5 Undervalued Quality Businesses💎

Down -20 to -48% with high cash flow generation ✅

Hi there, partner 👋

Markets have been brutal lately, especially for quality investors. Tech has sold off. Software has completely collapsed. And a handful of businesses with real moats, cash flows and compounding opportunities, are trading at multi-year low levels.

That’s what we’re digging into today.

These are not businesses that are deteriorating, it is a list of quality names where the fundamentals are still intact, facing sentiment-driven price reductions. The valuation levels has reached levels where long-term investors are likely to be rewarded.

Let’s take a look at the 5 undervalued companies in question 👇

1. 🧩 Topicus.com $TOI.V

Price: ~CAD $99.60 | Down ~48.8% since July 2025

The business

Topicus is the European arm of the Constellation Software empire. A serial acquirer of niche vertical market software businesses in the Netherlands and broader Europe.

It operates the same playbook as its parent: find small, mission-critical software companies with sticky recurring revenue, buy them at fair prices, never sell, and let the cash flows compound.

Constellation Software still owns 48% of shares outstanding, which tells you everything you need to know about who’s watching this closely.

Why it’s down

Two things have conspired against Topicus in the past year:

A brutal sector-wide selloff in vertical market software driven by AI fears

A period of slower organic growth.

The AI risk is real, to some extent. Yes, it is much easier to create the code for services that can replace many of Topicus’ VMS businesses. However, Topicus’ advantage is:

Deep relationships with organizations and government. The name of the game here is trust, reliability, and assurances. And Topicus has built a network of loyal customers that won’t trust anybody to process their data or to create workflows deeply embedded in the corporation.

Data, data, data. It’s all about the data, and Topicus has this in groves. It’s hard to create industry defining services without customer data to improve the product over time.

Switching costs are real. Software is often a really low cost for a corporation. If the migration is a hassle (Which it always is), a company will dread switching software unless they absolutely have to.

AI lowers the barrier to build. It does not lower the barrier to replace. A better product is not enough when the incumbent owns the workflow, the data, and the relationship.

Is Topicus a quality business?

