5 Quality Buys February 💎

High quality businesses pulling back -20% to -50%

Hi partner! 👋🏻

Welcome to the Feburary edition of Top 5 Buys ✅

In this article, we will discuss our top stock picks for February 2026.

Let’s get into it 👇

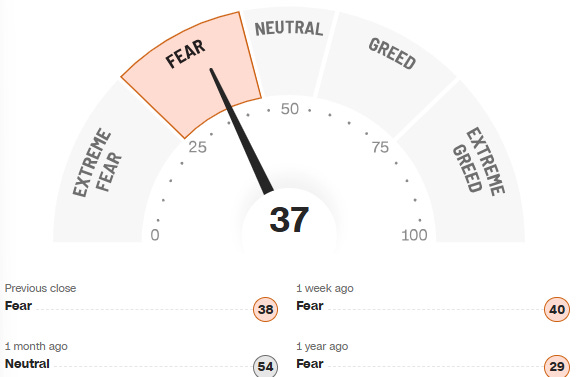

The Market Sentiment: Fear 😨

The market is volatile as a result of:

Interest rates being “Higher for longer”

Mega-CapEx budgets (Way higher than expectations)

A changing world order and global politics

Investors answer this uncertainty with fear — pulling money out of the market.

After a brief optimistic second half of 2025, the trend is now negative:

The crazy part? Despite massive fear and uncertainty — the S&P 500 is still close to all time highs:

This is simply because many of the largest companies in the S&P 500 have held up very well, think Nvidia, Alphabet, and Apple.

