S&P Global: A Steady, Capital-Light, Quality Compounder 👑

<5 min read

This article is sponsored by Quartr

Sick of trying to get an overview of the earnings calls of all your holdings?

Quartr solves this by providing the best resource on the internet for:

Tracking quarterly and annual earning calls

Pulling out key slides and data in no time

Keeping track of company mentions

Try Quartr 7 days for free & get 20% off their Core & Pro plans

The Invest In Quality team has been using the Quartr service for years, it is fantastic.

S&P Global: The Business

S&P Global is a financial services company with a rich history dating back to the late 19th century. It has evolved into a global leader in the provision of essential data, analytics, and research for investors, corporations, and governments.

S&P Global is the leading provider of credit ratings on fixed-income securities. After the 2007-2008 Global Financial Crisis S&P Global separated itself from the underwriting process. This means that they are no longer a part of the debt prospectus and the risk of something similar happening again is reduced.

Business Model

S&P Global operates 3 primary diversified business segments that make up its business model:

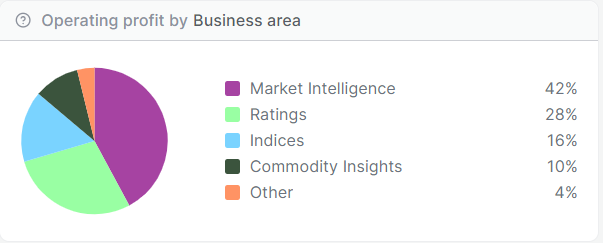

Market Intelligence: This segment offers a wide range of financial information, data, and analytics services to institutional and individual investors, as well as corporations. Its platforms, such as Capital IQ and Market Intelligence, provide customers with critical data for risk assessment, investment analysis, and strategic decision-making. Market Intelligence represents 42% of S&P’s operating profit.

Ratings: S&P Global Ratings is one of the largest credit rating agencies globally, providing credit ratings and related research for governments, corporations, and structured finance instruments. The ratings segment generates revenue from issuers and investors who rely on its assessments to make informed investment decisions. Ratings represent 28% of operating profits for S&P Global.

S&P Dow Jones Indices: S&P Dow Jones Indices creates and manages an extensive array of stock and bond indices, including the iconic S&P 500. It licenses these indices to exchange-traded funds (ETFs), mutual funds, and other investment products, generating revenue based on usage and licensing agreements. The indices segment represents 16% of the operating profits.

Commodity Insight: S&P Global delivers essential information and intelligence to industries that rely on commodity prices in their operations. S&P Global delivers comprehensive data, analysis, and insight into commodities like energy, metals, agriculture, and more.

Mobility: This is a segment that S&P Global got from their merger with IHS Markit. The business segment focuses on delivering data, analytics, and insights into the auto industry. The data is used by transportation and logistics firms, as well as investors and policymakers.

The segments sorted by operating profit:

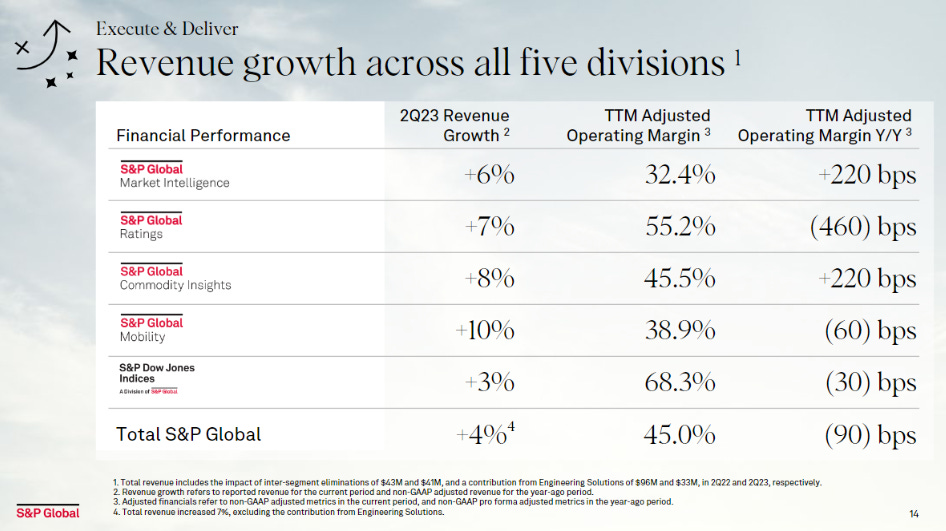

The business segments based on the most recent quarter:

S&P Global operates several high-margin businesses that are growing between 3%-10% annually. High operating margins sustained for years indicate a favorable competitive position.

Revenue streams

Most of S&P Global’s revenue comes from subscriptions. This is a plus as subscriptions are recurring, and are in most cases superior to transactional revenue:

60% of S&P Global’s income comes from the US, while 23% comes from the EU, and 11% from Asia:

Competitive Advantage

S&P Global has built a formidable competitive advantage over the years, driven by several key factors:

Reputation and Trust: S&P Global's credit ratings are among the most trusted in the world. Their ratings guide investors and issuers, providing a critical benchmark for assessing credit risk. The company's history of accurate assessments and robust methodologies has solidified its reputation for reliability.

