Portfolio Update & Future Returns💎

Why I believe the Quality Growth Portfolio will compound by +20% CAGR

Hi partner 👋

Let’s keep it real: the portfolio’s returns have been poor over the past 12 months.

It’s never fun to lag behind the S&P 500, but my mindset is long term.

I don’t focus on a single calendar year, or even two. I look at a 5+ year time horizon.

My CAGR since I started sharing my portfolio in 2023 is 20%.

My long-term CAGR since I began investing in 2013 is 18%.

My goal is to compound at 15%+ over the long term. So far, I’m exceeding that goal.

My approach has worked extremely well over time, and I will continue to trust it despite short-term underperformance.

“Quality stocks” as a group are underperforming the broader market in 2025.

All sectors, industries, and investing styles underperform during certain periods. It’s only natural that Quality investing does as well.

Here’s what I’m excited about 👇

The long-term return of the S&P 500 is around 10% CAGR. I’m at 18%. And the best part?

My portfolio is:

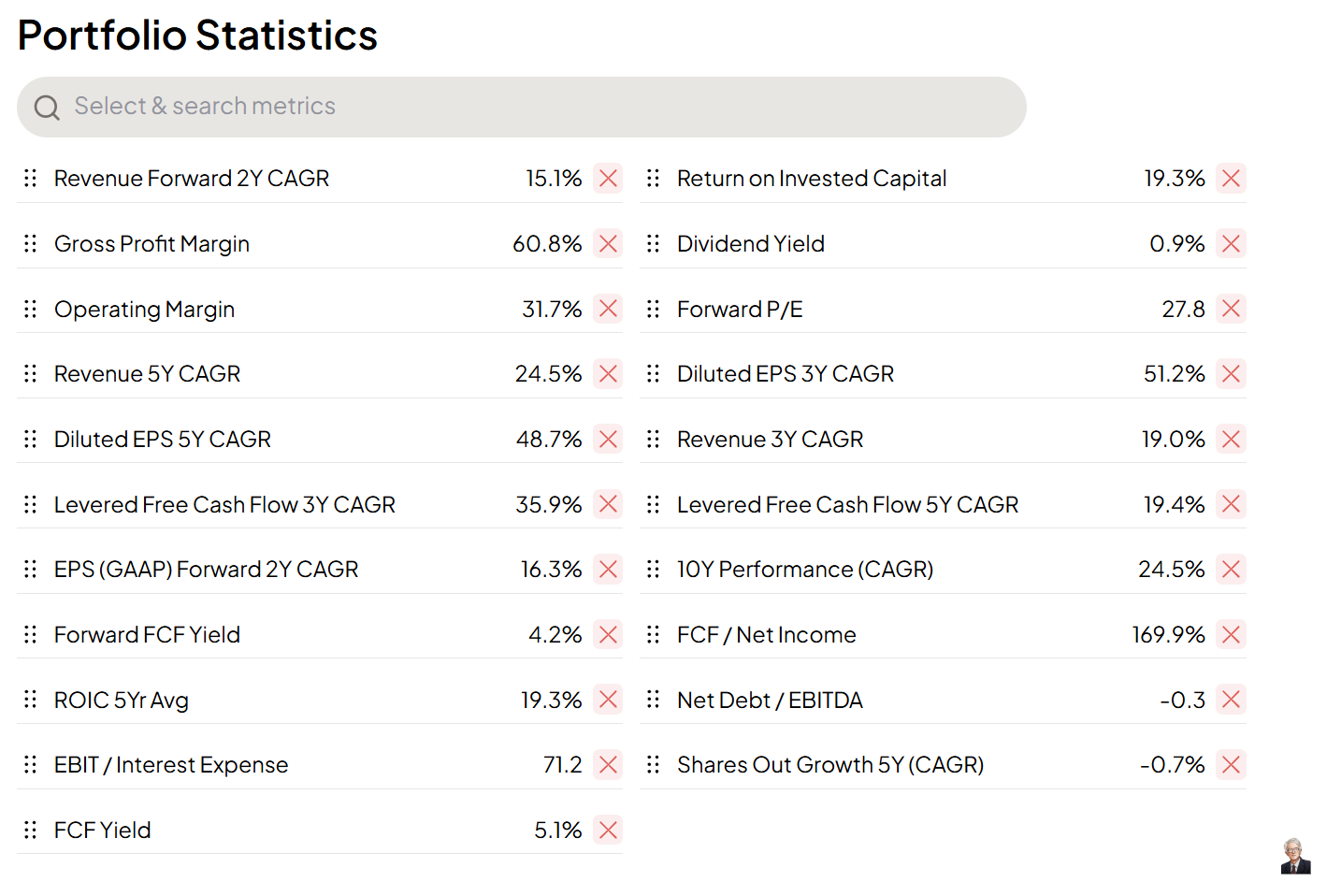

Cheaper (Free cash flow yield is 5.2% vs. 2.57%)

Higher quality (+10% higher ROIC, +10% higher operating margins)

Faster growing (Historic growth is +15% higher, future expected growth is +10% higher)

Than the S&P 500 average.

