Invest In Quality is writing a book on Quality Growth Investing to be released in August, join the pre-sale list to get a discount when the book releases here: SurveyMonkey

Booking Holdings is the world's leading provider of online travel and related services, provided to consumers and local partners in more than 220 countries and territories through six primary consumer-facing brands: Booking.com, Priceline, Agoda, Rentalcars.com, KAYAK, and OpenTable.

Mission: To make it easier for everyone to experience the world.

The Business Model

Booking.com operates an online travel agency. It acts as an intermediary between travelers seeking accommodations and a vast array of lodging options, including hotels, apartments, vacation homes, and more. The platform is user-friendly and it is easy to compare different traveling options. Booking.com makes money from earning a commission on bookings made through its platform.

The Revenue: Commission-driven

Booking.com's revenue primarily stems from commissions earned on each successful booking facilitated through its platform. For every reservation made, the company receives a percentage-based commission from the accommodation provider. This commission structure has proven to be a lucrative revenue stream, considering the sheer volume of bookings processed on the platform.

Booking.com revenue and earnings are related to how many potential customers they can get on their website, and how many of these customers are converted into ordering their vacation on Booking.com and not on other websites.

Thanks for reading Invest in Quality! Subscribe for free to receive new posts and support my work.

The Stock: A Snapshot of Performance

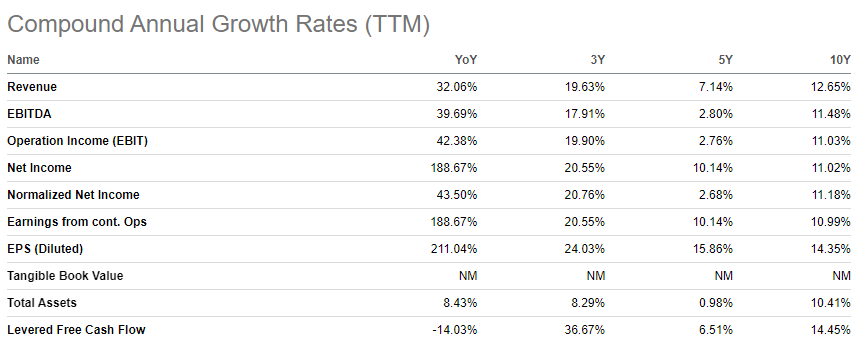

The stock has compounded by 9.4% annually for the last 10 years, as it has grown steadily on the top and bottom lines for that period.

The Growth: Post-Pandemic Boom

Growth has been steady over the last decade, with revenues at 12.65% annually, earnings per share at 14.35%, and levered cash flows at 14.45%. In more recent times, booking.com has benefited from the post-pandemic traveling boom, which is likely to persist for some time. Revenues are up 32% YOY, EBITDA is up almost 40%, and net income is up 188%.

Try Stockopedia 14-days for free using our link (Sponsored).

The Invest In Quality team use the platform to:

Research Global Stocks

Get weekly ideas from the Stockopedia team

Use their stock screener to find hidden global gems

Try it 14 days completly free, if you like it, you will get 25% off your purchase using our link: Stockopedia (You also have 30-day money back guarantee after the 14 days)

Competitive Advantage: A Wide Network and Brand Recognition

Wide Network

Booking.com has built a global network of accommodations that use its services. Just starting a website and trying to drive traffic to it won’t be effective when competing with Booking.com, as they have exclusive deals and countless categories the customer can choose from.

Barriers to entry

It would require a lot of capital for a new entry to compete with Booking.com head-on, as years of satisfied customers have solidified them as trusted allies when ordering vacations.

Brand Recognition

The booking.com brand is well recognized, which positions them well for an increase in traveling spending.

Booking.com holds a favorable competitive position, but not a wide moat.

Why Own Booking.com?

Steady compounder

Secular trends in the traveling segment

Solid fundamentals

Solid growth

Capital light business

The Risk: External Factors

Risk of substitutes: The emergence of new platforms like Airbnb poses a real threat to Booking.com’s business model in the future. Consumers are looking for authentic experiences and might drop the traditional hotels in favor of living in someone’s house or cabin.

Macroeconomic factors: The travel industry is sensitive to economic downturns. Often, the first thing consumers cut back on is their travel.

Slow mover: Booking holdings are less agile and flexible than the new smaller businesses finding new ways to offer travelers great experiences.

Thanks for reading Invest in Quality! Subscribe for free to receive new posts and support my work.

The Valuation

Using a discounted cash flow analysis with the 3 following scenarios:

Worst: Growth 7% for the next 5 years, then 6%, valued at 20 times FCF at the end of the period.

Best: Growth 15% for the next 5 years, then 12%, valued at 30 times FCF at the end of the period.

Normal: Growth 10% for the next 5 years, then 8%, valued at 25 times FCF at the end of the period.

Booking Holding is today valued at 18.4 times FCF or an FCF Yield of 5.4%

At the current valuation of $114Bn, we can expect an above 15% return (~17%) if the business manages to keep growing its FCF at 10%:

Conclusion

Booking Holdings is a capital-light compounder that is likely to keep growing as more consumers are turning online to order their vacations and accommodations. The industry is experiencing a boom after the pandemic, and Booking is well-positioned to capitalize on this trend. Their fundamentals are solid, and their growth has been good, especially in recent times.

The potential risk for Booking Holding is the threat of new substitutes like Airbnb, that are offering new, authentic, and cheap experiences worldwide. Currently, there is room for both types of companies, but as Airbnb grows, they might take more and more of Booking Holdings’ market share.

The most exciting element of Booking Holding is its valuation. It trades at an FCF yield of 5.4%. For a growing capital light compounder, this is a solid valuation.

Disc: Invest In Assets holds no position in the stock discussed.

Thanks for reading Invest in Quality! Subscribe for free to receive new posts and support my work.