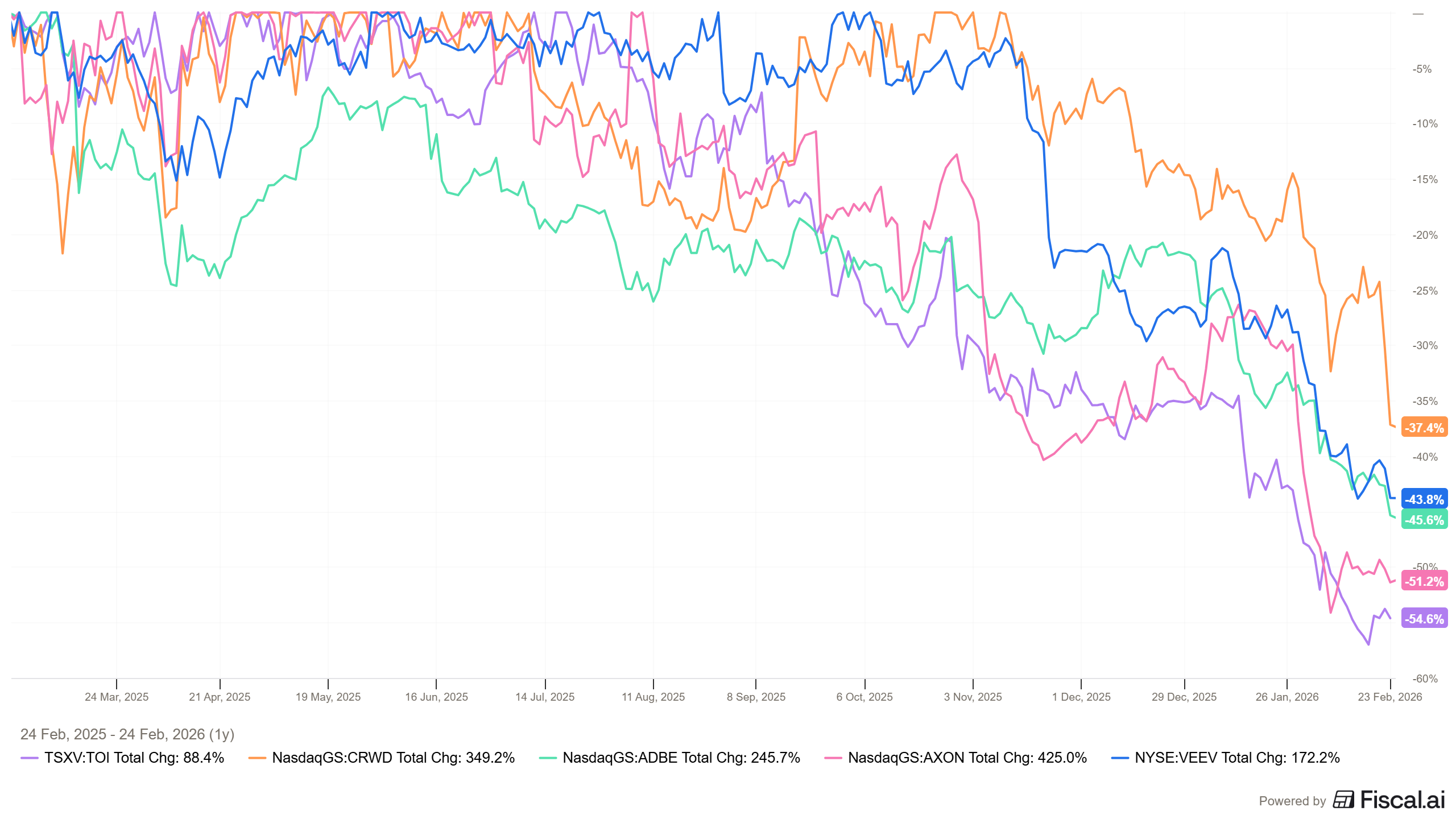

“SaaS” companies have not been that fortunate, after the narrative shock we’ve seen with the ‘agentic AI’ wave, many former darlings are struggling big time:

Fast growing strong businesses like Crowdstrike and Axon are down -37.4% and -51.2% respectively. And community darlings like Topicus is down -54.6% from its all time highs.

Predicting the future is impossible, but we can point to 5 quality growth companies that are likey to continue compounding despite the prevailing narrative being that AI will eat Software-as-a-Service for lunch.

Here are this month’s Top 5 👇

#1 Microsoft MSFT 0.00%↑

Microsoft is not a “SaaS”-business, it is a infrastructure business.

Azure isn’t a project management tool you cancel in a downturn. It’s where the workloads live. And workloads don’t leave easily.

Across Windows, Office, security, developer tools, and cloud, Microsoft is deeply embedded into the operating system of global business. The switching costs at scale are enormous. From a technical, financial, and political perspective inside organizations.

Copilot inside Microsoft 365 is a way for Microsoft to improve the product, monitization and stickyness of the product for hundreds of millions of users.

The business of Microsoft has:

Massive cash flows (Free cash flow is somewhat restricted due to high CapEx spend)

Pristine balance sheet

Bundling powerful tools and products across the entire tech stack

When budgets tighten, vendors consolidate. And consolidation favors platforms. And who is the king of enterprise platforms? You guessed it, Microsoft.

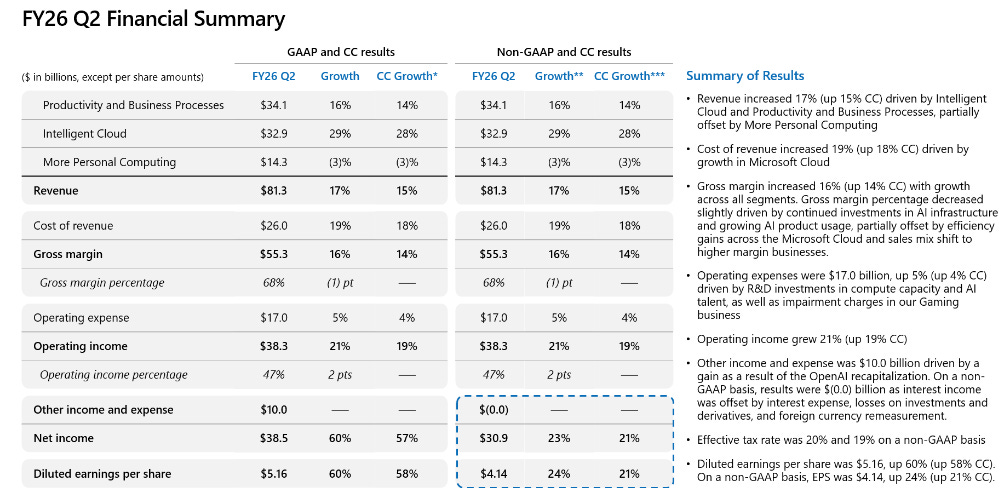

And it’s not like Microsoft is showing weakness in its fundamentals.