Data and Analytics: S&P Global's Market Intelligence segment offers extensive data and analytics, which are invaluable for making informed investment decisions. The depth and quality of its data give it a competitive edge, attracting clients seeking reliable and actionable information.

Ecosystem and Integration: S&P Global's integrated approach to its businesses provides clients with a comprehensive suite of services. Ratings, Market Intelligence, and S&P Dow Jones Indices can work in tandem, offering clients a holistic view of the financial markets. This ecosystem approach not only fosters customer loyalty but also opens up cross-selling opportunities.

Regulatory Barrier to Entry: The financial services industry is subject to stringent regulations, particularly for credit rating agencies. S&P Global's established position and compliance with regulatory requirements create a substantial barrier to entry for potential competitors. This regulatory moat ensures that S&P Global remains a dominant player in its field.

Strong Client Relationships: S&P Global has developed deep relationships with its clients over decades, based on the quality of its services and long-standing trust. This loyal customer base enhances revenue stability and provides a platform for future growth.

S&P Global and Moody’s handle 90% of the world’s debt ratings. The trust and relationships built over decades create an environment with high barriers to entry for competitors. Customers choosing a different provider than S&P Global or Moody’s will end up paying 30-50 basis points more for the debt. This means that competitors could offer to rate the customer’s debt for free, and the customers are still incentivized to choose one of the two leading providers. This is an incredible advantage for a business to have and means that this part of the business has substantial pricing power.

Additionally, if a customer already uses S&P Global for rating its debt, it is a much shorter distance for cross-selling other financial services that they might need, pulling clients into their ecosystem and locking them up.

Fundamentals

Operational

ROIC 5Y: 28%

Gross Margin: 65.8%

Operating Margin: 30.3%

FCF/Net Income 5Y: 114%

The Growth (10-year CAGR)

Revenue: 9.9%

EPS: 10.9%

FCF: 8.1%

Dividends: 12.6%

Book Value: 25.7%

Valuation

Fwd. PE: 26

Fwd. EV/EBITDA: 21.5

FCF Yield: 2.85%

Note: S&P Global’s ROIC fell to low levels in 2022 as S&P Global and IHS Markit merged. The main reason for the sharp decline in ROIC is due to the goodwill on the balance sheet from the merger.

S&P Global explanation of synergies on the merger:

The Stock

The stock price has compounded by 16.5% annually over the last 10 years. A total return of 459.32%. Since its inception, the stock has been a 100-bagger, returning 10037% since 1990.

Why own S&P Global?

Stable slow grower

A great business model

Wide moat and profitable ecosystem

Doesn’t need debt to achieve superior returns

Diversified revenue stream with high operating margins

Growing dividend (50 years) and stock buyback programs

Valuation

Using a discounted cash flow analysis to arrive at a fair value, with 3 different scenarios of growth and exit multiples. Growth from 6-12% which is in line with the forecasts of the management team. Using the TTM FCF of $3.18 billion, we get:

The fair value estimate for a 10% return is $80 billion. The company is currently valued at $111 billion. Based on the DCF analysis, S&P Global is somewhat overvalued. As the business is well-diversified and likely to deliver stable, profitable growth over many years, it can still be a good investment for long-term investors. But the current valuation looks a bit too expensive for my personal taste.

The market is currently pricing in my “best case scenario” (Scenario 2), with 12% growth for the next 5 years, 10% growth the following 5 years, and an exit multiple at 25. This is above what the management is guiding for, and their historic growth rates, so I have my doubts that they will reach this.

If S&P Global delivered on their $5 billion FCF estimate for 2023 (which they probably will miss), we would get a different intrinsic value. On this basis, the business looks more attractive.

The intrinsic value will depend on management’s ability to execute on growth opportunities and margin expansion. Can they unlock the synergy effects from the IHS Markit merger, or will it overall dilute the business?

Free cash flow yield

S&P Global’s FCF yield is 2.85%, vs. the risk-free rate of ~5% which seems unattractive for the moment being.

Please check out our sponsor: Quartr — Get 7 days for free & get 20% off

Conclusion

S&P Global is a fantastic business. It has several high operating margins and business units growing at a healthy rate. It is capital light (If you exclude the goodwill from the balance sheet) and it doesn’t require debt to continue to grow. It creates shareholder value by paying a growing dividend, and repurchasing their own share while growing and reinvesting where they can to further grow the business.

From a quality perspective, S&P Global scores highly. From a growth perspective, they score moderately. From a valuation perspective, they score poorly. You are not likely to get a company like S&P Global on the cheap unless there is an event that depresses prices (Like in 08-09). If you are able to get this business at a forward PE of 20 or forward FCF yield of 5%, I would consider it a good value.

S&P Global is a company you can hold for years, it is a stable and profitable business with one of the widest moats out there. It is unlikely that they won’t exist in 10 years.

Whenever you are ready, this is how I can help you:

Essentials of Quality Growth — Join more than 200 investors who have bought the guide. It is 8 years of experience condensed into 154 pages of how to successfully invest in the stock market.

(Free) Valuation Cheat Sheet — Learn an easy and reliable method of valuing a business. Learn how to set a margin of safety for your investments.

(Free) How to identify a compounder — Learn how to effectively look for great companies that you can buy and hold for the long term.

Promote yourself to +4.500 stock market investors (48% open rate) — Contact us via: investinassets20@gmail.com