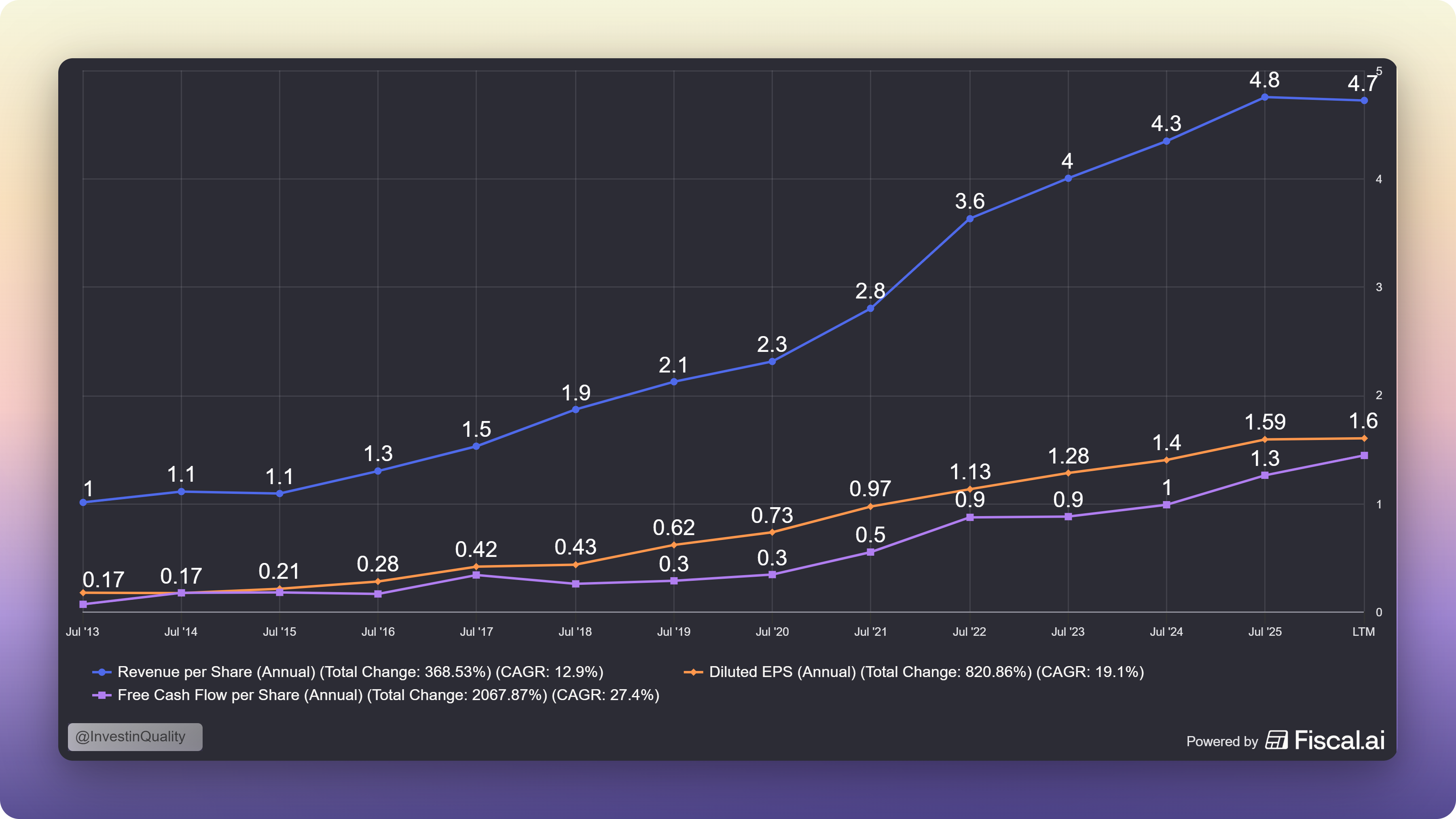

Let’s first look at the growth in the most recent quarters:

Revenue per share CAGR: +20.4%

Free cash flow per share CAGR: 26.9%

Book value per share CAGR: 21.7%

The business is growing rapidly ✅

Return on capital has consistently been in the 15-25% range since 2018:

