Adyen is a Quality Growth Business with Secular Tailwinds and a Superior Business Model 💎

Stellar growth, high return on capital, and a long runway for reinvestments. 🧠

I’m writing a book on Investing, stay tuned!

The business

Adyen operates a payments platform that integrates a payments stack that includes gateway, risk management, processing, issuing, acquiring, and settlement services for its customers.

Adyen offers a back-end infrastructure for authorizing payments across merchants' sales channels, as well as online, mobile, in-store, and APIs; and data insights. The company's platform services a range of merchants across various verticals, connecting them directly to Visa, Mastercard, and other payment methods.

The Product

Adyen operates within several categories in the payment space.

Their main service is payments. They offer online service, in-person, cross-channel, and platform integration.

As add-on products, they offer “Enhancements” like “Risk management”, revenue optimization, and other products that create insight and value for their customers.

Pricing

Customers of Adyen pay a fixed Processing Fee of £0,10 + the payment method fee. There are no setup fees and there is one integration. This means that Adyens customers only pay for what they use (E.g. no monthly fees) and that Adyens customers can offer their customers all their preferred payment methods through their solution.

Adyen is growing rapidly and globally:

+41% in EU yoy

+74% in NA

+48% in Asia

+24% in Latin America

The fundamentals

ROCE: 26.7%

Gross Margin: 14.88%

Operating Margin: 9.74%

Cash Conversion: 100%

Cash & Equivalents: £6.98BN

Net cash: £1.4BN

Interest coverage: 55.6x

Fwd. PE: 72

PS. 5.7

PEG: 1.11

Note: Adyen’s margins do not exclude costs from financial institutions. Adyen excludes this cost when calculating its margins, giving them an EBITDA margin of ~60%.

The Stock

Adyen’s stock price has compounded by 25% over the 5 years it has been a public company. The stock is significantly down from its post-pandemic highs. However, Adyen has far outpaced its peers, Square and Paypal:

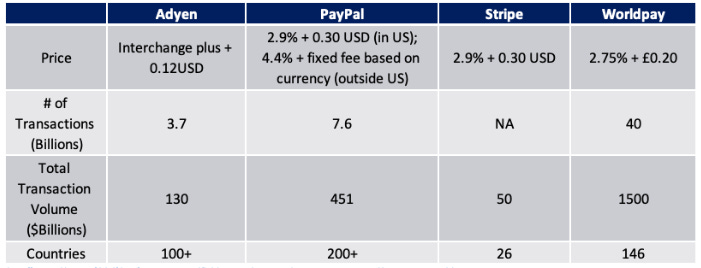

Competitive Advantage

Pricing

Adyen offers a more competitive pricing structure than its main competitors - PayPal, Stripe, and Worldpay.

Speed of implementation and integration

One of Adyen’s biggest advantages is that it acts as a global platform with direct connections to international cards, enabling plug-and-play expansion to new regions.

Simplifying the supply chain

Creating an easy-to-use and implement one-stop shop for enterprises to connect with payment companies. This picture illustrates how Adyen simplifies the supply chain:

Management: Skin in the game

Pieter van der Does is the co-founder and CEO of Adyen since 2006. Pieter owns a 3% stake in Adyen, valued at £1.29 billion.

The superior pricing structure, speed of implementation, simplification of the supply chain, and alignment of the CEO and shareholders add up. It is hard for new entrants and existing competitors to compete with Adyen’s compelling business model. This shows up in the return on capital Adyen has vs. its peers:

Want to try Stockopedia? I use it for:

Company comparison

Financial stock analysis

Global stock idea generation

The best global stock screener I have tried yet

Invest in Quality subscribers can try Stockopedia 14 days for free, and get a 25% discount if you decide you want to keep using it. Use my link to get the discount: Stockopedia

Key Growth Drivers for Adyen

Existing merchants - Adyen’s customers are growing, hence higher processing volumes, plus expanding relationships where customers want more of Adyen’s offerings. This entails channel expansion and geographical expansion.

New merchants - “We have a direct sales approach focused on onboarding new merchants in all geographies where we are present and verticals we are targeting, both of which are constantly expanding.”

Capitalizing on evolution in the industry: Adyen's strength is in its speed and the ability to react to market developments that can help its merchants due to the structure of its technology and its teams.

Deepening platform offering to existing merchants - These businesses are often looking for turnkey solutions that they in turn can offer to their SME business partners.

The Growth (5-Year CAGR)

Revenue: 55%

Earnings per share: 50.8%

Free cash flow per share: 58.2%

Operating Income: 47.9%

Processed volume for 2021 516BN (+70% yoy)

“Net revenue”: 1BN (Gross profit) (+46% yoy)

Book Value: 44.2%

Note: This growth is really something special, and warrants a premium in the market.