Productivity was up +16% YoY

Intelligent Cloud was up +29% YoY

Diluted earnings per share was up +60%

In the most recent quarter:

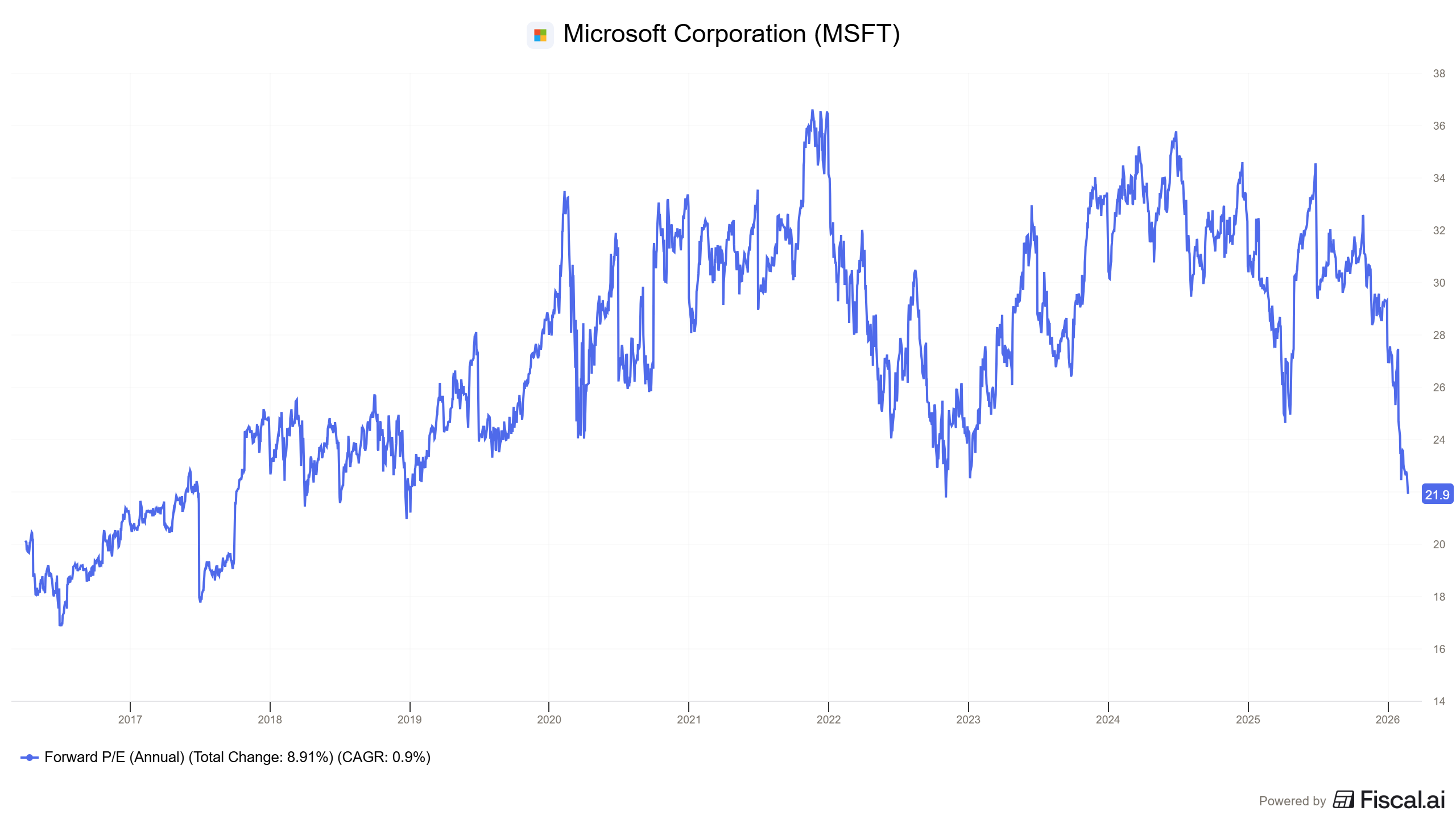

The fact of the matter is that Microsoft is a pristine quality business, growing at unheard of levels for its size, now trading at 21.9x forward earnings:

The last time Microsoft was trading at this level was in the 2022 sell off — a great time to add shares.

Microsoft has a free cash flow yield of 2.2% + 14.3% expected long term growth.