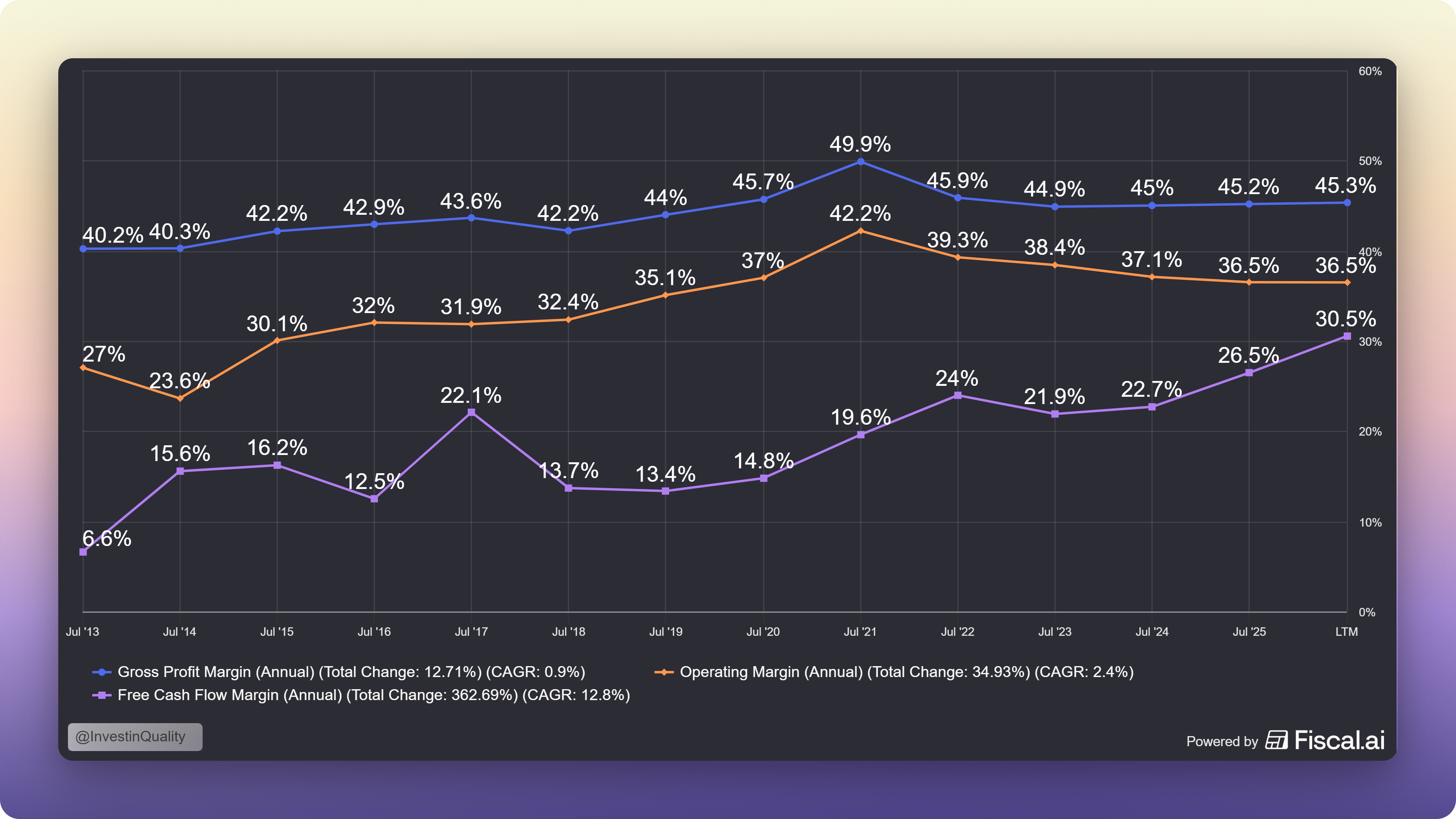

Gross, operating, and free cash flow margins have been stable:

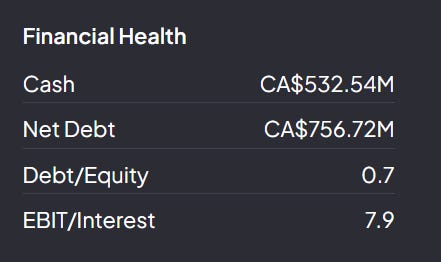

The company is in solid financial shape:

Valuation

Topicus is is trading at all time low valuation multiple levels.

Right now, the FCF yield is 7.61%, which is really high for a quality business.

Especially with the back drop that the business is not broken, but its cheap because the market doesn’t want to touch software right now.

High quality business, attractive valuation.

2. 🚗 Copart CPRT 0.00%↑

Price: ~$33.36 | Down ~47.8% since May 2025

The business

Copart is the dominant global marketplace for salvage and used vehicles. It operates a two-sided platform connecting insurance companies (who need to dispose of totaled cars) with buyers (dismantlers, rebuilders, dealers, and exporters).

The business model is extraordinarily capital-efficient once yards are built: network effects, marketplace dynamics, and significant switching costs for insurers who have integrated Copart deeply into their claims workflow.

Why it’s down

Copart’s volumes at key insurance customers declined slightly as the number of uninsured drivers increased following several years of massive insurance premium inflation.

When premiums rise too fast, some drivers drop coverage. Fewer insured drivers means fewer total loss events, which means fewer cars flowing through the auction. Q2 FY2026 revenue fell 3.6% year-over-year to $1.12 billion, with EPS dropping from $0.41 to $0.36.

The market reacted harshly to a business it expects to compound consistently.