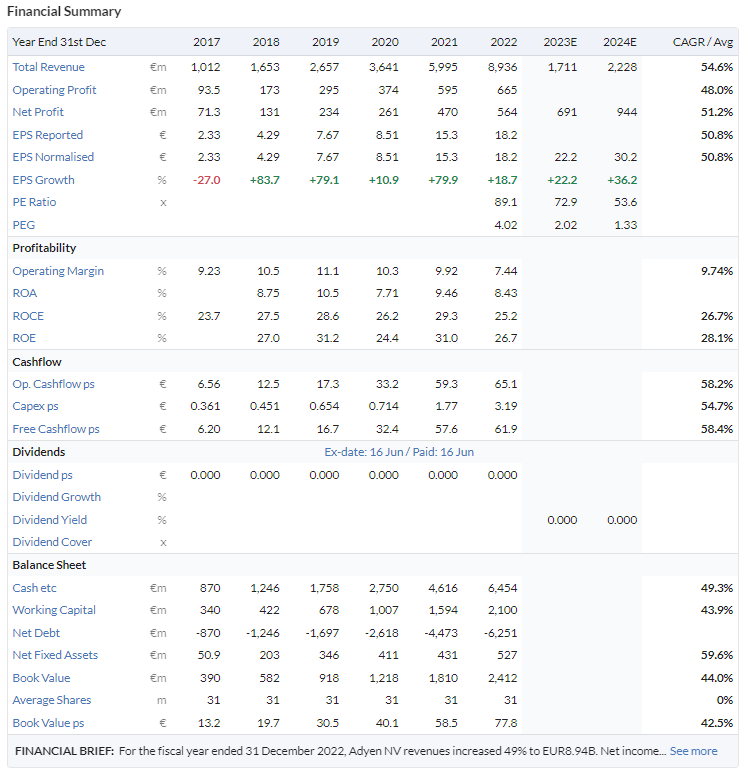

Financial summary

Why own Adyen?

Strong future growth prospects

Wide moat based on its business model and cost structure

Doesn’t need debt to achieve superior returns

Generates high amounts of cash

High return on capital (Employed and Invested)

Owner operator

The Risk

Competition: Adyen faces competition from actors with significant scale, like PayPal.

Substitutes: Adyen faces potential competition from non-traditional payment processors.

Disruption risk: If Adyen does not follow the technological advances made in the payment space, they risk becoming obsolete.

The concentration of merchants: Large merchants typically have arrangements with multiple payment service providers. If one of these merchants terminates the contract they have with Adyen, it would result in lower processing.

For investors, there is also a risk of paying too much for a company that heavily relies on future growth to justify its current valuation.

Valuation

Adyen is what Terry Smith would refer to as “highly rated”. Their multiples are very high and are dependent on high future growth for Adyen to be a good investment at current levels.

FCF Yield: 1.4%

Risk-free-rate 3.7%

Normal Scenario: 25% growth for 5 years, then 20% for the following 5 years, and valued at 30 times FCF at the end of the period.

Worst Scenario: 15%, 10%, valued at 25 times FCF.

Best Scenario: 30%, 25%, valued at 35 times FCF.

Using Adyen’s TTM free cash flows of £607 million (Source: Bi-annual reports)

Current MARKET CAP: £43 billion

Normal scenario: 56.5 billion (31.4% upside)

Best scenario: 89.8 billion (108% upside)

Worst scenario: 24.5 billion (-43% downside)

Weighted present value: 50.2 billion (16.7% upside)

Using a DCF to value a fast-grower like Adyen can be challenging. If we estimate that Adyen will continue to grow at historical rates of 40-50% annually, the company is significantly undervalued. Even if we use what is consensus expected from Adyen, of ~30% annual growth rate, the business is a good value at current levels (My best case scenario above).

The question always comes back to:

Can Adyen keep growing at high rates?

Can Adyen expand its moat and hence keep competitors at bay?

Can Adyen keep growing profitably?

Can Adyen grow without diluting shareholders?

Assuming we want a 15% annual return, Adyen’s price would have to drop to ~£37 billion (-14% from current levels):

If you haven’t already, check out my free Valuation Cheat Sheet

Conclusion

Adyen is a quality, fast-growing company with a strong competitive position. The business has been compounding its earnings by more than 40% annually over the last 5 years, and its future prospects look compelling as a lot of the world is still transitioning to digital payment.

Adyen has a significant competitive advantage from its business model and owner-operator structure, allowing management to be aligned with shareholders and have a long-term mindset.

Based on our DCF analysis, and Adyen’s historical multiples, Adyen is close to fair value for a 10% annual return. The macro-environment has changed with inflation, higher rates, and a “looming recession”. This of course poses risks for Adyen, but the company does not need debt to grow and is profitable with a net cash position of £1.4 billion.

Disclosure: I’m long Adyen since Q2 2022, with a cost of £1274. I’m looking to add more if the company delivers and Mr. Market provides a compelling entry.

8/11 is investor day, interesting is also the big own and operational cash position. Will bring huge additional income

Hi, Any change in valuation?