5 Quality Compounders I'm Watching Right Now 🏰

High growth, high quality, attractive valuations 💎

Hi partner 👋

I don’t buy stocks I’m not ready to own for a decade. But that doesn’t mean I stop looking.

There’s a list I keep of companies that have passed my initial quality filter, that I’ve spent real time understanding, but that I haven’t pulled the trigger on yet. Either the price isn’t right, or I’m still working through a question I can’t fully answer, or I’m simply being patient.

Today I want to share five names sitting on that list right now. These aren’t speculative ideas. Every one of them has a durable competitive advantage I can articulate clearly, a management team that allocates capital like an owner, and a business model I’d be comfortable holding through a downturn.

What they don’t all have yet is the right entry point.

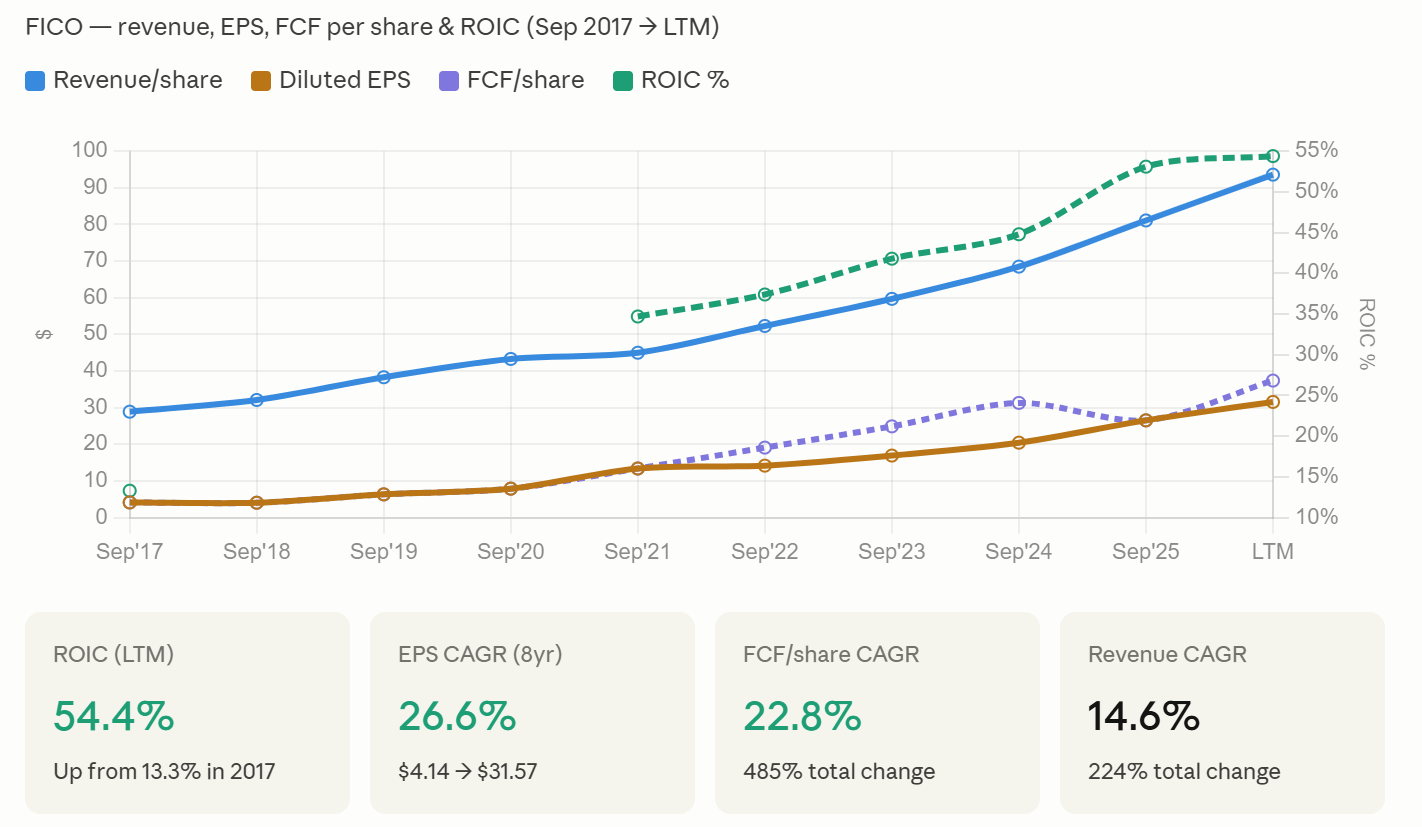

1. FICO: The toll road nobody talks about

If you’ve ever applied for a mortgage, a car loan, or a credit card in the United States, FICO scored you. You probably didn’t think about it. Neither did the lender. That’s exactly the point.

Fair Isaac Corporation sits in one of the most enviable competitive positions in American finance. Its FICO Score is embedded so deeply into the credit decisioning infrastructure of US lenders that replacing it isn’t a technology problem, it’s a coordination problem. Every major lender uses it. Every regulator references it. Every consumer knows their number. The network is the moat.

What makes FICO genuinely interesting right now isn’t the scoring business alone. It’s the transition happening underneath it. The company has been transforming its software division into a subscription-based SaaS platform. Revenue from this segment is becoming stickier, more recurring, and higher margin. And then there’s the pricing story: FICO charges mortgage lenders a fee each time a score is pulled, and that fee has been going up, meaningfully, year after year. The lenders complain. They always complain. But they keep paying.

Put all three together, the scoring monopoly, the software platform transition, and demonstrated pricing power, and you get a business that has compounded both earnings and free cash flow at a remarkable rate for nearly a decade.

The SaaS platform ARR tells an equally compelling story. Platform ARR has grown from $47.7M in 2021 to $348.8M LTM, a near 7x increase in four years.

Meanwhile, Dollar-Based Net Retention on the platform sits at 136% LTM, meaning existing customers are spending significantly more each year.

FICO has traded at astronomic multiples in the last few years, but now FCF yields are at multi year highs, giving investors a opportunity to both get earnings/fcf growth and multiple expansion if the investment case turns out bullish.