FCF yield of 2.2% + 14.3% growth = 16.5%

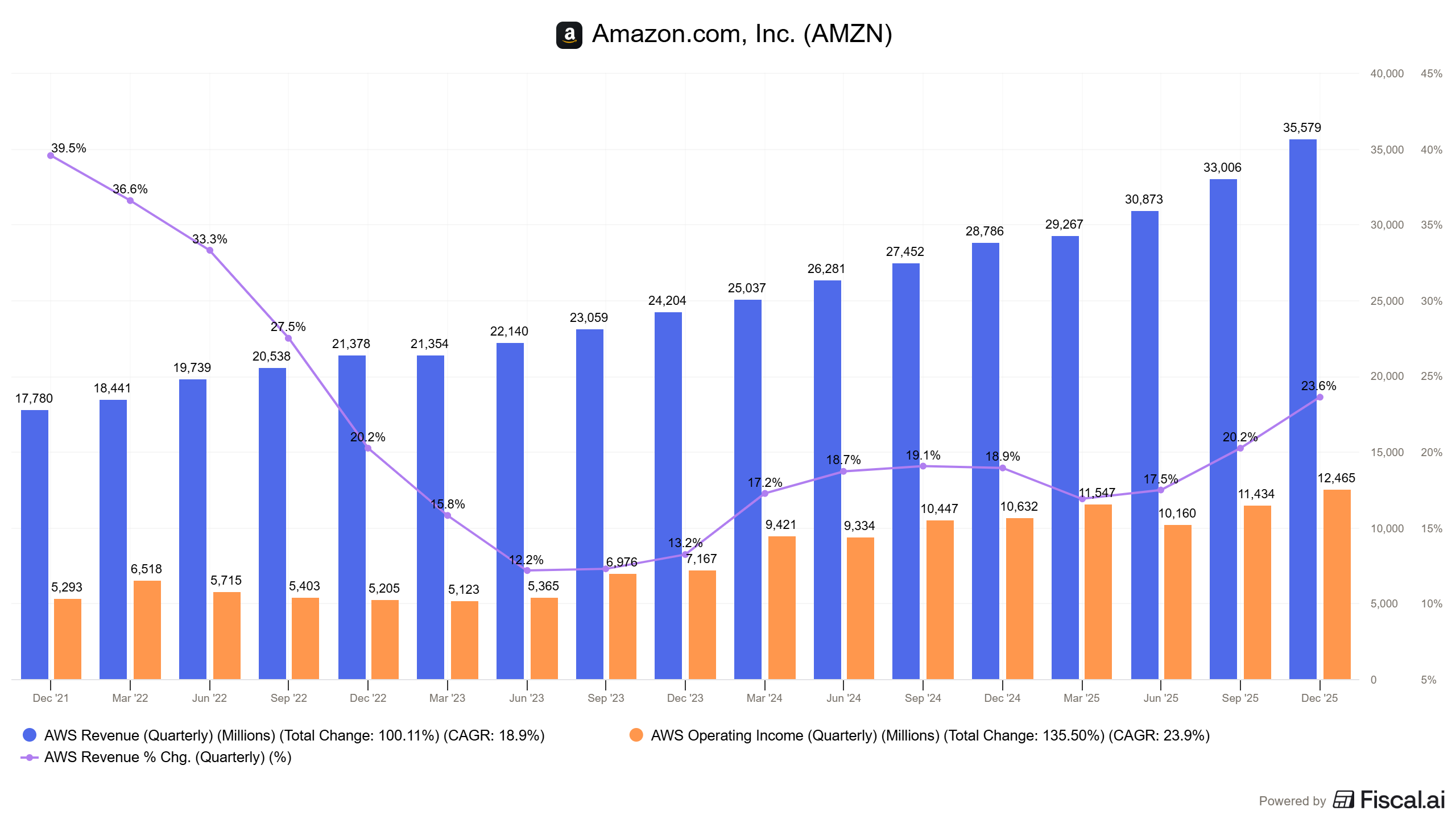

#2 Amazon AMZN 0.00%↑

When SaaS sells off, anything cloud-related gets dragged down with it.

But AWS is not optional software, it is the infrastructure where modern digital businesses are built.

When customers cut costs, they may reduce usage, but they don’t rip out AWS. The workloads stay. That distinction matters.

All the focus is on AWS; the rest of Amazon is chronically mispriced.

Retail margins expand meaningfully when cost discipline improves. We’ve already seen what happens when fulfillment efficiency tightens and overcapacity normalizes.

Amazon’s advertisement business is a high-margin machine integrated directly into purchase intent. A structural advantage for Amazon that is part of their flywheel.

And ultimately, Amazon’s optionality allows it to reinvest across logistics, AI, devices, healthcare, and Prime. Few companies in the world have that capital allocation flexibility.

Free cash flow always looks weak at the peak of capex cycles. And then it inflects when investment moderates.

Add AI to the equation:

AI workloads don’t replace cloud infrastructure. They increase the demand for it. And AWS remains one of the foundational platforms.

The acceleration in top-line growth is a sign that this is happening:

Despite the reaccelleration of AWS and other business segments, Amazon continues to trade at attractive rates.

Looking at price to operating cash flow because free cash flows are temporarily depressed due to a large CapEx investment cycle, and earnings not providing a realistic picture of earnings capacity:

Amazon has an earnings yield of 3.5% + 17.3% expected long term growth.

Earnings yield of 3.5% + 17.3% = 20.8%