The numbers that matter

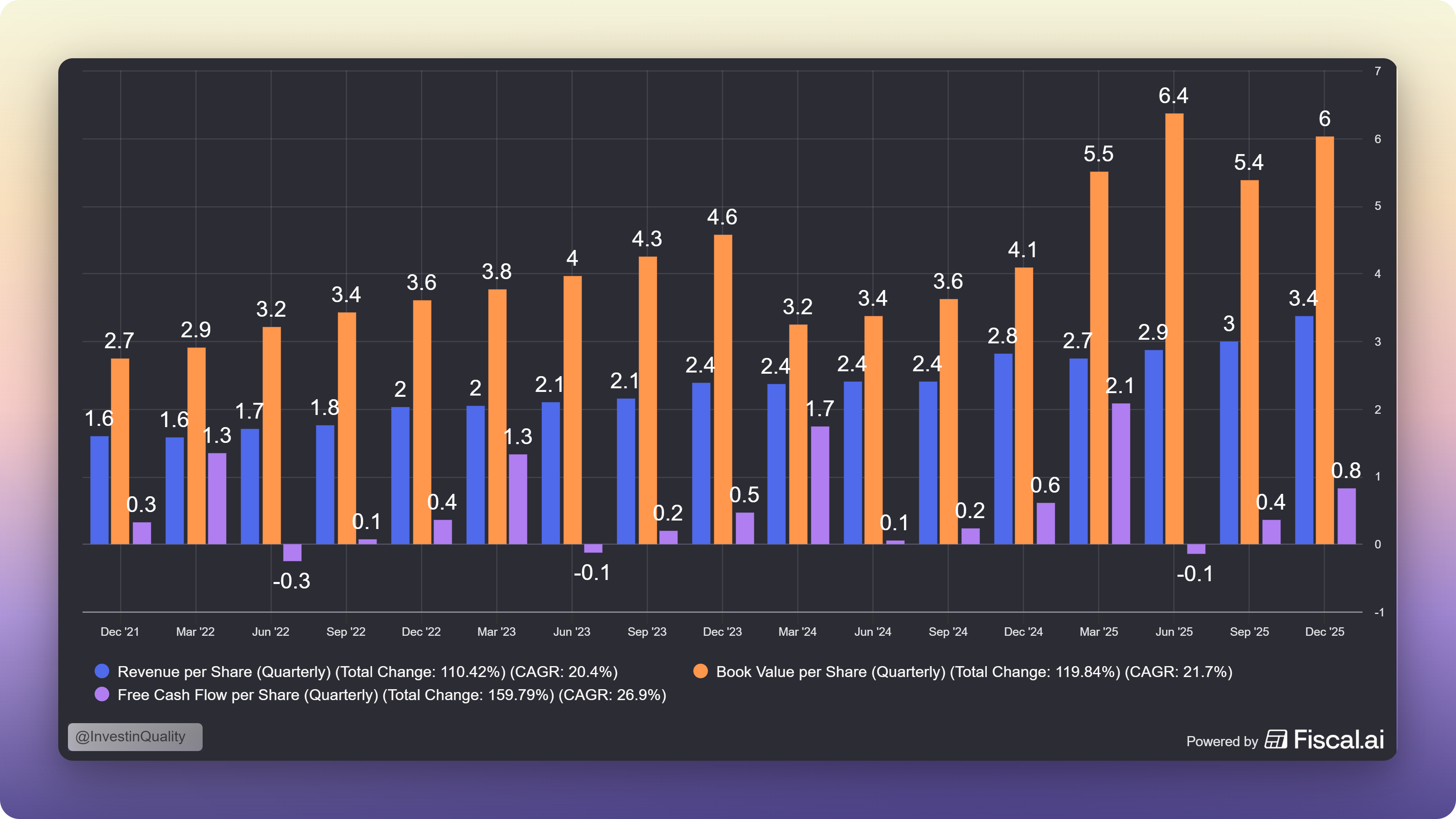

Copart’s growth has been impressive:

Revenue per share CAGR: +12.9%

Earnings per share CAGR: 19.1%

Free cash flow per share CAGR: 27.4%

Although revenue have slowed down, free cash flow keeps compounding at attractive rates ✅