Let’s do some simple math for the Quality Growth Portfolio:

Earnings per share are expected to grow 16.3%

Dividend yield is 0.9%, growing at 15.5% per year

Free cash flow yield is 5.1% vs. the S&P 500 at 2.57%

Let’s break it down:

Earnings growth of 16.3% + 0.9% dividend yield + multiple expansion to market levels over the next 5 years (14.69% CAGR).

16.3% + 0.9% + 14.69% = 31.89%

31.89% seems unrealistically high, but that’s the number we arrive at with the assumptions above.

Where might my assumptions be flawed?

First, earnings per share. Will the companies I own grow that fast?

We have some laggards in the portfolio where growth has temporarily stalled.

The heavy capex spending of some of the core holdings might also impact future earnings per share (higher operating expenses to support new investments could reduce EPS if revenue doesn’t grow fast enough).

We could enter a recession or a tougher macro environment, where growth becomes more difficult.

There are plenty of risks.

But the fact remains: the companies I own have wide moats, exceptional returns on capital, long runways for growth, and a proven track record of expanding earnings, not just for years, but for decades.

Here is the Portfolio Statistics:

The other assumption that could be wrong is that my portfolio will always trade at a discount to the index on a multiple basis.

The index is often heavily weighted toward its strongest performers, many of which have earnings expectations far into the future. That helps justify today’s high multiples.

So maybe we can expect my portfolio of high-quality stocks to re-rate closer to a 3%–3.5% FCF yield. (Keep in mind, the S&P 500 as a whole trades at a 2.57% FCF yield, extremely expensive in my view.)

Just look at the S&P 500’s multiple expansion since 2016:

A move to 3.5% FCF yield over 5 years would imply a 7.85% CAGR from multiple expansion.

A move to 3% FCF yield over 5 years would imply an 11.18% CAGR.

Even if I’m slightly off, that still suggests very strong returns.

Let’s make a more conservative estimate:

In 5 years, my portfolio trades at a 3.5% FCF yield, grows EPS by 12% annually, and pays an average dividend yield of 1% per year.

That would give:

Multiple expansion: +7.85% CAGR

Earnings per share: +12% CAGR (including buybacks)

Dividend: +1%

Total return: 7.85 + 12 + 1 = 20.85%

Not bad. And broadly in line with the portfolio’s performance since I started sharing it online in 2023.

My portfolio is attractively valued, with strong growth prospects over the next 5 years, and holds dominant competitive positions making it difficult for competitors to take market share.

Does that sound compelling? I think so. And for me, it’s a much more comfortable position than owning an S&P 500 index fund at a 2.57% FCF yield.

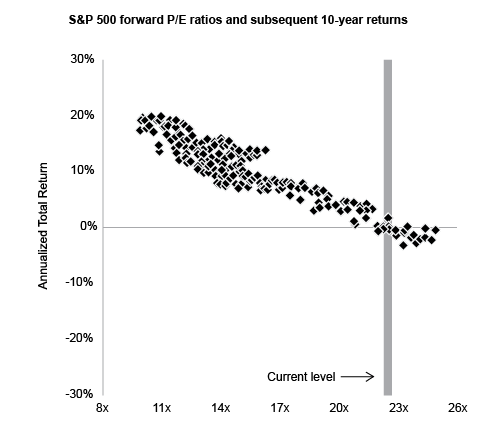

My portfolio is positioned to return 15–20% over the next 5 years. Historically, from these valuation levels, the S&P 500 has rarely delivered more than 2% CAGR over the following years if we look at the data:

That said, times are changing. Companies are becoming more capital-efficient. We’re seeing the first one-person companies valued at over a billion dollars, and the composition of the index is evolving rapidly compared to the historical data we reference.

This could justify structurally higher multiples for the index, as asset-light, high-ROIC businesses deserve premium valuations.

Still, I believe you need a fairly bullish assumptions to project a 10%+ annual return for the S&P 500 over the next decade. For example, the index would need to grow EPS at around 10% annually while maintaining today’s elevated multiples. Not impossible — but not especially conservative in my view.

So that’s my case for why I believe my portfolio can significantly outperform the S&P 500 over the next 5–10 years.

Now let’s look at the top 5 holdings.