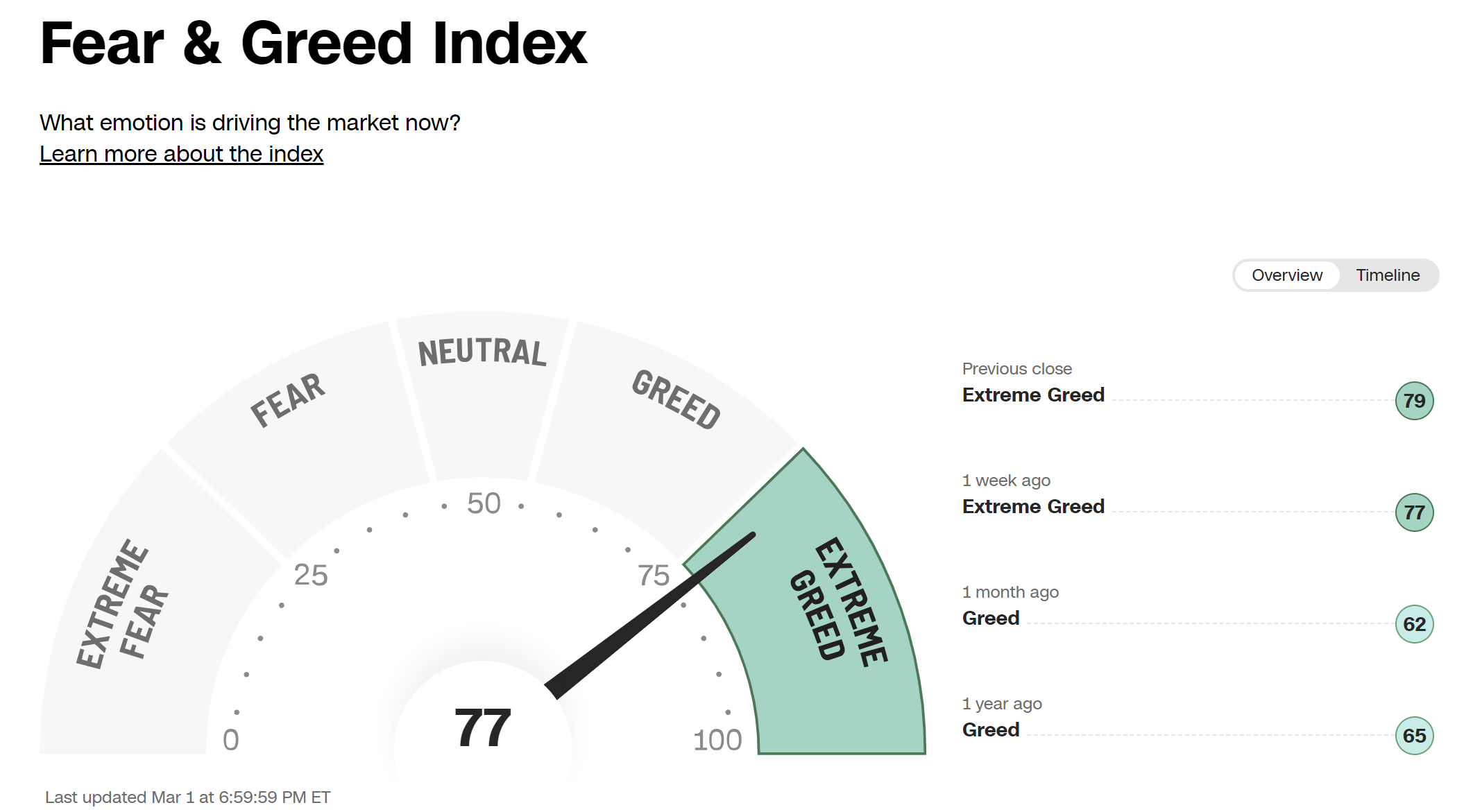

A hard concept to grasp, but in times of greed (such as we are in currently), the risk is much higher than when prices were suppressed (Oct 2022 for example). This is easy to identify in hindsight, but much harder to understand in the moment.

Lesson 8:

"The near absence of bargains works as a reverse indicator for us. When we find there is little worth buying, there is probably much worth selling."

Be mindful when everything seems overpriced. This can be a good opportunity to sell.

Lesson 9:

"There’s no such thing as a value company. Price is all that matters. At some price, an asset is a buy, at another it’s a hold, and at another, it’s a sell."

Price compared to the underlying asset and its earnings power is what we should focus on. A fast-growing business could have a PE of 50 and be cheap, and a business with a PE of 3 could be expensive - we have to determine what we think the future value of a business will be.

Lessons 10:

"The way to maximize outcomes is to focus on the process."

Like Benjamin Graham, Klarman is focused on improving his investing process. This is the single most important factor for retail investors to grasp. By having a well-defined investing system, you eliminate 95% of investing mistakes.

Whenever you are ready, this is how I can help you:

Go Premium to access exclusive content & follow our market-beating Quality Growth portfolio. Read more here.

Essentials of Quality Growth — Join more than 250 investors who have bought the guide. Essentials of Quality Growth Investing is a multi-step guide for building a stock market portfolio of 10-20 high-performing quality compounders.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

(Free) How to analyze the financial statements — Learn how you read & analyze the balance sheet, income statement, and cash flow statement.

Promote yourself to +6.500 stock market investors (48% open rate) — Contact us via: investinassets20@gmail.com

Invest in Assets, I absolutely loved reading this post. I'll share it with as many people as I can, especially with some friends who are just getting started on their investing journeys.