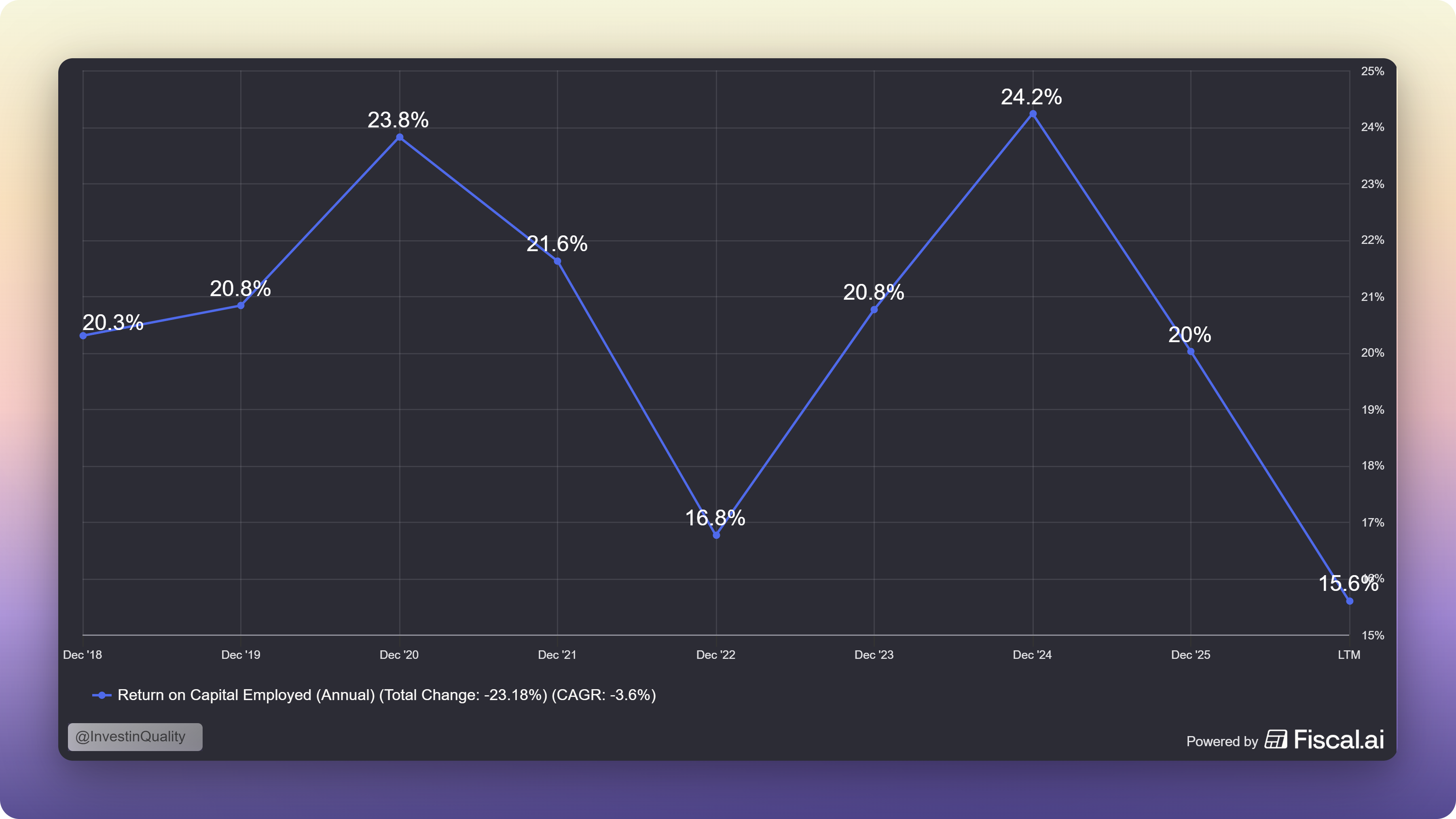

Copart’s return on capital is unmatched, usually staying well above 25%:

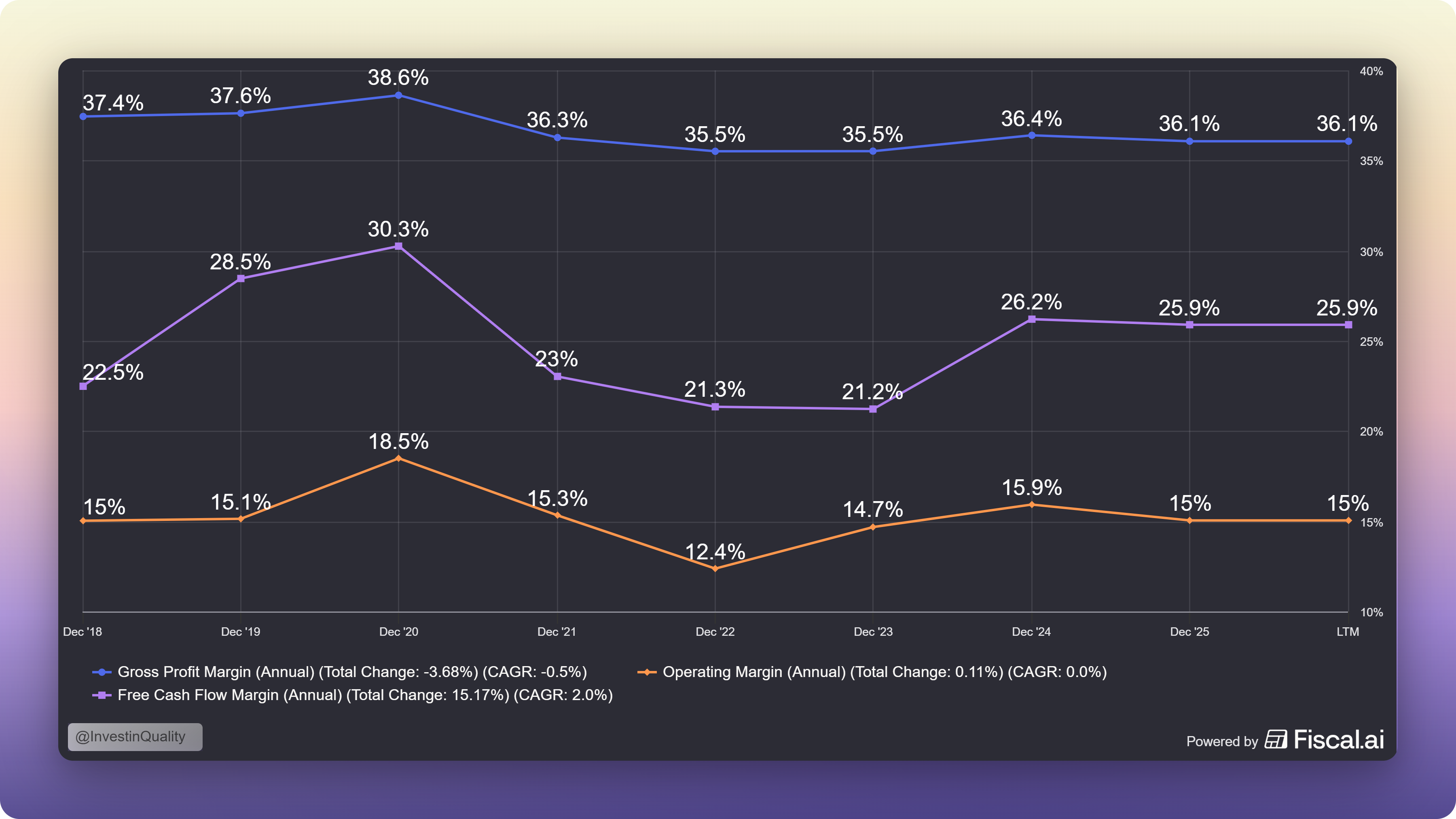

Margins are not only stable, but also expanding over time. This is a sign of a business with a sustainable competitive advantage.

Copart’s moat hasn’t moved an inch, and there is no sign of deterioration.

They have over 200 yards, their own auction technology, and are deeply embedded into the insurance industry claim process (It will take a long time to replicate).

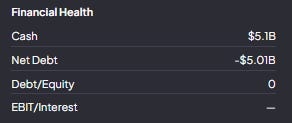

Copart’s balance sheet remains flawless, with a $5.1 billion of net cash position.

While revenue growth has slowed in the last few years, earnings per share and free cash flow continue to grow at attractive rates.

Valuation verdict

At 21x forward earnings for a business with no debt, 34% net margins, $5.1 billion in cash, and a near-monopoly position in vehicle auctions, this is a genuinely attractive entry point.

If you subtract the $5.1 billion from the market cap, you get a forward PE of ~17x.

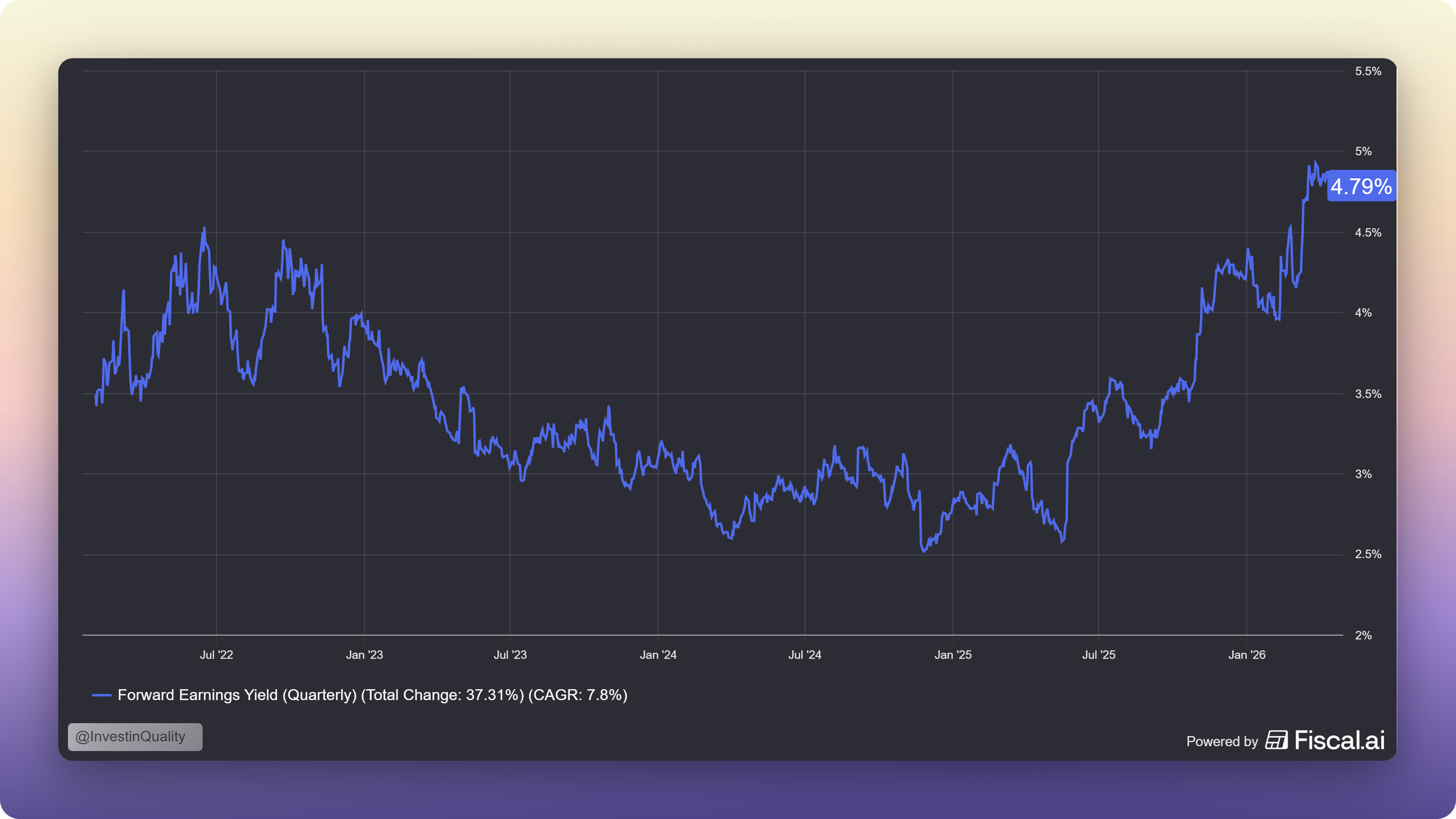

The FCF yield is also at a multi-year high of 4.79%, not seen since 2017: